Original content

In Argentina, 70% of the 930,000 hectares (ha) of maize cultivation are in excellent condition, while the remaining 30% are in good condition. Based on early harvest projections, they anticipate a good yield in 21% of the country. Beneficial rains in Oct-24 and Nov-24, particularly in regions where rainfall exceeded 60 millimeters (mm) in the last ten days, have significantly boosted crop conditions. These rains have enabled farmers to prepare for a robust harvest. Southeastern Córdoba and Northwestern Buenos Aires are the most favorable regions for maize harvesting, especially after recent storms that have enriched soil moisture levels.

Argentina's 2024/25 season corn production estimates have been slightly revised downward to 59.5 million metric tons (mmt) compared to the previous projection of 59.6 mmt. In contrast, corn planting progress has been promising. This advancement is due to sufficient rainfall, which has been favorable for the planting season.

The Brazilian corn market has been supported by a combination of firm external prices and a devalued currency of Brazilian Real (BRL) which has helped maintain vigorous export activity, considering the year's challenges. However, this situation has left some uncertainty about the size of carryover stocks. At the same time, the market is experiencing regional and seasonal peculiarities. Due to the turn of the year, logistics are limiting business flow in the short term, and some large consumers are already positioning themselves in terms of stockpiles for the period. As a result, the perception is that 2024 is essentially over for commercialization. With the crop's arrival in some Southern Brazil regions in mid-Jan-25, the market is expected to create an environment where it will be possible to purchase corn at lower prices in Jan-25 and Feb-25 while stocking up without significant difficulties. In line with tight supply scenarios, the domestic market is expected to act aggressively to manage expectations, ensuring that corn prices remain contained.

Ukraine exported nearly 1.7 mmt of corn as of December 23, with projections exceeding 2 mmt for Dec-24 despite initial shipment delays. Corn prices remained stable due to favorable market conditions, including limited United States (US) supply and weather concerns in Brazil and Argentina. Ukrainian corn dominates the European market, while US exports focus on Latin America and Mexico, offering Europe a USD 10 per metric ton (mt) price advantage.

The United States Department of Agriculture's (USDA) latest weekly export sales bulletin, released on December 27, revealed higher-than-expected figures for US corn. Sales for the 2024/25 harvest reached 1.711 mmt in W51, surpassing market projections of 1 to 1.6 mmt. Cumulative commitments for this season now total 38.023 mmt, significantly outpacing the 29.421 mmt recorded at the same time in 2023.

