Original content

The global avocado market, with a significant contribution from Peru, is expected to grow continuously despite potential challenges. Global avocado exports are projected to reach 3.2 million tons by 2028/29, driven by expanding production in 23 exporting countries. These countries include Peru and Colombia, which complement Mexico's dominant position during its off-season. Consumption is rising in traditional markets like the United States (US), the European Union (EU), and the United Kingdom (UK), as well as in emerging regions such as China, Saudi Arabia, and Southeast Asia.

While trade faces challenges, including proposed US tariffs on Mexican products and climate-related risks, investments in promotion, consumer education, and market diversification are expected to support the avocado industry’s growth.

Morocco's avocado exports continue to increase significantly, reaching 42 thousand tons between Oct-24 and Dec-24. The forecast for the 2024/25 harvest will yield approximately 90 thousand tons, with exports expected to account for 80 thousand to 90 thousand tons, while the local market will consume about 10% of the total production. Despite a slight decline in avocado prices in European markets, Moroccan exporters are focused on accelerating exports, with a key milestone in April to ensure their competitiveness against major exporting nations such as Spain, Colombia, and Israel. The avocado farming industry has expanded significantly in Morocco, particularly in regions like Tiflet, Moulay Bousselham, and Larache, and is expected to continue succeeding in international markets.

New Zealand's avocado industry is optimistic about the current season after facing two challenging years marked by cyclones and economic difficulties. Favorable weather conditions have led to strong flowering and fruit sets across key growing regions, with an anticipated harvest of seven million trays, up from five million in the previous year. The Bay of Plenty leads production, contributing 50%, followed by Northland at 45%, while other regions like Auckland, Gisborne, and Taranaki contribute smaller volumes. Around 50 to 60% of New Zealand’s avocados are exported, primarily to Australia, with key Asian markets such as South Korea, Japan, and Thailand driving further growth. Investments in orchard management, export strategies, and sustainability efforts are reinforcing New Zealand’s reputation for premium avocados, ensuring resilience and long-term potential for the industry.

The Peruvian avocado export campaign for 2025 has experienced delays due to adverse weather conditions, including heavy rains and unusual waves, which disrupted harvest schedules and shipments from ports. Initial avocado shipments have been sent to China, but prices decreased approximately 20% year-on-year (YoY), as Chinese demand shifts toward premium gifts like cherries. Despite these challenges, growth projections remain positive, with a 5 to 10% increase expected in production from the Peruvian highlands and an overall growth projection of 20%.

While Europe faces an oversupply from multiple origins, exporters like Marand Company remain optimistic about market recovery. They are also hopeful about the logistical advantages of the Chancay Port, which is expected to improve transit efficiency to Asia starting in April or May.

In Njombe Town Council, Tanzania, avocado farmers face challenges due to intermittent electricity supply, which disrupts irrigation during dry periods and limits overall productivity. Despite significant investments in avocado cultivation, particularly in Kifanya, reliable power is urgently needed to ensure consistent water access for farms. Njombe, a primary hub for high-quality avocado seedlings, produces 1.5 million seedlings annually, attracting demand from neighboring countries such as Burundi and Congo. However, local growers stress the importance of prioritizing domestic seedlings to strengthen Tanzania's agricultural industry and maintain competitiveness in the global market. Addressing the electricity issue is crucial for sustaining and advancing avocado farming in the region.

