Original content

The United States Department of Agriculture (USDA) reduced Argentina's 2024/25 soybean production estimate by 1 million metric tons (mmt) to 52 mmt due to high temperatures and limited rainfall, which stressed crop development. By late W3, farmers had planted 97% of soybeans and 95% of double-crop soybeans. However, dry conditions caused low plant populations and lowered crop ratings, with 8% of soybeans classified as poor/very poor, 43% as fair, and 49% as good/excellent.

The National Supply Company (CONAB) revised its domestic soybean production forecast for the 2024/25 season to a record 166.32 mmt, slightly higher than its previous estimate of 166.21 mmt. This marks a 12.6% year-on-year (YoY) increase from the 2023/24 harvest, driven by favorable weather and a slight expansion in the planted area. However, the forecast remains below other agencies' estimates, which range from 167 to 173 mmt.

According to the Mato Grosso Institute of Agricultural Economics (IMEA), early sales of the 2024/25 soybean crop in Mato Grosso have reached 45.2% of the projected total, up by 4% month-on-month (MoM). This pace surpassed the same period of the 2023/24 harvest of 38.18% but lags behind the five-year historical average of 51.59%. This coincides with the delayed soybean harvest in Mato Grosso due to late planting and excessive rainfall.

Soybean harvesting in Mato Grosso, Brazil's largest soybean-producing state, has begun slowly due to dry weather delaying planting earlier in the season. So far, only irrigated soybeans planted in early Sep-24 have been harvested. Despite this sluggish start, IMEA forecasts a record crop of 44 mmt, a 12.7% YoY increase driven by expanded acreage. However, persistent overcast skies and heavy rainfall pose risks to yields. Wet weather during the harvest could delay the start of dryland soybean harvesting and cause bottlenecks at grain elevators, potentially slowing overall harvest progress.

China achieved a record-breaking soybean import volume of 105.03 mmt in 2024, a 6.5% YoY increase. The growth was driven by declining Chicago Board of Trade (CBOT) soybean prices, strong crush margins, and concerns over potential trade tensions with the United States (US), prompting buyers to secure larger-than-usual shipments of US soybeans as a precaution. Although Brazilian soybeans were priced lower, Chinese importers prioritized US supplies to mitigate risks. Looking ahead, ample supplies and negative crush margins will reduce future demand for US soybean imports.

US soybean crushing set a record in Dec-24 as new mills became operational, with the National Oilseed Processors Association (NOPA) reporting a 6.9% MoM increase and a 5.8% YoY rise. The monthly crush reached 206.604 million bushels, exceeding the average estimate and breaking the previous record. Driven by new and upgraded plants, the expanded processing capacity has boosted NOPA members' projected crush to 2.215 billion bushels in 2024, a 4.4% YoY increase. Soybean oil stockpiles among NOPA members also hit a record high as of December 31, 2024.

