Original content

Since Dec-24 the global grape market has shifted with increased arrivals from South Africa, Namibia, and Peru creating a surplus. Although there were initial concerns about the grape quality from Peru's Piura region due to drought, no issues have been noticed so far. However, the increased supply has caused prices to drop, especially for loose grapes. Current prices range from USD 16.33 to 20.42 (EUR 16 to 20) for clamshell packs and USD 14.29 to 16.33 (EUR 14 to 16) for 4.5-kilogram (kg) boxes of white grapes. Red grapes are priced similarly, except for the more expensive Red Globe variety at USD 23.48 (EUR 23/4.5-kg box). Retail promotions are expected to boost consumption in the coming weeks, helping to balance the market after earlier price hikes caused by shortages.

The Brazilian table grape industry has remained resilient to climatic challenges, supported by a strong domestic market of over 215 million people. Despite heavy rains affecting harvests, growers ensure year-round production by using covered vines for sensitive varieties. Brazil’s unique climate enables production peaks in February to April and September to November, while reduced harvests during other months cater to local demand.

Chilean grape exports are running smoothly this 2024/25 season, supported by the resolution of a potential United States (US)’s port strike and steady shipments to major markets. Younger vineyards have driven a 5% production increase, marking a productive harvest in Dec-24 in Copiapó. Favorable conditions, including a frost-free winter, increased soil moisture, and a mild spring, supported this growth. Early varieties such as Sweet Celebration, Cotton Candy, and Sweetie have shown excellent quality, boosting strong demand in the US and Europe. While US grape prices remain stable or slightly higher, concerns over weaker demand in China may shift focus to other markets. The harvest is expected to conclude by April and has set an optimistic tone for stable pricing.

Peru, the world’s leading exporter of table grapes, managed to mitigate climate challenges in the 2023/24 campaign, exporting 525 thousand metric tons (mt) despite heavy rains and heat affecting fruit quality. For the 2024/25 campaign, exports are expected to reach a record 640 thousand mt, fueled by recovery in key regions like Ica and Piura and the adoption of high-yield seedless varieties like Sweet Globe and Autumn Crisp. With major US, Europe, China, and Latin America markets, Peru’s logistical advancements, including cold treatment during shipping, continue to enhance its export efficiency.

South Africa's grape export data through W52 reveals a 13.5% year-on-year (YoY) decline in inspected cartons for export, totaling 18.19 million 4.5 kg equivalent cartons. This drop is due to lower yields of early varieties in the Northern Provinces and Orange River regions. Despite this, exports increased by 20% YoY, reaching 11.86 million cartons. The national crop estimate stood at 76.4 million cartons, a 1% YoY rise from the prior season.

The top varieties exported in W52 included Prime, Midnight Beauty, and Evans Delight. The Orange River region packed 13.78 million cartons, an 8% decrease from last year, with Sweet Celebration, Sweet Globe, and Timpson leading production. The Northern Provinces packed 3.37 million cartons, down 15%. While all regions faced delays in early variety harvests, mid- and late-season packing remains on track, with producers reporting high-quality harvests.

