Original content

The Rio Grande do Sul Rice Institute (IRGA) reported that the planting of the 2024/25 rice crop in Rio Grande do Sul concluded early in Jan-25, covering 927.8 thousand hectares (ha), slightly below the projected 948 thousand ha. The shortfall was due to flooding and heavy rainfall in central areas, which hindered sowing and forced planting in areas not recommended by the Agricultural Zoning of Climatic Risk (ZARC). The planting season for irrigated rice typically spans September 1 to December 20. Rice growers face challenges such as drought, which has reduced river levels essential for irrigation, and delayed field management caused by excessive rain.

India entered a four-year agreement to export 1 million metric tons (mmt) of non-basmati white rice annually to Indonesia following a strong harvest that boosted domestic inventories. Facilitated by India’s Ministry of Cooperation and Indonesia’s Ministry of Trade, this partnership will be executed through National Cooperative Exports Limited, sourcing rice through open bids from cooperative societies.

Indonesia's rice output is projected to drop by 2.43% year-on-year (YoY) to 30.34 mmt in 2024 due to prolonged dry weather, increasing its reliance on imports to sustain its 280 million population. India had previously restricted rice exports in response to an El Niño-induced poor monsoon and rising domestic prices but lifted the floor price and export bans in late 2024 to capitalize on higher production. This deal reflects India’s strategy to leverage its position as the world's largest rice exporter while addressing Indonesia's import needs.

Pakistan’s rice production for the 2024/25 season has been revised down to 9.5 mmt, a 3.65% YoY decline in area and yield, while exports are projected to fall by 11.48% YoY to 5.8 mmt, according to the United States Department of Agriculture (USDA) data. Despite favorable irrigation and planting conditions ensuring a promising harvest, Pakistan faces stiff competition following India’s re-entry into the global rice market, which lifted its export ban and minimum export price (MEP) by late 2024. India’s competitive pricing in the basmati and non-basmati markets will shift demand dynamics significantly.

In 2023/24, Pakistan’s rice exports nearly doubled due to an abundant harvest, competitive pricing, and strong demand from Malaysia and Indonesia, aided by India’s temporary export ban. However, with India resuming exports, Pakistan's exporters face challenges maintaining their market share amid intensified competition.

In 2024, Russia achieved a record rice harvest of over 1.2 mmt, maintaining wholesale prices at 2022 levels. Plans are underway to expand rice cultivation from 207 thousand ha to 275 thousand ha by 2029, focusing on the Astrakhan Region and Primorsky Krai. Russia aims to meet domestic demand and enhance export potential by boosting yields by 1 metric ton (mt) per ha to achieve 2 mmt of rice production by 2030. Initially, rice prices were expected to decline due to the abundant supply, export restrictions, and stabilized imported rice prices before eventually stabilizing, supported by the cost advantage of Russian rice over imports, mainly from India.

Vietnam's agricultural exports have surged, driven by strong performances in vegetables, fruits, and rice, with durian playing a key role in boosting economic gains. Rice remains the cornerstone of Vietnam's export portfolio, achieving a 21% YoY increase in value to nearly USD 5.8 billion. The agricultural department projects a record-high average rice price of USD 620/mt in 2024, with further growth anticipated in 2025.

