Original content

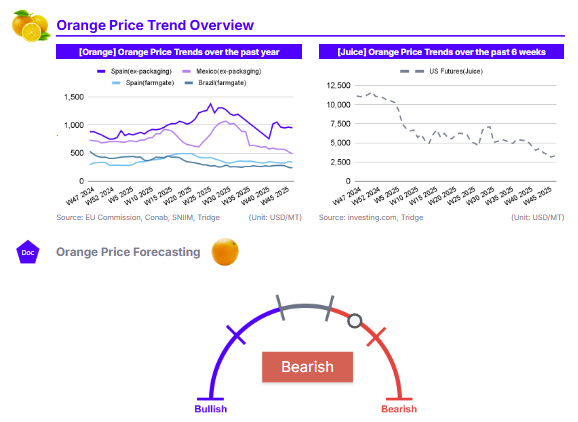

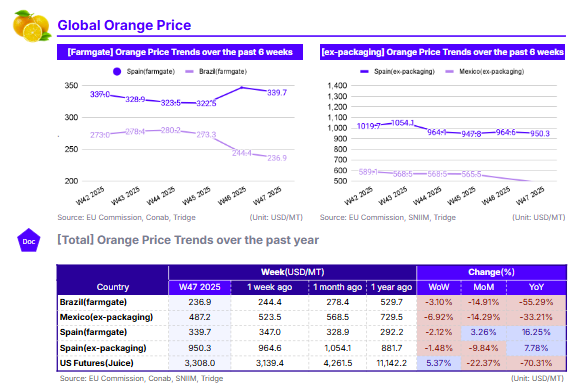

In Brazil, the farmgate price for oranges was USD 236.9/metric ton (mt) in W47, a decline of 3.10% week-on-week (WoW). Mexico’s ex-packaging price saw a sharp drop of 6.92% WoW to USD 487.2/mt. Spain’s farmgate price fell 2.12% WoW to USD 339.7/mt, and the ex-packaging price decreased by 1.48% WoW to USD 950.3/mt. Conversely, US Orange Juice Futures staged a significant rebound, rising 5.37% WoW to USD 3,308/mt.

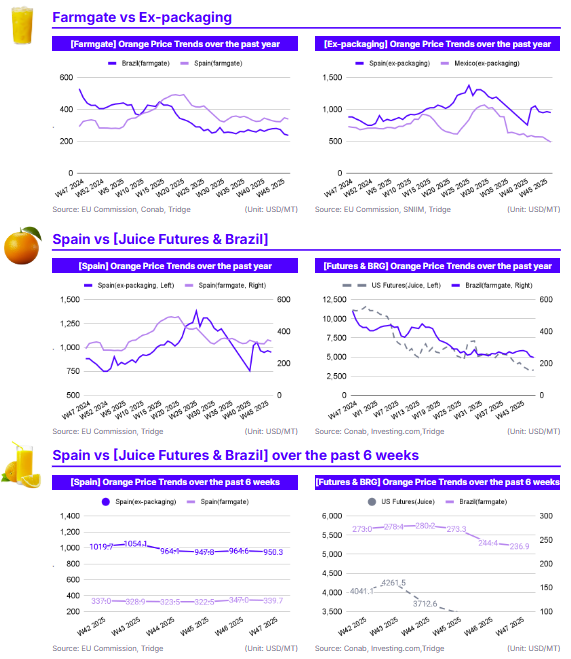

The most striking contrast this week is the sharp decline in physical commodity prices against the strong rebound in US Futures. The steep price drops in Brazil (-3.10% WoW) and Mexico (-6.92% WoW) are driven by persistent oversupply dynamics meeting weak external demand. Brazil's drop is explicitly linked to subdued demand from the European Union (EU), which is squeezing prices in São Paulo despite an overall positive outlook for the 2025/26 season. Mexico's sharp decline is attributable to increased competition from rising US domestic production and rain-related quality concerns for its citrus crop. In Europe, Spain's farmgate price fell 2.12% WoW as production keeps ramping up as the 2025 season progresses. Spain also continues to face heavy competition from foreign oranges, particularly from South Africa. The 5.37% WoW surge in US Futures is likely a price correction following a steep drop in recent weeks.

US Orange Juice Futures prices fell 22.37% month-on-month (MoM), resulting in a massive 70.31% year-on-year (YoY) collapse. Brazil’s farmgate price saw a significant 14.91% MoM drop and remains down 55.29% YoY. Mexico followed suit, dropping 14.29% MoM and 33.21% YoY. Spain remains the clear outlier. Its farmgate price increased 3.26% MoM and 16.25% YoY, while the ex-packaging price was still up 7.78% YoY despite a MoM decline of 9.84%.

The severe YoY price collapse in the Americas is the primary long-term trend, driven fundamentally by supply normalization. Brazil is expected to produce 306.7 million 40.8-kg boxes in 2025, a massive increase from the previous year's 37-year low. This recovery, combined with a 6% projected increase in the US California Navel orange crop, provides ample supply, driving prices down from 2024's crisis peaks. Furthermore, the removal of US tariffs on oranges from Brazil and South Africa increases competition, applying downward pressure on futures and physical prices in the region. In contrast, Spain’s robust 16.25% YoY price increase reflects its persistent structural supply shortage. Spain's citrus production is expected to hit a 16-year low in 2025, a situation that structurally caps near-term price decreases and supports the bullish long-term outlook for Spanish oranges.

Global buyers, particularly juice processors, should prioritize sourcing from Brazil to capitalize on its structural price advantage and stable availability. In W47, the Brazilian farmgate price of USD 236.9/mt is highly competitive, trading at a substantial discount compared to Mexico (USD 487.2/mt) and Spain (USD 339.7/mt). This price has fallen 14.91% MoM and is now down 55.29% YoY, offering significant value for money compared to alternative major producing origins.

This low pricing is driven by Brazil’s normalized harvest volumes (expected 306.7 million 40.8-kg boxes in 2025) coinciding with subdued demand from the EU, which is putting downward pressure on São Paulo prices. For US buyers, sourcing from Brazil hedges against Mexican quality concerns and benefits from the recent removal of tariffs on oranges imported from Brazil, potentially leading to a further price advantage. However, buyers should act quickly as historically, prices for Brazilian oranges have a tendency to trend upwards towards the end of the year as the harvest in Brazil nears its end. According to Tridge Eye data, suppliers worth considering in Brazil include NCD Brazil, GBG, and Soeli Desouza Ferris.

Read more relevant content

Recommended suppliers for you

What to read next