Original content

Argentina has finalized its 2024/25 soybean harvest, yielding a total of 50.3 million metric tons (mmt), according to the Buenos Aires Grain Exchange. This final output represents a slight increase of 100,000 metric tons (mt) compared to the previous season. The harvest campaign was marked by challenging weather, including a summer drought and heatwave. However, beneficial autumn rains helped yields recover, allowing for a stable production outcome. The planted area of 17.3 million hectares, the largest since the 2015/16 season, helped offset losses resulting from extreme weather conditions. As the world's leading exporter of soybean oil and meal, the conclusion of Argentina's harvest is a key factor for global markets. The country's production, while solid, remains below the record high of 60.8 mmt set a decade ago.

Brazil's soybean sector is poised for record-breaking growth in the 2025/26 season. According to a recent United States Department of Agriculture (USDA) report, the planted area is projected to increase by 3% to 49.1 million hectares. This expansion is expected to boost production to a new high of 176 mmt, up from 169.5 mmt in the previous season. The optimistic forecast is driven by strong global demand, favorable weather conditions, and an anticipated increase in average yields to 3.58 metric tons (mt) per hectare. Furthermore, discussions around relaxing the Amazon Soy Moratorium could unlock significant additional land for cultivation. The report also highlights a growing trend towards domestic processing, with the soybean crush projected to reach 58 mmt. This is fueled by rising demand for animal feed and an upcoming biodiesel mandate, indicating a shift towards adding more value within Brazil's economy.

Brazil is tightening its grip on China's massive soybean market, further sidelining United States (US) suppliers. In the first quarter of 2025, Brazil's soybean exports to China rose by 7% to 16.9 mmt, while May saw a staggering 37.5% year-on-year (YoY) jump to 12.11 mmt. This surge builds on a dominant position established in 2024, when Brazil supplied 71% of China's total soybean imports. A new trade agreement between the two nations is expected to intensify this relationship, placing additional pressure on the US, whose market share in China has fallen below 30%. With Brazil's agricultural sales to China already exceeding USD 60 billion in 2023, economists warn that the US must urgently diversify its export markets to mitigate the growing competitive threat.

Canadian farmers have slightly increased their soybean plantings in 2025, with the total area rising by 0.5% to 5.7 million acres, according to a recent Statistics Canada report. This increase is part of a broader trend that saw farmers pivot away from canola and barley towards wheat, corn, and pulses. The national soybean figures mask significant regional shifts. Quebec reported a record 1.1 million acres, a 4.4% increase, while Manitoba saw a substantial 13.0% jump to 1.6 million acres. In contrast, Ontario, the largest soybean-producing province, reduced its plantings by 7.4% to 2.9 million acres. These varied strategies reflect differing regional weather conditions, with warm, dry weather in the Prairies expediting seeding, while cooler, wetter conditions in the East caused some delays.

The US is making a strategic push to solidify its position in Nigeria's soybean market, aiming to fill a widening supply gap. After a six-year hiatus, the US resumed exports to Nigeria in 2024, shipping 64,000 mt. This initiative is timely, as Nigeria's domestic soybean production has fallen by 14% over the last three years, failing to keep pace with rising demand for protein. To foster these trade relations, the US Soybean Export Council recently hosted a major conference in Lagos, bringing together key stakeholders from Nigeria's agricultural sector. With Nigerian farmers facing challenges like regional insecurity, the US sees a significant opportunity to become a primary supplier. This move aims to secure a mutually beneficial partnership, addressing Nigeria's protein needs while opening a valuable new market for American soybean producers.

The latest USDA reports indicate a decrease in US soybean plantings for 2025, with acreage adjusted down to 83.38 million acres, a 4.2% decline from the previous year. This figure came in slightly below analyst expectations. Despite the smaller planted area, soybean stocks as of June 1 were robust, totaling 1.01 billion bushels, up 4% from the same time last year and higher than market forecasts. The increase was driven by an 18% rise in off-farm stocks, which offset a 12% decline in on-farm holdings. Meanwhile, the development of the 2025 crop is progressing steadily. As of early Jul-25, 96% of the soybean crop had emerged, 32% was blooming, and 8% was setting pods, slightly ahead of the five-year average. Crop conditions remain mostly positive, with 54% of the nationwide crop rated as good and 12% rated as excellent.

