News

Original content

Carbon markets offer a significant opportunity for livestock farming in Latin America. This is particularly through carbon sequestration in pastures, which supports climate change mitigation while potentially attracting substantial investment. At a seminar hosted by the Inter-American Institute for Cooperation on Agriculture (IICA) and key industry partners, experts emphasized the need for collaboration among governments, producers, and the private sectors to unlock this potential. Costa Rica shared its pioneering payment-for-results model, aiming to compensate small-scale ranchers for soil carbon capture. Experts stressed the importance of developing regulatory frameworks, financing mechanisms, and standardized sustainability indicators across the region. With Latin America producing 23% of global meat and around 12% of milk, the region’s livestock sector holds significant weight, but remains challenged by inconsistencies in sustainable livestock definitions. With carbon market potential valued at over USD 6 billion by 2030, stakeholders called for clear policies, financing, and investment to scale carbon credit initiatives across the region.

Mexico’s beef sector is gradually recovering from the severe impact of a screwworm outbreak that led the United States (US) to suspend live cattle imports, causing an estimated USD 700 million in losses. Only Sonora and Chihuahua are currently allowed to resume exports, following improved sanitary measures and progress in controlling the parasite. Since Nov-24, 32 infected cattle shipments have been intercepted and returned to prevent the disease from spreading northward. Mexican authorities have intensified inspections at federal checkpoints to contain the outbreak. The screwworm is a parasite affecting cattle and sheep that reduces productivity and causes skin injuries, resulting in significant economic damage. In response, US and Mexican officials have agreed to a phased reopening of key border points beginning July 7, with full reopening expected by mid-Sep-25. While domestic beef prices have seen a slight rise and overall food prices remain mostly stable, ongoing negotiations continue on other trade matters, such as avoiding tariffs on tomatoes. The beef export reopening marks a critical step toward restoring Mexico’s livestock trade stability.

Despite limited supply, domestic demand for beef in Spain remains at its lowest point of 2025, creating a sluggish local market. However, exports, particularly to Europe and North Africa, are helping stabilize prices, as foreign markets offer higher returns than domestic sales. At the Ebro and Binéfar markets, prices for male and female cattle remained steady, while cow prices rose due to tight supply in Europe. Although certain beef cuts, like forequarters, are facing weaker demand, overall supply is balanced, with few animals on farms and no urgency to sell, especially as feed is cheap and farmers are opting to increase weight. Domestic sales remain weak, but export markets continue to provide crucial support, with European demand showing strong momentum amid higher prices.

As the US reciprocal tariff suspension period ends on July 9, concerns are mounting in South Korea that agriculture may become a bargaining chip in South Korea-US tariff negotiations. Although the government has pledged to protect the sensitive nature of agriculture, distrust remains strong among farmers, particularly regarding the potential lifting of restrictions on US beef from cattle over 30 months old, a measure seen as vital for food safety. At a public hearing on June 30, industry groups such as the National Hanwoo Association urged the government to firmly block such imports, citing the risk of public backlash and damage to domestic beef markets. The US has previously raised issues with South Korea’s genetically modified organism (GMO) regulations, age limits on beef, and fruit import restrictions, pushing for greater market access. While calls for transparency in the negotiation process grow louder, government officials stress the need for strategic discretion. Still, they emphasize that South Korea is aware of US demands and will negotiate while fully considering agricultural sensitivities and the economic impact on domestic producers.

The United States Department of Agriculture (USDA) has lowered its US beef production forecast for 2025 to 26.36 billion pounds (lbs), citing reduced steer, heifer, and cow slaughter. This decline is expected to persist through the second half of 2025 (H2-2025), despite slightly heavier carcass weights. Conversely, the 2026 forecast has been raised by 135 million lbs to 25.275 billion lbs, driven by increased feedlot placements and higher animal weights. Strong global demand has led to an upward revision in 2025 beef export projections, though shipments to China remain restricted due to expired facility registrations. In contrast, exports to markets such as Hong Kong, South Korea, Japan, and Taiwan have grown. US beef imports are also rising to meet robust domestic demand for lean processing beef. Cattle price forecasts for both 2025 and 2026 have been revised upward, reflecting strong demand and recent price strength. In spring 2025, packers unexpectedly slowed slaughter rates, breaking seasonal trends, which tightened supply and pushed boxed beef prices higher. However, this increase has not fully offset packers’ losses, as slaughter steer prices have climbed even faster, reaching record highs by mid-Jun-25.

