Original content

In 2024, the dairy industry in Western Europe faced significant challenges impacting milk production. Disease outbreaks, including Bluetongue Virus (BTV-3) in Northwestern Europe and Epizootic Hemorrhagic Disease (EHD) in Spain and France, caused temporary reductions in milk output, fertility issues, and increased mortality rates. These diseases continued to affect production, leading to smaller herd sizes. Additionally, strict environmental regulations, such as restrictions on manure use in the Netherlands and nitrates exemptions in Ireland, forced farmers to reduce herd numbers to comply with new laws. Rainy weather during the spring and early summer of 2024 further exacerbated the situation, forcing farmers to keep cattle indoors, which reduced production in countries like France, Germany, the Netherlands, and Belgium. These nations faced the most significant losses in dairy cattle numbers.

As of November 3, 2024, Germany's livestock sector reported 10.5 million cattle, including 3.6 million dairy cows, marking a decrease of 1.6% in overall cattle numbers and 2.1% in dairy cows compared to May-24. Compared to Nov-23, the cattle population dropped by 3.5%, with dairy cow numbers decreasing by 3.3%. Additionally, the number of farms with dairy cows continued its long-term decline, falling by 1.6% from May-24 to 48,600 farms and down by 3.8% compared to Nov-23.

In 2025, Irish dairy farming is projected to experience a 4% increase in milk production, driven by improved yields and a stable land base. While production costs remain elevated, the forecasted improvement in the annual average milk price (5% increase) and stable feed prices will enhance margins. Feed expenditures are expected to drop by 9%, and fertilizer prices are forecast to decrease by 5%. The average net margin per hectare (ha) is estimated to increase by 35% and per liter (L) margins by 29%. Despite the high-cost environment, favorable milk prices and normal weather conditions will improve profitability.

As of Oct-24, the number of dairy farmers in Japan fell to 9,960, marking a 5.7% decrease from the previous year and dropping below 10,000 for the first time since 2005. The decline has accelerated since 2022, mainly due to worsening business conditions driven by a weak yen and high crude oil prices, which have increased production costs. An online survey revealed that 58.9% of farmers reported being in deficit, with 47.9% considering leaving the industry. Factors cited for financial struggles included rising feed, equipment, and utilities costs, alongside falling income from milk and cow sales. Despite the economic challenges, 98% of consumers wanted to continue purchasing domestically produced milk, though many were unaware of the industry's struggles.

According to the French Chamber of Agriculture, Poland is the only European country with favorable conditions for continued growth and increased milk production over the next decade. ºBolstered by modernization and restructuring since joining the European Union (EU) in 2004, Poland’s milk industry is thriving, with milk production rising nearly 30% from 2013 to 2022. Polish dairy farmers can increase productivity without expanding herd sizes, presenting a positive outlook for the sector.

In contrast, other European nations, including the Netherlands, Germany, and Italy, have seen declines in dairy cattle populations over the past decade. The trend is expected to worsen, with forecasts suggesting a 13 to 20% drop in Northern European milk production by 2035. Factors contributing to these declines include climate anomalies, fluctuating milk prices, and stricter environmental and animal welfare standards.

