Original content

The vice-president of the Corrientes Rice Producers Association (ACPA) announced a significant increase in rice sown area this year, expecting to reach 222.7 thousand hectares (ha), marking one of the largest planted areas in the association's history. The predicted harvest is anticipated to exceed 1.5 million metric tons (mmt), with a productivity rate of 6.8 metric tons (mt) per ha. This success is due to favorable local and international market conditions, deregulation measures, eased input imports, and reduced agrochemical usage.

Severe floods in Malaysia have devastated over 38 thousand ha of paddy fields in the northern states, severely impacting the central rice-producing regions. Kedah and Kelantan are the worst affected, with 12,600 ha and over 26 thousand ha of paddy fields submerged, respectively. The timing of the floods has been particularly critical, as many paddy fields were either newly planted or ready for harvest, causing significant financial losses for farmers. In Kelantan alone, agricultural losses were estimated to surpass USD 3.61 million. Despite the scale of the disaster, the government has yet to announce any support measures for the affected farmers.

According to the Minister of Agriculture and Food Security, Malaysia's rice supply shortage, caused by floods, will be mitigated by reducing the price of imported white rice from December 8. The floods have disrupted paddy farming, alongside vegetable, livestock, and fish farming, leading to a drop in local rice production, which accounts for 56% of the market. To address this, the government will leverage lower international rice prices, which have dropped to USD 632.34/mt from previous highs of USD 722.67 to USD 745.26/mt. While acknowledging a 4% decrease in rice supply due to earlier droughts in Kelantan, the Minister reassured that the price reduction for imports would not harm farmers and would align with the government’s goal of achieving 61% local rice productivity.

Farmers in Kalmykia, Russia, harvested 16.7 thousand mt of paddy rice this year, marking a 59% year-on-year (YoY) increase. This significant improvement is due to a 38% YoY expansion in the rice cultivation area to 3.6 thousand ha. State support played a crucial role by providing subsidies to offset water costs for rice farming, enabling timely agricultural practice, and using zoned rice varieties. The average rice yield increased to 5.01 mt/ha this year, up from 4.32 mt/ha in 2023. Reduced water tariffs, saving farmers USD 390,223, further supported this growth. Known for producing the world’s northernmost rice, Kalmykia continues to uphold its reputation as a key rice-growing region. Its rice industry dates back to the 1970s.

Thailand’s Ministry of Commerce has set a 2025 rice export target of 7.5 mmt, a reduction from this year’s estimated 10 mmt. From Jan-24 to Nov-24, rice exports rose 14% YoY to 9.27 mmt, with the annual volume expected to reach 10 mmt, valued at over USD 6 billion. This growth is due to strong import demand for year-end consumption, including Christmas, New Year, and Chinese New Year celebrations. Despite the reduced export target for 2025, Thailand maintains sufficient rice production and robust export capabilities to meet global market needs and ensure reliable deliveries.