Uruguay’s beef sector showed strong performance in the first half of 2025 (H1-2025), driving the country's export growth. In Jun-25 alone, beef exports reached USD 226 million, a 34% increase from Jun-24, making beef the top export product, surpassing pulp. China regained its position as the leading market with a nearly 70% year-on-year (YoY) rise in purchases, totaling USD 76 million. Exports to the European Union (EU) also surged, nearly doubling from the previous year, supported by strong prices due to limited supply and a stronger euro. Shipments to Europe hit multi-year volume records, while the US remained a key buyer with a 66% increase in purchases over H1-2025. Overall, beef export growth was driven more by higher prices than volume, with prices peaking in May-25 before a slight dip in Jun-25, yet still strong by historical standards. Despite this momentum, exporters face challenges from a strong local currency and rising domestic costs, prompting calls for lower interest rates to ease the exchange rate pressure and support competitiveness.

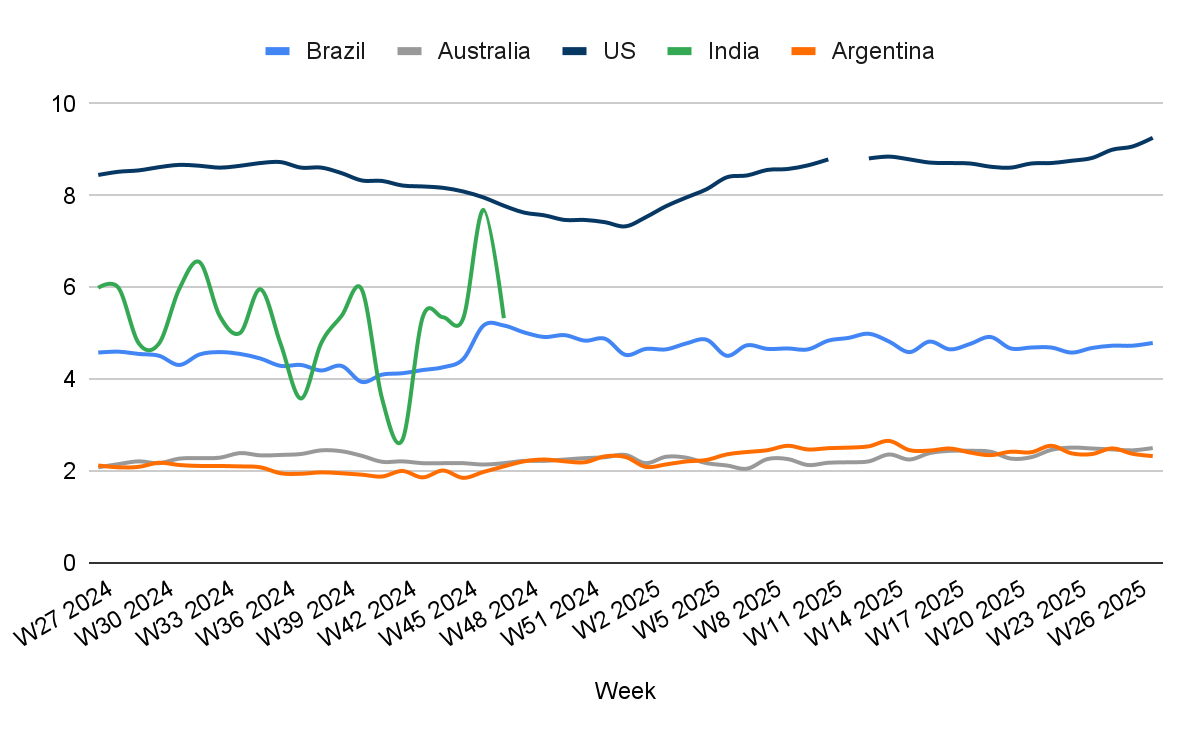

In W27, Brazil’s wholesale price for boneless rear beef rose by 1.27% week-on-week (WoW) to USD 4.79 per kilogram (kg), reflecting a 2.35% month-on-month (MoM) uptick and 4.59% YoY increase. The weekly price rise in US dollar terms was largely influenced by exchange rate fluctuations, as prices in Brazilian real remained steady at BRL 26.0/kg for the fourth consecutive week. According to the Center for Advanced Studies in Applied Economics (Cepea), although beef prices had shown small but consistent increases, the market has entered a phase of relative stability with slight declines. This is primarily due to the start of feedlot offerings, which have increased slaughter schedules and given buyers more room to negotiate lower prices. Liquidity in the spot market remains limited, as cattle ranchers are selling only small lots, while wholesale meat sales weakened toward the end of Jun-25, contributing to modest price drops. Safras and Mercado projects good availability of cattle finished in intensive systems in Jul-25, supported by term contracts and internal confinement operations. Despite these downward pressures, robust beef exports continue to play a key role in supporting prices, offsetting domestic softness.

