Original content

Australia's orange production for marketing year (MY) 2024/25 is forecasted to reach 545 thousand metric tons (mt), marking a 5% year-on-year (YoY) increase from the prior year's 520 thousand mt and the highest level in two decades. Favorable early seasonal conditions, including dry weather during fruit set and above-average rainfall supporting fruit growth, have contributed to this improvement. Orange export volumes are projected at 190 thousand mt, the third-highest on record, driven by increased production and high-quality fruit. Domestic consumption is expected to rise to 170 thousand mt, while the volume allocated for processing is forecast to decline by 3% to 195 thousand mt due to enhanced fresh fruit quality.

In 2024, Brazilian orange prices reached record highs, with fresh market values surpassing USD 16 per 40.8-kilogram (kg) box (BRL 100/40.8-kg box), driven by strong industry demand and limited fresh orange supplies due to reduced production. Persistent dry weather and high temperatures in the citrus belt affected crop development, while citrus greening disease or Huanglongbing (HLB) and low productivity increased costs for growers despite higher prices. Projections for the 2024/25 season estimate a harvest of 223.14 million boxes in São Paulo and the Triângulo Mineiro, a 3.4% rise from the September estimate but 27.4% lower than the previous season's production. With critically low orange juice stocks, production must rise significantly in the 2025/26 season to stabilize global supply.

China's orange production is forecasted to reach 7.62 million metric tons (mmt) in MY 2024/25, reflecting a slight decline from the previous year. This reduction is due to adverse weather conditions, including persistent rains in April and May, high temperatures in late summer, and cold weather during early spring that affected fruit-setting rates. Additionally, HLB disease has significantly impacted key growing regions, with Jiangxi and Guangxi provinces expected to see a 20% YoY decline in production. Despite these challenges, the total number of orange producers is increasing, partially offsetting production losses and contributing to the overall stability of China's citrus industry.

For MY 2024/25 , European Union (EU) orange production is projected to decline to just over 5.6 mmt, with Spain contributing approximately 50% of the total output. Despite increased orange supply in Spain, a sharp reduction in Italy's production has driven the overall decrease. Adverse weather conditions, including extreme heat, drought, frost, torrential rains, and rising farming costs, have significantly impacted citrus yields. Orange juice imports to the EU are expected to rise, primarily from Brazil and Egypt, while exports are likely to decrease due to reduced domestic supply. The United Kingdom (UK) remains the top destination for EU orange juice, accounting for over half of exports.

Spanish agricultural union Agrarian Association of Young Farmers of Andalusia (Asaja-Andalucía) has criticized citrus processors for purchasing juicing oranges at below-cost prices despite historically high orange juice futures market prices. Asaja-Andalucía claims processors are exploiting their dominant position by offering farmers prices that do not cover production costs, violating Spain’s Food Chain Law. Meanwhile, strong international demand for orange juice is being driven by low production in Brazil, caused by drought and diseases. However, this surge in demand has not translated into higher prices for farmers, who continue to face low returns. Asaja-Andalucía calls for government intervention to protect growers and ensure the profitability of domestic citrus production in Spain, urging scrutiny of imports from countries with lower production costs.

Florida’s orange production continues its decline, with Alico Inc., a major citrus grower, announcing its decision to wind down operations after the 2024 crop harvest. The company attributed the move to a 73% drop in production over the past decade, compounded by Hurricanes Irma, Ian, and Milton, which worsened damage from the citrus greening disease. Alico owns over 53 thousand acres, with about 3.4 thousand acres of citrus to be managed by third-party caretakers through 2026. The company plans to repurpose a quarter of its land for commercial and residential development. Florida’s orange forecast for the 2024/25 season is projected at 12 million 40.8-kg boxes, representing a 20% YoY decline. This highlights the persistent challenges confronting the state’s renowned citrus industry.

