Original content

In the 2024/25 marketing year (October to September), Australia’s wheat production is anticipated to substantially increase year-on-year (YoY), driven by favorable weather on the East Coast and improved rainfall in Western Australia. The Australian Bureau of Agricultural and Resource Economics (ABARES) forecasts production at 31.9 million metric tons (mmt), a 23% increase YoY. Despite the optimistic outlook, quality concerns persist, as late Nov-24's heavy rains delayed harvests and affected parameters like test weight. While Western Australia experienced less severe impacts, significant rainfall events on the East Coast have raised challenges, according to trade sources.

The port of Rouen, Europe's largest wheat export hub, experienced a significant drop in milling wheat exports during the week ending December 25, with less than 10 thousand metric tons (mt) shipped compared to 35,900 mt in W50 2024. The reduction is due to high French wheat prices, making Russian wheat a cheaper alternative. Slowed export activities during the French holiday season also contributed to the reduction. Moreover, adverse weather led to France's lowest wheat harvest in 40 years, further constraining exports. Despite these challenges, Rouen managed to ship 5.76 mmt of milling wheat during the 2023/24 season, with Morocco and Algeria as key destinations.

Kazakhstan's wheat import ban, which was in place from August 21 to December 31, 2024, has been officially lifted as of January 1, 2025. During the ban period, imports from third countries and the Eurasian Economic Union (EAEU) were restricted, with only transit shipments allowed. Considering the current state of the grain market, the Ministry of Agriculture will now focus on implementing non-tariff measures to manage imports. These measures aim to protect local producers from potential market distortions while preventing illegal wheat trade activities.

Morocco introduced a new subsidy system for soft bread wheat imports, effective from January 1 to April 30, 2025. Coordinated by the ministries of economy and agriculture, the subsidy system aims to financially support traders, cooperatives, and mills importing soft wheat for human consumption. According to Morocco's National Office of Cereals and Legumes (ONICL), importers will receive a one-time payment to bridge the gap between the average port price of wheat for the month and USD 267.55/mt. The average price calculation will use the two lowest prices of imported wheat from countries like Germany, Argentina, France, and the United States (US), provided the price difference does not exceed USD 29.73/mt.

According to the Ministry of Agrarian Policy and Food of Ukraine (MAPFU), the country exported 3.132 mmt of grain and leguminous crops in Dec-24 (2024/25 MY), marking a significant 54.4% YoY drop, equivalent to 1.704 mmt less than in 2023/24 MY. Wheat exports in Dec-24 fell to 700 thousand mt, a decline of 108.4% YoY.

The Department for Environment, Food and Rural Affairs (DEFRA) has reported a decline in the United Kingdom's (UK) 2024 wheat production compared to the previous year and the five-year average. The wheat harvest experienced a 20% YoY decrease to 11.1 mmt, with both the sown area and yields falling by 10% from the five-year average. This marks the weakest wheat harvest since 2020, primarily due to adverse weather conditions impacting crop growth and reducing overall yields.