Australia’s National Young Cattle Indicator (NYCI) averaged USD 2.50/kg in W27, marking a 2.04% WoW uptick, a 0.40% MoM rise, and a significant 20.19% YoY increase. According to Meat and Livestock Australia (MLA), the feeder steer indicator outperformed the restocker steer indicator, signaling a positive shift in market dynamics. Despite this, total yardings dropped by 21.79 thousand heads, falling to 50.48 thousand heads, indicating a tighter supply. Limited processor attendance was observed during the week, although demand remained strong for heavier steers weighing between 400 kg and 500 kg. Due to a shortage of high-quality cattle, prices rose across most states, with lot feeders outbidding processors, pushing feeder steer prices higher than restocker values. Queensland reported the largest price increase, underscoring strong regional demand amidst constrained supply.

In W27, US lean beef (92% to 94%) prices hit a record high, averaging USD 9.26/kg, reflecting a 2.09% WoW rise, a 4.99% MoM uptick, and a 9.59% YoY increase. This surge is largely attributed to strong seasonal demand driven by summer grilling and outdoor events. The consistent price increase also reflects structural supply issues, with the US cattle inventory at its lowest since 1952, attributed to prolonged droughts, pandemic-related disruptions, and meatpacking plant closures. While consumer demand has remained stable, supply constraints have significantly raised input costs, especially for small-scale ranchers managing limited herds amid rising feed prices and scarce resources. For businesses that focus on local sourcing and affordability, like food trucks and independent butchers, the sustained price increases are creating financial strain. Further adding to the pressure, the suspension of live cattle imports from Mexico, due to a screwworm outbreak, has tightened supplies. Fortunately, the gradual opening of the border has started, with cattle from Sonora and Chihuahua given the green light for exports. The 10% import tariff hike introduced in Apr-25 may have also constrained beef import volumes.

In W27, Argentina’s average steer beef price declined by 2.11% WoW to USD 2.32/kg, reflecting softer demand likely due to the end of a short-term boost from two national holidays in W25. Prices were also down 2.11% MoM, but remained 9.43% higher YoY, indicating a slow but possible recovery in demand following the economic downturn of 2024. Nonetheless, the beef sector continues to face significant volatility. In May-25, cattle slaughter dropped 5% YoY to 1.12 million heads, suggesting structural issues in the supply chain. Although slaughter weights reached a record 232.3 kg, feedlot profitability plummeted by 63% in just one month due to rising input costs, raising concerns about long-term sustainability. While there is no current shortage of animal protein, with per capita consumption still high at between 115 kg and 120 kg, consumers are increasingly shifting toward more affordable proteins like chicken and pork.

To realize the estimated USD 6 billion carbon credit opportunity by 2030, Latin American governments should prioritize developing a regional framework for livestock-based carbon markets. This should include establishing scientifically sound methodologies to quantify soil carbon sequestration in pastures, standardizing sustainability indicators across countries to build investor trust, and supporting small-scale ranchers through bundled carbon projects. Governments should also create enabling policies, streamline regulatory procedures, and offer financial incentives such as payment-for-results schemes, as pioneered by Costa Rica. Public-private collaboration and knowledge sharing across borders will be key to scaling carbon monetization initiatives.

Mexico should continue strengthening its animal health infrastructure, focusing on surveillance, rapid response, and transparent communication protocols with key trade partners like the US. To avoid future trade disruptions, a regional screwworm eradication program led by the Service for the National Service of Agrifood Health, Safety and Quality (Senasica), supported by bilateral funding, could be institutionalized. The government should negotiate expanded export certifications for other beef-producing states that meet sanitary benchmarks. Additionally, leveraging this recovery phase to promote value-added beef, such as premium cuts in the US market, can help recapture lost export value and investor confidence.

The South Korean government should institutionalize a multi-stakeholder negotiation framework that includes farmer associations, food safety experts, and trade economists to inform tariff-related decisions. It should seek to maintain the 30-month age limit on US beef imports by emphasizing food safety concerns backed by scientific evidence. Simultaneously, South Korea can propose balanced concessions in less sensitive sectors while leveraging its trade deficit in US agricultural products to push for reciprocity. Greater transparency and proactive communication with domestic stakeholders will help rebuild trust and avoid public backlash during trade talks.

Sources: Tridge, Agrinet, Agromeat, Aflnews

Read more relevant content

Recommended suppliers for you

What to read next