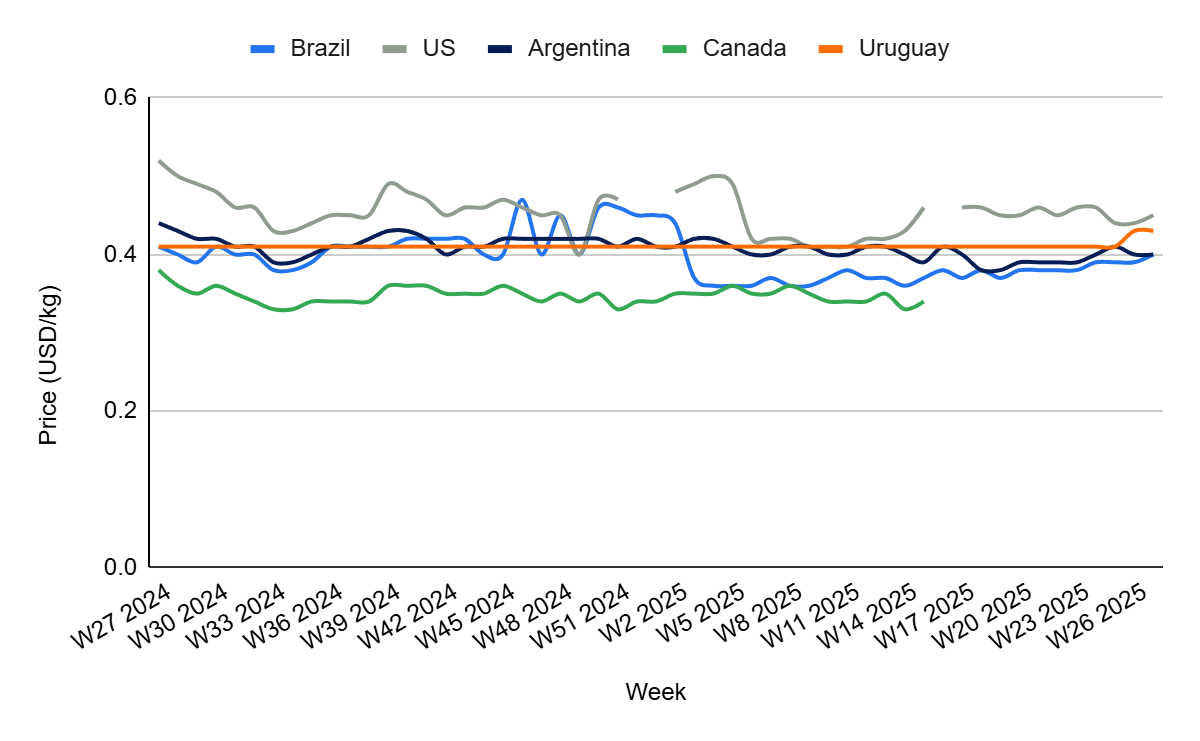

In W27, Brazil’s soybean price increased 2.56% week-on-week (WoW) to USD 0.40 per kilogram (kg), bringing the total increase over the past month to 2.56%. However, this price is still 2.44% down from the USD 0.41/kg compared to W27 2024. The short term increase can partly be attributed to robust demand from China. Ongoing trade friction with the US solidifies Brazil's position as the preferred supplier, leading to strong export premiums and supporting prices at the source. Furthermore, recent policy announcements in Brazil and the US supporting higher biofuel blending have created a positive demand shock for soybean oil, which in turn lifts the entire soybean complex globally. The YoY reduction in price can largely be attributed to high planted area and production in Brazil, recovering production in Argentina and high global stock levels, all of which put downward pressure on prices.

In W27, US soybean prices are also up, increasing 2.27% WoW to USD 0.45/kg. However, prices are down 2.17% over the past month and are down 13.46% since the same time last year. The modest weekly gain is largely attributed to two recent developments. First, a weather premium is being factored into the market as the US crop enters a critical growth stage in July, with increasing heat raising concerns about final yields. Second, a recent EPA announcement supporting higher biofuel blending mandates has created a positive demand shock for soybean oil, lifting the entire soybean complex.