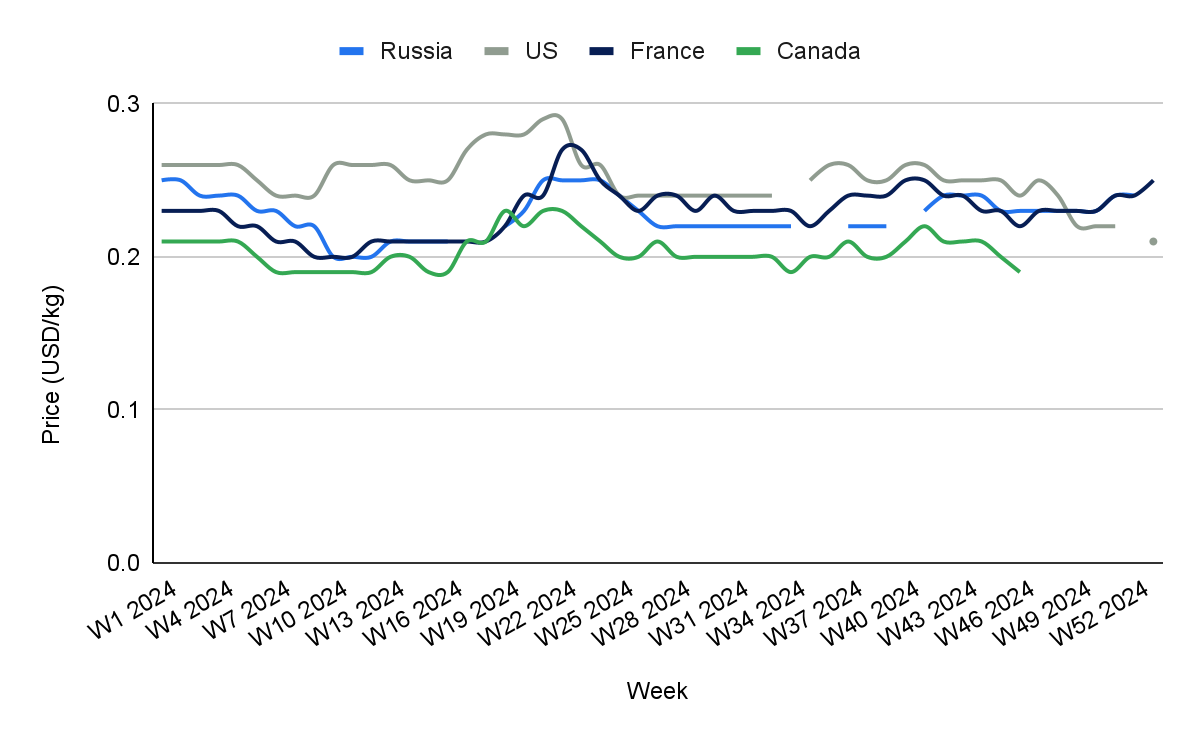

In W1, US wheat prices stood at USD 0.21 per kilogram (kg), a decline of 4.55% month-on-month (MoM) and 19.23% YoY. This decrease is primarily due to expectations of record global wheat supplies and a strong US dollar (USD), which have exerted downward pressure on prices. The United States Department of Agriculture (USDA) forecasts the US wheat crop to increase 11% YoY in 2024, totaling approximately 2 billion bushels. This abundant supply has contributed to the price decline. Moreover, strengthening the USD has made US wheat exports more expensive, potentially reducing demand from major importers such as the Philippines, Mexico, and Japan.

French wheat prices rose by 4.17% week-on-week (WoW) in W1, reaching USD 0.25/kg, with an 8.70% increase MoM and YoY. This upward trend is due to strong export demand, particularly from North African countries like Morocco, which have opted for French wheat due to poor local harvests and ongoing import support programs. Tightened domestic supply due to lower carryover stocks and increased miller purchases during the holiday season further fueled the price surge. Additionally, while Russia’s competitively priced wheat has intensified global market competition, logistical constraints, and buyer preferences in key markets have favored French exports. Currency fluctuations also played a significant role in enhancing the competitiveness of French wheat in international markets.

In W1, Ukrainian wheat prices remained stable WoW and MoM at USD 0.24/kg but rose 14.29% YoY. This price increase is primarily due to reduced wheat production in major exporting countries, such as Russia and the European Union (EU), leading to a more competitive market for Ukrainian wheat. For instance, Russia's 2024 wheat harvest decreased by 10 mmt compared to the previous year, and the EU also experienced a smaller harvest, resulting in less wheat available for export. Furthermore, Ukraine's wheat exports have been robust, with significant sales to countries like Egypt, which purchased 120 thousand mt of Ukrainian wheat in 2024.

Wheat-exporting countries like Australia, France, and Ukraine can reduce dependency on traditional export markets by expanding their reach to emerging markets where wheat consumption is rapidly growing. For instance, Australia could target Southeast Asian countries like Indonesia, where wheat demand is rising due to increasing population and changing dietary habits. Australian varieties, such as Durum wheat and APW (Australian Prime Hard) wheat, could cater to this emerging market’s preferences for high-quality grains suitable for local baking. Similarly, France could explore markets like Thailand, where premium milling wheat is in demand for bread-making. French soft wheat varieties, known for their excellent baking properties, would align well with the needs of Thai consumers seeking high-quality flour. Moreover, Ukraine could focus on Sub-Saharan Africa, where wheat consumption is growing as a staple food. The country’s soft wheat varieties, known for their adaptability to different climatic conditions, could help meet the demand in these emerging regions, fostering stronger trade ties and ensuring a more stable export portfolio.

For wheat-producing nations like France and Ukraine, maintaining competitiveness in the global market hinges on improving the quality of their wheat. For example, France can enhance its wheat production by investing in cutting-edge breeding programs that create high-yield, disease-resistant, and drought-tolerant wheat varieties. By developing soft wheat strains, such as those used in baking, farmers can achieve higher protein content and milling quality, which is essential for meeting international buyers' stringent quality standards. Likewise, Ukraine has the potential to boost its wheat quality by adopting advanced seed technologies, specifically those bred for resilience against extreme weather conditions like drought and heavy rainfall. Ideal for baking and milling, soft wheat varieties would improve yields and ensure that the wheat produced is of high quality, meeting the demands of both domestic and global markets. Investing in these breeding programs can significantly enhance wheat quality, providing farmers with the tools to adapt to changing climate conditions and produce more reliable crops.

Efficient supply chains ensure that wheat reaches international markets on time and cost-effectively. In France, upgrading storage facilities would be a key step in preventing quality degradation during transit. State-of-the-art silos, equipped with temperature and humidity control systems, would help preserve the integrity of the wheat. These would be particularly crucial during periods of heavy rainfall, which can lead to spoilage. By ensuring better handling and long-term storage, France could minimize losses and meet the demands of export markets more effectively. Improving rail and port infrastructure in Ukraine is critical to reducing logistical bottlenecks that currently hinder efficient wheat exports. Upgrading these systems would allow smoother transportation and quicker shipment times, lowering costs and preventing delays that could compromise wheat quality. Moreover, introducing digital solutions such as global positioning satellite (GPS) tracking for shipments and better inventory management systems would enhance overall transparency and streamline the supply chain, ensuring that wheat is transported efficiently from farms to international markets. Such advancements would reduce losses and foster excellent reliability in fulfilling export commitments.

Sources: Tridge, Agrotimes, : Foodmate, Hellenic Shipping News, Sinor, UkrAgroConsult

Read more relevant content

Recommended suppliers for you

What to read next