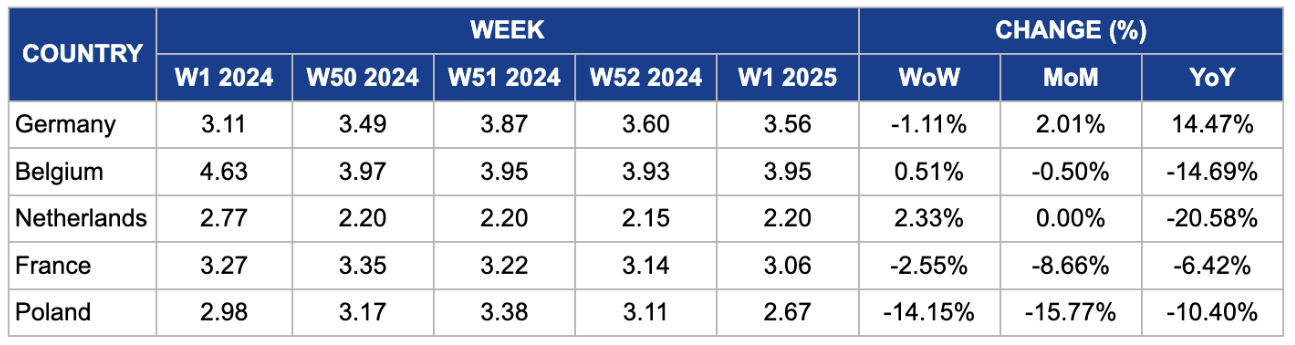

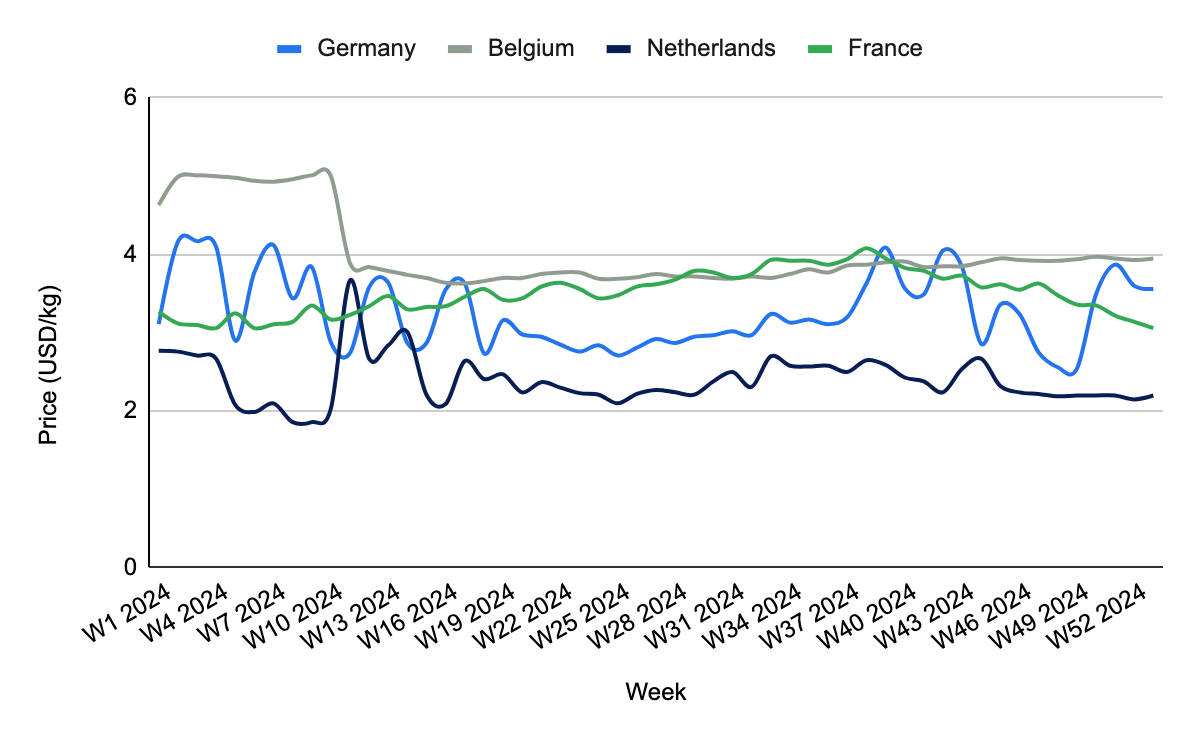

In W1, Germany's milk prices stood at USD 3.56 per kilogram (kg), marking a 1.11% week-on-week (WoW) decline following peak pricing of USD 3.87/kg in W51, as prices adjusted after the seasonal spike. Despite this short-term drop, prices rose 2.01% month-on-month (MoM) and 14.47% year-on-year (YoY), driven by tight supply conditions. The reduction in Germany's dairy cow population, down 3.3% YoY to 3.6 million as of Nov-24, and seasonal declines in milk yields significantly constrained output. Additionally, adverse weather and stricter environmental regulations across key European producers like France, the Netherlands, and Belgium amplified supply pressures, keeping prices elevated despite the recent adjustment.