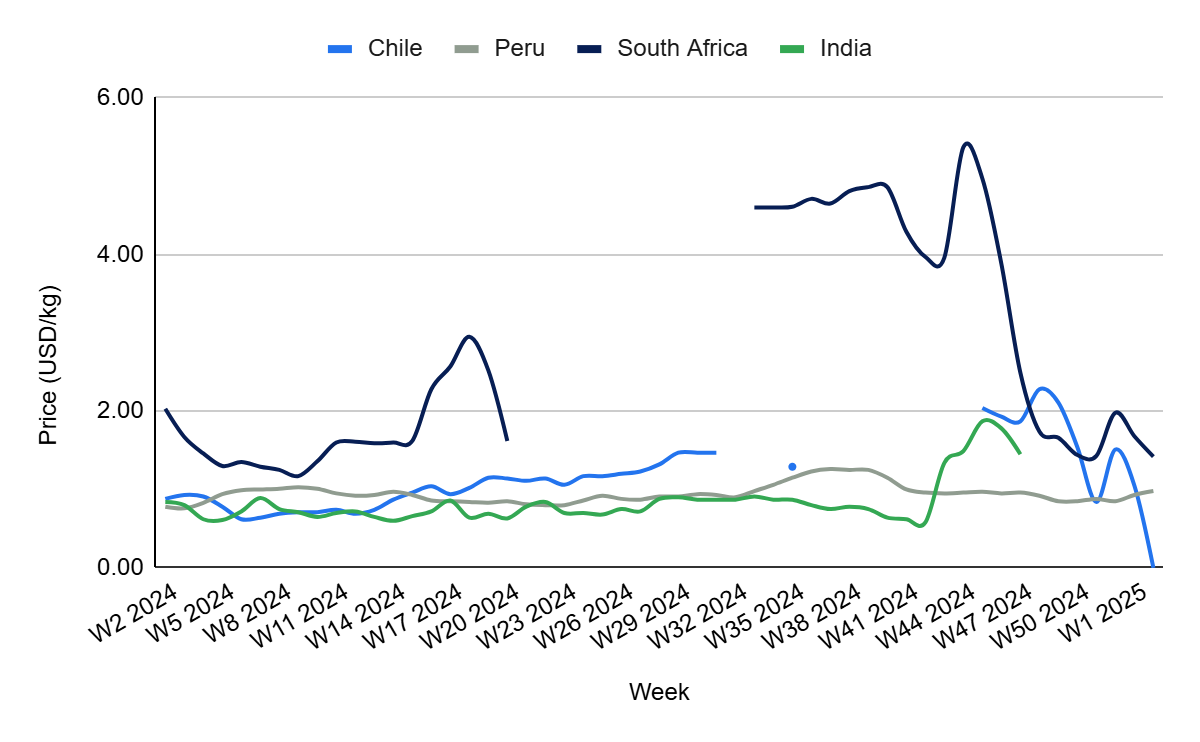

Chile's grape prices increased by 4.76% week-on-week (WoW) to USD 1.10/kg in W2, with a 25% YoY rise due to the continued strong international demand, particularly from the US, where supply shortages from California have supported Chilean exports. Additionally, the introduction of the Systems Approach for exports has further supported price growth. However, month-on-month (MoM) prices dropped by 27.63% due to the typical post-holiday dip in demand and the seasonal transition to the new harvest, which temporarily increased supply levels, putting downward pressure on prices.

Peruvian grape prices increased by 5.38% WoW to USD 0.98/kg in W1, reflecting a 12.64% MoM and 25.64% YoY increase due to the expected recovery in key regions like Ica and Piura, which have led to improved fruit quality despite the challenges of the previous campaign such as such as adverse weather conditions, pest or disease outbreaks, or logistical hurdles that affected production and quality. The adoption of high-yield seedless varieties such as Sweet Globe and Autumn Crisp has further boosted production. Additionally, strong demand from major markets such as the US, Europe, China, and Latin America, along with Peru's continued advancements in logistical efficiency, including cold treatment during shipping, has helped support higher prices.

South Africa's grape prices dropped by 15.48% WoW to USD 1.42/kg in W2, reflecting a decline of 0.70% MoM and a 30.05% YoY decrease. The price drop is due to a reduction in early variety yields in the Northern Provinces and Orange River regions, leading to delayed shipments. While the overall export volume increased by 20% YoY, the delayed early harvests contributed to a temporary oversupply of later varieties, which put downward pressure on prices. The delayed harvests and shifts in supply have led to a mismatch in market timing, contributing to the price decline. However, mid- and late-season varieties, particularly those from the Orange River and Northern Provinces, are expected to maintain high quality and steady production, which could help stabilize prices later in the season.

Grape exporters should adjust their pricing strategy to mitigate the effects of the surplus created by increased arrivals from South Africa, Namibia, and Peru. They should consider offering retail promotions, especially for clamshell packs and 4.5 kg boxes of white grapes, to drive consumer demand and balance the market. Exporters should work closely with retailers to implement targeted promotions and optimize the pricing structure to maintain competitiveness in the face of fluctuating supply levels.

Chilean grape exporters should focus on diversifying their markets in response to potential weaker demand in China. By prioritizing shipments to stable markets like the US and Europe, where demand for early varieties remains strong, they can maintain a balanced export portfolio. Additionally, exporters should leverage favorable harvest conditions and high-quality varieties to create targeted marketing campaigns that emphasize the unique qualities of Chilean grapes, strengthening their position in key markets.

Sources: Tridge, Eastfruit, Freshplaza, MXfruit, Portalfruticola, SATI, Simfruit, Windhoek Observer

Read more relevant content

Recommended suppliers for you

What to read next