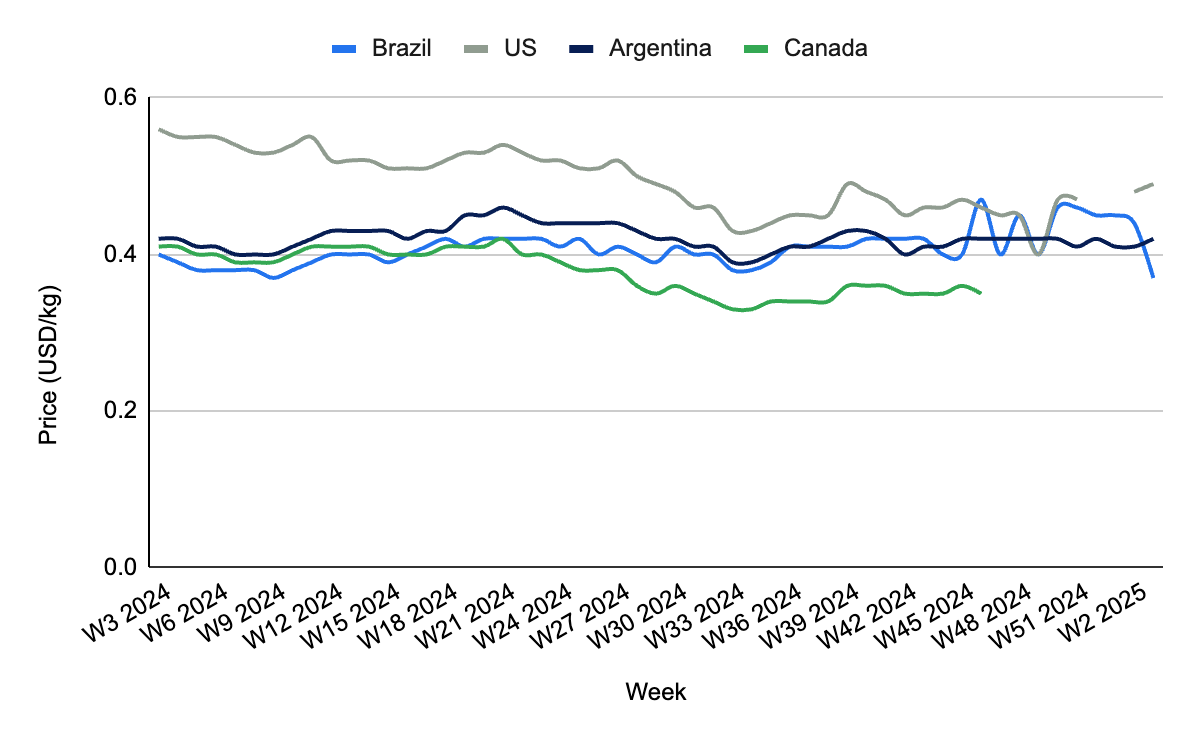

In W3, Brazilian soybean prices dropped by 15.91% week-on-week (WoW), 17.78% MoM, and 7.50% YoY, settling at USD 0.37 per kilogram (kg). This decline followed CONAB's revised domestic soybean production forecast for the 2024/25 season to a record 166.32 mmt, slightly up from its previous estimate of 166.21 mmt. The new forecast reflects a 12.6% YoY increase compared to the 2023/24 harvest, supported by favorable weather conditions and a modest expansion in the planted area. Despite the record outlook, CONAB's forecast remains below private consultancy estimates, which project production between 167 and 173 mmt.

In W3, US soybean prices rose by 2.08% WoW, reaching USD 0.49/kg from USD 0.48/kg. The USDA revised its soybean production forecast for the 2024/25 season downward to 2.58 mmt, which adjusted expected stock levels and drove prices higher. The lower production estimate is primarily due to a 1.93% YoY yield decline, resulting in tighter end-of-season stocks. According to the USDA, states most impacted by the reduced production include Indiana, Kansas, South Dakota, Illinois, Iowa, and Ohio.

In W3, Argentinian soybean prices rose by 2.44% WoW, reaching USD 0.42/kg. Despite the price increase, adverse weather conditions, including high summer temperatures and limited rainfall, have negatively affected soybean crop yields and quality. Moreover, the BAGE adjusted its 2024/25 planting estimates, reducing the projected soybean area by 200 thousand hectares (ha) to 18.4 million ha while increasing the corn area by 300 thousand ha to 6.6 million ha. This shift is driven by the declining profitability of soybeans, leading farmers to opt for more profitable alternative crops. Argentina's soybean production for the 2025 harvest is expected to range between 52 and 55 mmt, with weather conditions continuing to be a key factor in determining the final yield.

In W3, Uruguay's soybean prices held steady at USD 0.41/kg, supported by key factors such as favorable market conditions and the expansion of planting area. For the 2024/25 marketing year (MY), Uruguay's soybean planting area is projected to reach 1.3 million ha, a 19% increase from the five-year average. This growth is attributed to late-season soybean planting as producers brace for potential challenges from the La Niña weather pattern. The USDA forecasts Uruguay's soybean production for 2024/25 at 3.4 mmt, up from 3.2 mmt in the previous year due to favorable weather conditions. While Uruguay's soybean exports are expected to rise in 2024, the pace may slow in 2025 due to potential stagnation in global demand. Nevertheless, the steady export performance has helped maintain price stability in the domestic market.

Soybean producers in Brazil, Argentina, and Uruguay should consider locking in contracts or hedging their sales when market prices show positive movements, such as the recent uptick in Argentina and US prices. Given the fluctuating market trends, securing forward sales or negotiating contracts in advance of harvest could minimize exposure to price drops, particularly as supply and demand dynamics shift. Securing higher prices during peak market conditions can stabilize revenue and reduce the impact of future market corrections.

Delayed harvesting in Brazil and Argentina due to excessive rainfall and overcast skies highlights the need for exporters to enhance storage capacity and logistical capabilities. Investments in infrastructure (e.g., additional storage and better transport routes) will enable smoother post-harvest operations, prevent bottlenecks, and ensure timely exports. Improved infrastructure ensures efficient storage and transport, reducing the risk of delayed exports and providing flexibility during high-demand periods.

Producers and traders should closely monitor weather forecasts, especially in Argentina and Mato Grosso, where dry conditions and overcast skies affect crop development. To mitigate risks, it is crucial to adjust planting strategies, optimize irrigation, and prepare for possible harvest delays. By proactively managing weather-related risks, producers can reduce yield losses, optimize harvest timing, and prevent potential market disruptions. This approach will help ensure that crops are resilient to fluctuating weather conditions, safeguarding productivity and profitability.

Sources: Tridge, Hellenic Shipping News, NoticiasAgricolas, UkrAgroConsult

Read more relevant content

Recommended suppliers for you

What to read next