In W1, Belgium's milk prices stood at USD 3.95/kg, reflecting relative stability with a slight 0.51% WoW increase and a minor 0.50% MoM decline. However, despite ongoing supply pressures, prices have dropped significantly by 14.69% YoY. The reduction is attributed to weakened demand dynamics and improved supply chain efficiency, mitigating some of the seasonal challenges. Additionally, Belgium faced supply constraints similar to those of neighboring countries, including reduced dairy cow populations and lower milk yields due to adverse weather and stricter environmental regulations. These pressures did not prevent the notable YoY price decline, highlighting changing market conditions.

In W1, milk prices in the Netherlands reached USD 2.20/kg, reflecting a 2.33% WoW increase due to market adjustments addressing low short-term supply. MoM prices remained stable despite ongoing supply challenges, including stricter environmental regulations that forced farmers to reduce herd sizes. However, YoY prices dropped significantly by 20.58%, primarily attributed to the country's persistently high milk supply levels. The Dutch government has implemented schemes to address this overproduction in the next few months. Still, the oversupply continues to exert downward pressure on prices, overshadowing the impact of reduced herd numbers and stricter regulations.

Milk prices in France have continued their downward trajectory, declining to USD 3.06/kg in W1 2025, reflecting a 2.55% WoW, 8.66% MoM, and 6.42% YoY decrease. This negative trend, persisting since the last quarter of 2024, is essentially a market correction following higher prices earlier in 2024 despite reduced supply levels. Disease outbreaks, including BTV-3 and EHD, caused fertility issues, reduced herd sizes, and tightened supply. Additionally, rainy weather during the spring and early summer of 2024 forced cattle indoors, lowering production efficiency. These conditions initially drove prices higher but have begun to normalize, resulting in the current decline.

Milk prices in Poland fell to USD 2.67/kg in W1, reflecting a sharp 14.15% WoW, 15.77% MoM, and 10.40% YoY decline. This drop follows a peak in W51 2024, signaling a correction in the market. Poland's dairy industry is positioned for long-term growth, contrasting with declines in other European nations. Since joining the EU, favorable conditions, including modernization and restructuring, have driven production up. Unlike neighboring countries grappling with reduced cattle populations, climate anomalies, and stricter environmental standards, Poland has maintained productivity growth without herd expansion. These dynamics underpin Poland's resilience amid fluctuating prices, highlighting its potential for sustained growth in the European dairy market, and are pushing prices downwards.

With significant declines in dairy cattle populations across Germany, France, and the Netherlands, sourcing from markets with stable or growing dairy sectors like Poland is a strategic opportunity. Importers and processors should diversify supply chains to mitigate risks of disruptions due to fluctuating herd sizes or disease outbreaks. Establishing relationships with Polish dairy producers can help maintain a consistent milk supply and reduce dependency on volatile markets.

The dairy industry in Europe is facing challenges from disease outbreaks, regulatory changes, and climate conditions. To combat these pressures, investment in farm management technologies, such as precision farming tools, can boost productivity. Implementing systems that optimize feed usage, monitor animal health, and improve yield management can help dairy farmers adapt to changing conditions and reduce operational costs. Technological advancements will be crucial in stabilizing production and ensuring competitiveness in the market.

Poland’s dairy sector, which has seen growth in milk production despite challenges in other European countries, presents a valuable opportunity for stakeholders seeking to expand their dairy sourcing. With favorable market conditions and modernized farming techniques, Poland’s industry is well-positioned for growth. Stakeholders should focus on long-term partnerships with Polish producers, exploring opportunities to increase milk production and enhance supply chain stability in response to challenges facing other European markets.

Sources: Tridge, Agri Holland, Agro News GR, AVMA, Farmer PL, Nippon, The Cattle Site

Read more relevant content

Recommended suppliers for you

What to read next