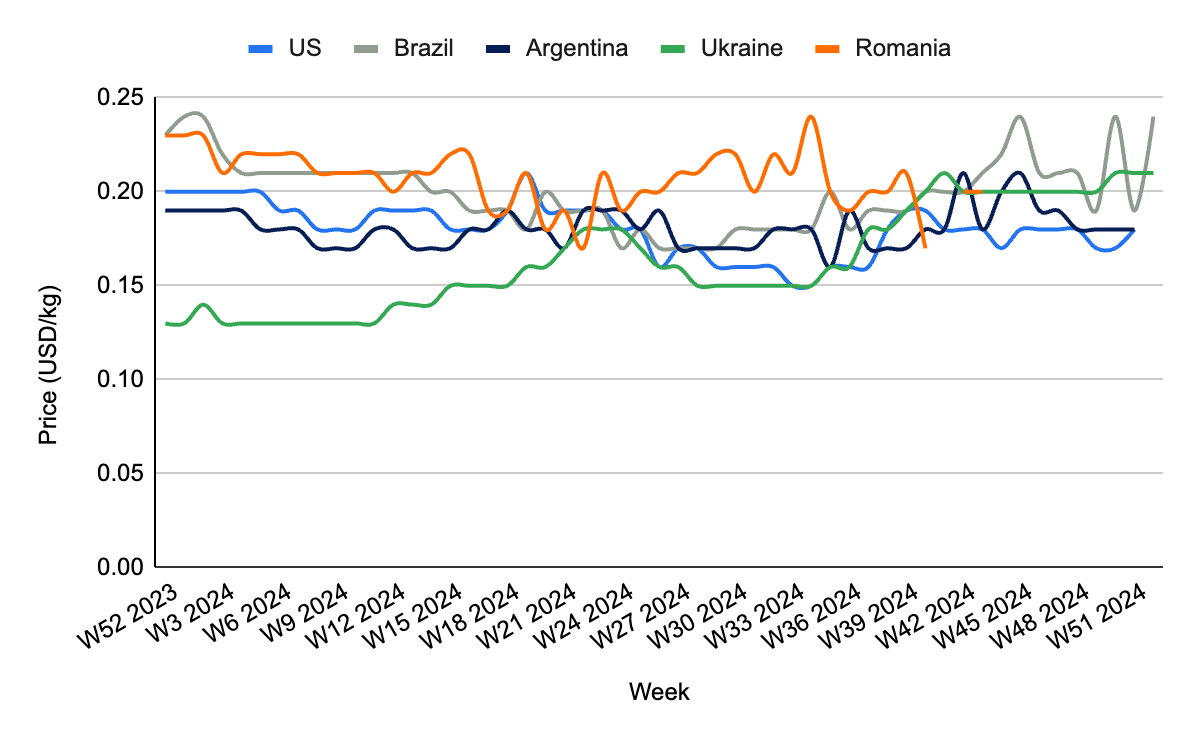

In W52, wholesale maize prices in Brazil increased significantly by 26.32% week-on-week (WoW), 26.32% month-on-month (MoM), and 4.35% year-on-year (YoY), reaching USD 0.24 per kilogram (kg). This surge is primarily due to severe drought conditions that intensified between May-24 and Aug-24, marking one of the most prolonged and most intense droughts in Brazil's modern history. The drought adversely affected maize production, leading to reduced yields and a tightening of domestic supply. Additionally, the Brazilian real (BRL) devaluation made Brazilian maize more competitive in international markets, increasing export demand.

Ukrainian wholesale maize prices remained stable WoW but increased by 5% MoM and saw a significant rise of 61% YoY in W52, reaching USD 0.21/kg. This price hike is primarily due to dry weather conditions that negatively affected crop yields, prompting the USDA to lower Ukraine's corn harvest forecast by 1 mmt to 26.2 mmt. Ukraine also faces a 13% YoY export decline through the Constanta Port, mainly due to its reliance on deep-sea ports for shipping. The Ministry of Agrarian Policy and Food confirmed that the harvest season has concluded with a total grain collection of 53.9 mmt. Although reduced exports typically put downward pressure on prices, logistical issues and transportation constraints have driven up costs, helping to keep maize prices elevated.

With Ukraine facing logistical challenges and Brazil dealing with seasonal transport limitations, stakeholders should optimize supply chains by securing alternative transportation routes or increasing port capacity. This involves building stronger relationships with logistic partners or investing in technologies like blockchain to improve traceability and streamline export processes. Enhancing logistical efficiency will reduce delays, lower transportation costs, and ensure timely delivery to key markets, maintaining the competitiveness of maize exports and avoiding disruptions to international trade.

In regions affected by drought or irregular rainfall, such as Brazil and Ukraine, stakeholders should invest in irrigation infrastructure and adopt climate-resilient farming practices. Techniques like drip irrigation, soil moisture management, and drought-resistant seed varieties, such as Monsanto’s DroughtGard or Pioneer’s P1573HR hybrid, can help mitigate the impact of unpredictable weather conditions. These varieties are engineered to withstand water stress, improve root systems, and ensure better yield stability under challenging environmental conditions. These investments will improve yield stability, reduce the effects of adverse weather events on maize production, and secure long-term profitability, ensuring more consistent supply for domestic and international markets.

In light of supply disruptions and price volatility in major maize-producing countries like Brazil, Argentina, and Ukraine, stakeholders should diversify their export markets. This could involve exploring emerging markets in Asia, such as India, China, and Vietnam, as well as in the Middle East, including countries like Turkey, Saudi Arabia, and the United Arab Emirates (UAE), where maize consumption is increasing. Strengthening regional trade agreements within these areas could also mitigate logistical challenges and broaden export opportunities. Expanding into new markets will reduce dependency on traditional markets like Europe and Latin America, ensuring a more resilient export portfolio. Moreover, strengthening regional networks can help circumvent logistical bottlenecks and maintain a steady flow of exports, ultimately supporting stable revenue streams despite global uncertainties.

Sources: Tridge, NoticiasAgricolas, UkrAgroConsult

Read more relevant content

Recommended suppliers for you

What to read next