The price decline compared to a month ago is a result of a fundamentally well-supplied domestic market. Favorable weather throughout Jun-25 has led to excellent crop conditions, with development slightly ahead of the 5-year average. This strong progress, combined with a June 1 stocks report showing inventories that were 4% higher than last year, has capped prices and exerted downward pressure throughout the past month. Meanwhile, the substantially lower YoY price can be attributed to ample domestic stocks, high global stock levels as well as intense export competition in major markets such as China.

In W27 in Argentina, prices are remaining steady at USD 0.40/kg with no significant changes during the past month. However, prices are still down 9.09% compared to the same time last year. The 2024/25 harvest season in Argentina has come to a close with a yield of 50.3 mmt. With the domestic supply now known and factored into the market, there are no new immediate supply shocks to drive prices in either direction. The market is in a "wait-and-see" phase. The substantial drop in prices compared to this time last year is the result of a much-improved supply situation, both domestically and globally. The 2024/25 harvest marks a significant recovery from the previous season, which was severely impacted by drought. This rebound in domestic production has added considerable volume to the market compared to the previous year, naturally pressuring prices downward. Furthermore, the large harvest in neighbouring Brazil is also putting pressure on Argentine soybean prices.

In W27, Uruguay’s soybean prices have remained stable over the past week but are up 4.88% month-on-month (MoM) and up by the same percentage compared to the same week last year. The Uruguayan price is slightly higher compared to its South American neighbours, demonstrating significant price strength. This trend suggests that Uruguay is largely insulated from the global oversupply that is depressing prices in Brazil and Argentina, likely due to a combination of a smaller, more specialized supply and strong, consistent export demand. Uruguay has a very strong trade relationship with China, which purchased nearly 80% of its soybean exports in 2024. This consistent, high-volume demand from a single major buyer is beneficial in the current environment where China is moving away from US soybeans in favour of South American soybeans.

With Brazil solidifying its role as China's primary soybean supplier, it is imperative for the US to pivot its export strategy away from over-reliance on a single market. The recent initiative to re-engage with Nigeria, a nation with falling domestic production and rising protein demand, serves as an excellent template. The US Soybean Export Council (USSEC) should aggressively replicate this model in other high-potential regions, particularly Southeast Asia (e.g., Vietnam, Indonesia) and North Africa. This involves investing in relationship-building, hosting targeted trade conferences to understand local needs, and promoting the quality, sustainability, and reliability of US soy. By proactively developing a diversified portfolio of smaller, growing markets, the US can build a more resilient export program that mitigates the risk of Chinese market concentration and provides long-term stability for its farmers.

For major producers like Brazil and Argentina, competing solely on the export of raw soybeans in an oversupplied market will lead to diminishing margins. A strategic shift towards enhancing domestic value-added processing presents a significant opportunity. By increasing local crushing capacity, these nations can capture more of the value chain, converting raw beans into higher-margin products like soybean meal and oil. Brazil is already leveraging this with its growing biodiesel mandate, creating a stable domestic demand floor. Argentina, already the world's top soymeal and oil exporter, should focus on modernizing and expanding this infrastructure. This strategy not only increases profitability but also diversifies revenue streams, making the agricultural sector less vulnerable to the price volatility of a single raw commodity and better equipped to serve both food and energy markets.

Uruguay's ability to command higher prices demonstrates the value of market differentiation. For producers in other regions, especially those in Canada or specific areas of the US and Argentina, a focus on specialized, high-premium niche markets offers a path to greater profitability. This involves a deliberate move to cultivate non-Genetically Modified Organism (GMO), organic, or identity-preserved (IP) soybeans. These products meet specific consumer demands in discerning markets like the European Union and parts of Asia, commanding higher and more stable prices than bulk commodity soybeans. Success requires investment in certification, traceability systems, and building direct relationships with buyers. By emulating Uruguay's model of targeted, high-quality supply, producers can insulate themselves from the price pressures of the commodity market and build a more sustainable and profitable business.

Sources: Tridge, UkrAgroConsult, Ecofin Agency, USDA, Beefweb, Successful Farming

Read more relevant content

Recommended suppliers for you

What to read next