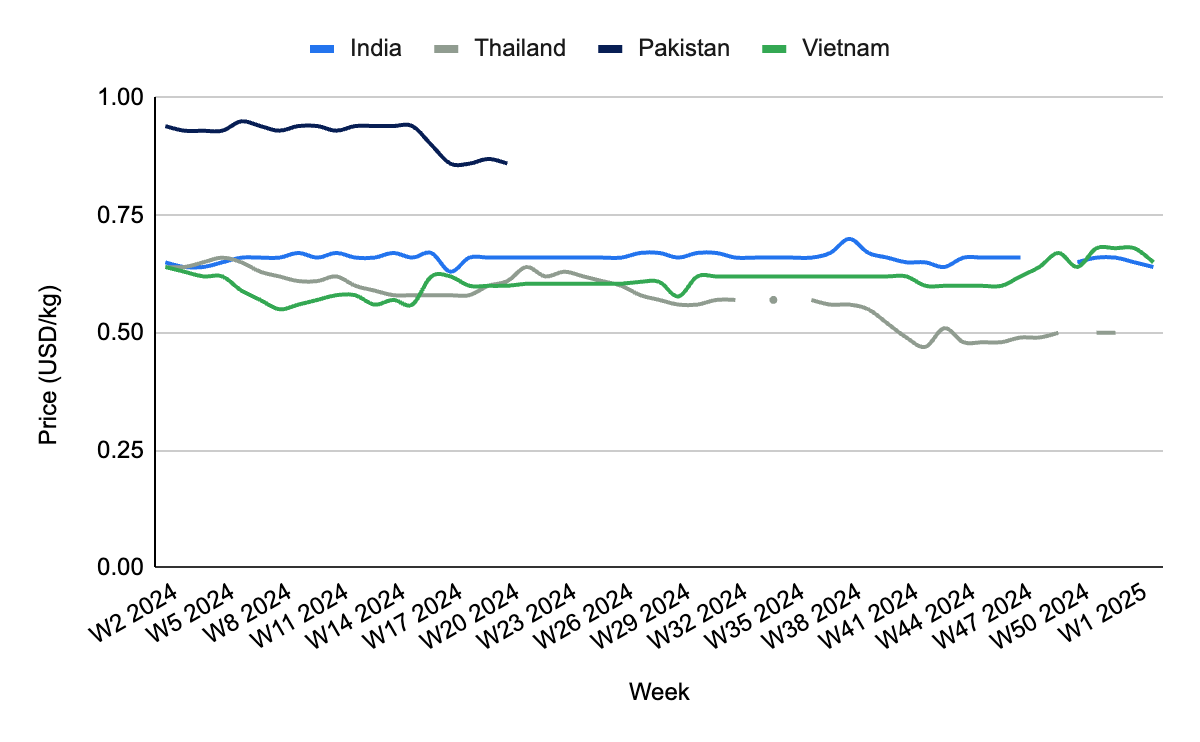

In W2, India's wholesale rice prices fell by 1.54% week-on-week (WoW), reaching USD 0.64 per kilogram (kg), down from USD 0.65/kg in W1. This marks the third consecutive week of declines, bringing rice prices to a 17-month low, driven by weak demand and the depreciation of the Indian rupee (INR) to a record low. Demand was weak from Asian and African buyers due to the New Year holidays. The price drop is mainly due to India’s record-breaking 2024 rice production, which reached 120 mmt during the summer, accounting for approximately 85% of total rice output. This bumper harvest increased rice inventories, with state granaries holding 44.1 mmt of rice reserves at the beginning of Dec-24, exceeding the government’s target by more than five times. The surplus supply has exerted significant downward pressure on domestic rice prices.

In W2, Vietnamese rice prices decreased 4.41% WoW and month-on-month (MoM) but increased 1.56% YoY, reaching USD 0.65/kg. The decline was due to overflowing rice stocks held by Vietnamese traders, which exerted downward pressure on prices. Vietnam’s rice purchases have also decreased compared to the previous year, reflecting fluctuations based on prevailing market conditions. To address pricing challenges, the Agriculture Ministry and the Rice Federation have consistently encouraged farmers to cultivate specific strategic rice varieties to help them secure assistance and purchase agreements with mills at more favorable prices.

In W2, United States (US) rice prices declined by 2.5% YoY to USD 0.78/kg. This decrease is primarily due to increased domestic production and higher carryover stocks from the previous marketing year. According to the USDA, the total rice planted area in 2024 increased to 2.943 million acres from 2.894 million acres in 2023. This acreage expansion and favorable weather conditions led to higher yields and an overall increase in rice production. Moreover, global market dynamics have influenced US rice prices. The anticipated end of India's export ban and large harvests in other major rice-producing countries are expected to exert downward pressure on global rice prices.

Rice-exporting countries like Pakistan should focus on diversifying their export markets to reduce dependence on traditional buyers and mitigate competition from India. By targeting emerging markets in regions such as Africa and the Middle East, exporters can tap into new opportunities. This can be achieved by strengthening trade relationships through bilateral agreements and participating in international trade fairs to promote premium rice varieties. Diversification will provide a competitive edge, offset the impact of India’s re-entry into global markets, and help maintain market share.

To address production challenges caused by climate change, Indonesia and Brazil should invest in cultivating drought- and flood-resistant rice varieties. Examples of suitable varieties include IR64, Swarna Sub1, and Sahbhagi Dhan, known for their resilience to submergence and drought conditions. Moreover, developing and adopting newer varieties, such as NERICA (New Rice for Africa), can improve productivity in regions prone to erratic weather patterns. Governments and stakeholders should partner with research institutions to accelerate the breeding and distribution of these resilient varieties. Introducing subsidies and training programs can encourage farmers to adopt them, helping to reduce production losses, stabilize yields, and ensure food security despite adverse weather conditions.

Vietnam and India should expand contract farming arrangements to support farmers and ensure fair product pricing. Collaborating with rice mills and exporters to establish minimum price guarantees will protect farmers from price volatility. Furthermore, offering technical assistance and resources for high-quality production will strengthen the overall supply chain. These measures will improve farmer income stability, enhance rice quality for export, and foster long-term sustainability in the rice sector.

Sources: Tridge, AgroInvestor, Foodmate, NoticiasAgricolas, Retail.economictimes, UkrAgroConsult

Read more relevant content

Recommended suppliers for you

What to read next