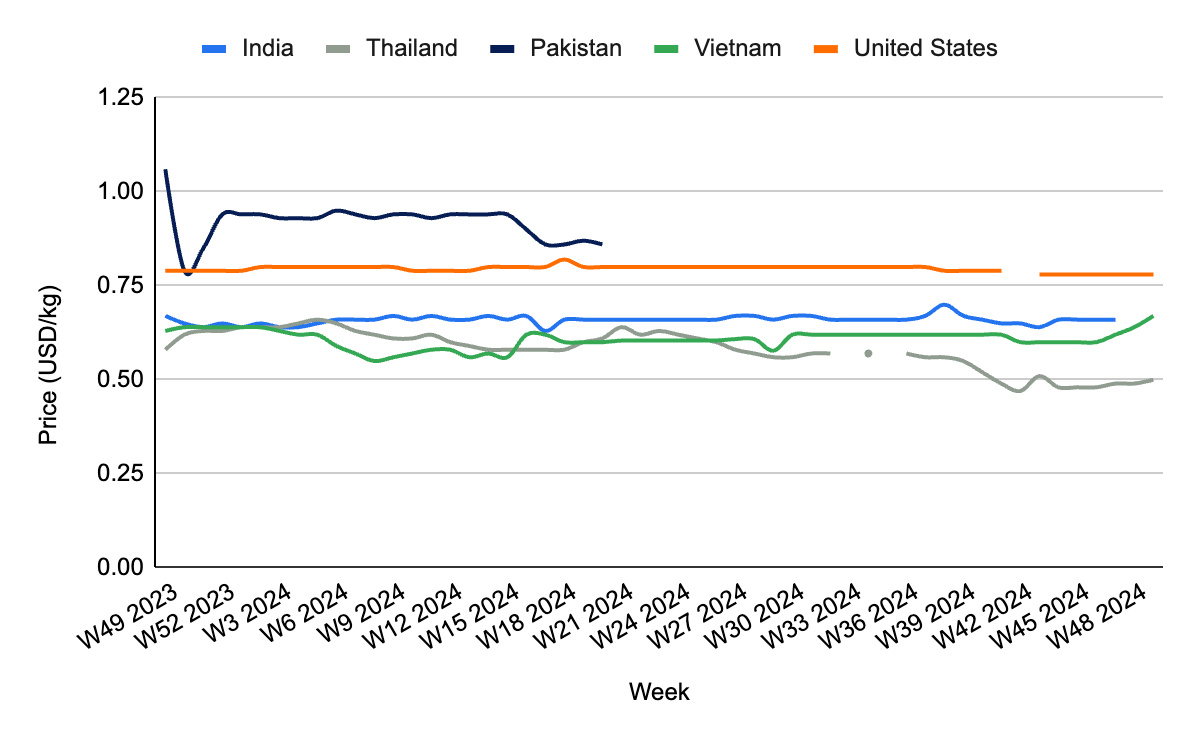

In W49, India's wholesale rice prices increased 1.52% week-on-week (WoW) to USD 0.67 per kilogram (kg). This price increase was driven by rising global demand after India lifted export restrictions on non-basmati rice. The policy changes included removing export duties on non-basmati white rice and reducing the levy on parboiled rice to 10%, following the removal of the minimum export price for basmati rice. These shifts, combined with ample government rice stocks, significantly impacted the global rice market. Nepal's rice imports from India reached USD 260.67 million in the 2023/24 season, contributing to a total of USD 1.74 billion over the past three years.

In W49, wholesale prices for Thai rice rose 2.04% week-on-week (WoW) and 4.17% month-on-month (MoM) to USD 0.50 per kilogram (kg), driven by global supply constraints and strong import demand from countries like the Philippines, Indonesia, and other Asian markets. Higher production costs, including elevated fertilizers, fuel, and labor prices, have contributed to these price pressures. However, seasonal supply increases and currency fluctuations, notably the Thai baht (THB) depreciation, helped mitigate some upward pressure. On a YoY basis, prices declined by 13.79%, mainly due to the arrival of the 2024/25 marketing year (MY) paddy rice crop, which boosted supply and placed downward pressure on prices.

Vietnamese rice prices rose 4.69% WoW and 11.67% MoM to USD 0.67/kg in W49, marking a recovery after lagging behind Thailand, Pakistan, and Myanmar prices. This price surge is due to unexpected demand increases from major import partners, notably the Philippines and Indonesia. These demand shifts and vigorous seasonal import activity have driven Vietnamese rice prices to their highest global levels, reflecting the critical role of heightened import demand in key markets.

In W49, the wholesale price of milled white long rice in Arkansas, US, stood at USD 0.78/kg, reflecting a 1.27% YoY decrease. This decline is primarily due to increased rice production in the US, which reached approximately 7.6 mmt for 2024/25 MY. This higher supply has led to downward pressure on prices. Furthermore, reduced global demand, particularly from major importers such as Mexico, the Philippines, and Indonesia for US rice, has further weakened price stability.The US dollar (USD) strengthening has also made US rice less competitive than other exporting nations.

Thailand will reduce its 2025 rice export target due to concerns about production constraints, labor costs, and market price pressures. To maintain its status as a key global rice exporter, Thailand should strengthen trade partnerships with its major importers, such as the Philippines and Indonesia, by negotiating long-term agreements and flexible trade terms. Moreover, addressing supply chain inefficiencies by improving logistics, infrastructure, and production processes could help mitigate costs associated with rising labor and input prices. Another strategic focus should be on premium rice markets by investing in certifications, sustainable farming practices, and branding efforts to align with the growing consumer demand for specialty and organic rice products. These strategies will ensure Thailand remains a reliable supplier in global rice markets while adapting to economic and logistical challenges.

Climate change has intensified weather unpredictability, as evidenced by the recent severe floods impacting rice-growing regions in Southeast Asia. Governments and agricultural organizations should implement climate-resilient rice farming techniques to safeguard future rice production. This includes promoting the adoption of flood-tolerant rice varieties such as Sub1, IR64, and BRRI Dhan 49, which are specifically developed to recover quickly from inundation and reduce crop loss. Furthermore, investing in early warning systems and flood prevention infrastructure, such as dams and controlled water storage, can minimize damage caused by extreme weather events. Rice farmers should also receive technical support to adopt modern farming methods such as proper drainage, crop diversification, and water-saving technologies. These proactive measures can reduce risks associated with climate variability while enhancing the sustainability and resilience of rice farming in vulnerable regions.

Thailand, Vietnam, and India are well-positioned to implement supply chain efficiency strategies through private-sector collaboration. As one of the world’s largest rice exporters, Thailand could benefit from private investments in modern storage facilities and improved logistics networks to minimize post-harvest losses and ensure timely distribution to key markets. With its growing rice export economy, Vietnam could strengthen transportation and implement advanced market forecasting tools to better respond to seasonal demand shifts and logistical bottlenecks. Similarly, with its vast rice-producing regions, India faces challenges such as post-harvest losses and distribution inefficiencies; thus, shared transport services and technological innovations could streamline supply chains, reduce costs, and improve market access. Strengthened partnerships between cooperatives, input suppliers, and private companies would enhance resilience and create a more efficient rice supply chain in these nations.

Sources: Tridge, Bangkokpost, Kvedomosti, Planetaarroz,Portal Do Agronegocio, Theedgemarkets

Read more relevant content

Recommended suppliers for you

What to read next