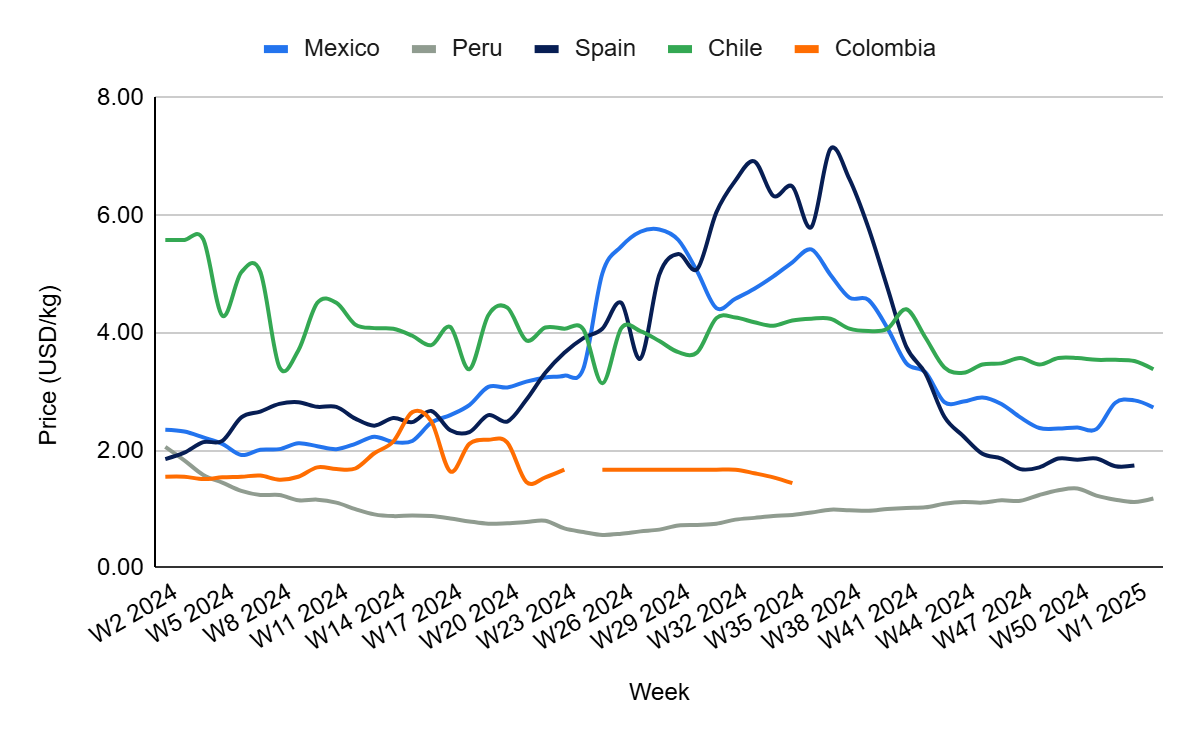

Mexico's avocado prices fell by 4.21% week-on-week (WoW) to USD 2.73 per kilogram (kg) in W2 due to some market adjustments following the previous weeks' price hikes. While the overall supply remains tight, slight shifts in demand have contributed to the dip. However, month-on-month (MoM) and YoY prices surged significantly by 15.68% MoM and 16.17% YoY due to ongoing supply challenges, with all sizes being extremely tight, which has led to quality-driven price elevation. Additionally, elevated prices and tight supplies are expected to persist for the next two weeks, further supporting the price increase. The reported checkerboarding, a ripening issue where avocados ripen unevenly, also indicates challenges in achieving consistent ripening, adding to the pressure on prices.

In W2, Peru's avocado prices increased by 5.36% WoW to USD 1.18/kg. However, prices dropped by 4.07% MoM and 42.72% YoY due to ongoing challenges in the export campaign caused by adverse weather conditions, including heavy rains and unusual waves, which disrupted harvest schedules and shipments. The MoM decline reflects the seasonal normalization of supply as production stabilizes, while the significant YoY drop is driven by weakened demand in key markets like China, where consumer preferences have shifted toward premium gift items such as cherries. Additionally, an oversupply in Europe from competing origins has exerted further downward pressure on prices.

In Spain, avocado prices increased by 1.15% WoW to USD 1.76/kg in W2 due to a slight recovery in production following favorable rainfall in spring and autumn, which boosted water reserves and improved yield prospects, especially in regions like Axarquía and Costa Tropical. The modest growth in supply from new production areas in western Andalusia, alongside the ongoing development of the organic segment, also contributed to the price increase. However, YoY prices dropped by 5.38% MoM and 4.86% YoY due to increased competition from high-yielding regions, particularly North Africa (mainly Morocco), and the larger supply of avocados in Spain, which has put downward pressure on prices in comparison to the previous year.

Avocado prices in Chile dropped by 3.98% WoW to USD 3.38/kg in W2, reflecting a 4.52% MoM and 39.43% YoY decrease due to the high supply from the ongoing harvest season, which continues to apply downward pressure on prices. The MoM decline is due to sustained post-holiday demand softening, while the significant YoY drop reflects the normalization of market conditions following the exceptionally high prices in the previous year, which were caused by earlier supply disruptions. Stable domestic and export demand has not been sufficient to counterbalance the impact of elevated supply levels.

Peruvian avocado exporters should diversify marketing efforts by targeting high-demand regions, such as premium markets in Europe and Asia while emphasizing quality and freshness. Collaborating with logistics partners to minimize disruptions from abnormal weather will further support consistent supply and competitive pricing.

Mexican avocado exporters and distributors should collaborate with supply chain partners to address ripening inconsistencies by adopting advanced ripening technologies and monitoring systems. Additionally, demand management strategies, such as targeted promotions and emphasizing premium quality, can stabilize market fluctuations and optimize revenue during periods of tight supply.

Moroccan avocado exporters should focus on strategically aligning export timing to peak demand periods in European markets, ensuring competitiveness against Spain, Colombia, and Israel. Additionally, they should explore diversifying into new high-potential markets outside Europe to mitigate price pressures and maximize revenue from the growing production.

Sources: Tridge, Agraria, Eastfruit, Freshfruitportal, Freshplaza, IPP Media, Msn, Sunlive

Read more relevant content

Recommended suppliers for you

What to read next