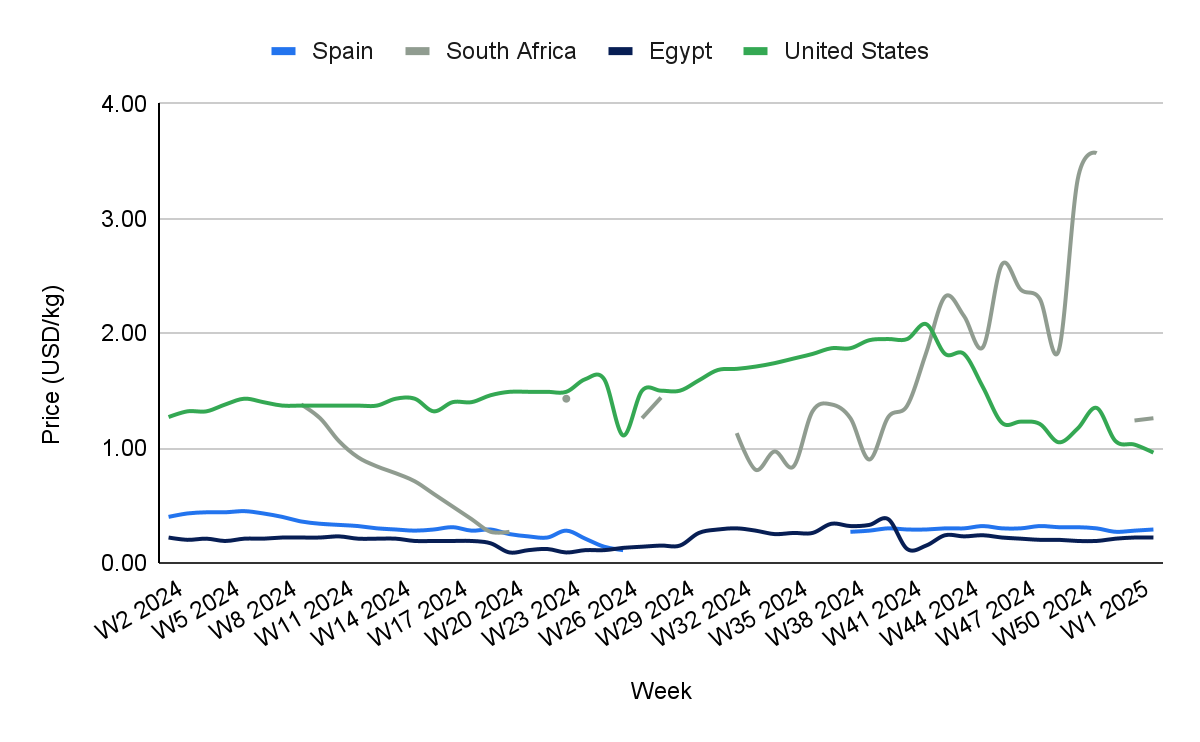

Orange prices in Spain slightly increased by 3.57% WoW to USD 0.29/kg in W2 due to strong international demand for orange juice, driven by low production in Brazil caused by drought and diseases, which created upward pressure on prices for fresh oranges. However, MoM and YoY prices dropped by 3.33% and 27.50%, respectively, due to below-cost prices offered by processors for juicing oranges, reflecting an imbalance in market dynamics. This price suppression, exacerbated by the dominant position of processors and competition from lower-cost imports, has prevented farmers from benefiting fully from the global surge in demand for orange juice.

South Africa's orange prices dropped significantly by 59.49% week-on-week (WoW) to USD 1.26/kg in W2, reflecting a 64.71% month-on-month (MoM) decrease. The price decrease is due to the current off-season period for oranges, as the next harvest is not expected until May. During this time, limited market activity and reduced demand for fresh oranges contribute to lower prices. Additionally, recent substantial rainfall in key growing regions such as Limpopo and Mpumalanga has improved crop conditions, leading to expectations of a strong harvest later in the year, which has further softened current prices. Internationally, the significant production shortfalls of 2024 have eased, and high orange juice prices have started to reduce demand. Consumer resistance to these high prices and competition from alternative beverages have also added downward pressure on orange prices in the domestic market.

In Egypt, orange prices remained steady at USD 0.22/kg in W2, with no WoW change due to balanced supply and demand dynamics during the seasonal peak of orange production in winter. Strong market activity supported stable pricing as domestic demand and favorable export opportunities continued to underpin the market. However, MoM prices increased by 15.79% due to strong consumer interest and export competitiveness, which have maintained elevated prices compared to previous months, despite ample supply levels.

Orange prices in the United States (US) dropped by 6.8% WoW to USD 0.96/kg in W2, reflecting a 28.89% MoM drop and a 24.41% YoY decrease. The price decline is due to a continued post-holiday lull in consumer demand and increased import volumes from California and other producing regions that have bolstered market supply. Florida's historically low orange production, impacted by hurricanes and citrus greening, remains a significant factor; however, imports have effectively compensated for these shortfalls. This expanded availability and reduced seasonal demand have amplified downward pressure on prices. Additionally, the oversupply of lower-cost imported oranges has also contributed to the sharp MoM and YoY price drops.

Italy's orange prices increased by 2.91% WoW to USD 1.77/kg in W2 due to steady local demand, particularly among Italian households, where oranges remain a staple fruit. The ongoing production challenges in Sicily, including drought and torrential rains, have contributed to limited supply, driving prices upward in the short term. Additionally, the market's preference for organic oranges, which have seen a notable rise in sales, has provided support for overall pricing. However, MoM and YoY prices dropped by 3.80% and 2.21%, respectively, due to increased competition from imported oranges, particularly from South Africa, which flooded the European market earlier in the season. This oversupply and moderate production levels in Spain and Italy have created a challenging pricing environment. Furthermore, while organic orange sales have grown, the segment still represents a smaller share of the market, limiting its overall impact on price stabilization.

Italian orange producers and exporters should strengthen supply chain efficiency by reducing post-harvest losses and ensuring timely market entry to compete with imported oranges. Highlighting the premium quality of Sicilian and organic oranges through targeted marketing can drive consumer preference and maintain pricing stability. Collaboration with retailers to promote local and organic options will increase demand and mitigate competition from imports.

US orange importers and distributors should optimize inventory management to prevent oversupply during periods of low consumer demand. Diversifying sourcing schedules and aligning import volumes with seasonal market trends can help maintain balanced supply levels, reducing downward pressure on prices.

EU orange juice processors and importers should increase sourcing from Brazil and Egypt to compensate for declining domestic orange production. Strengthening supplier relationships and ensuring logistics readiness can help meet rising demand and stabilize supply for key markets like the UK.

Sources: Tridge, Freshfruitportal, Freshplaza, Fruitnet, Nbcmiami, USDA

Read more relevant content

Recommended suppliers for you

What to read next