Original content

Brazil's wheat imports grew significantly in 2024, reaching the highest volume in four years for the 12 months ending in Nov-24. In Nov-24 alone, Brazil imported 427,530 metric tons (mt) of wheat, 33% higher year-on-year (YoY). This increase is primarily due to Argentina's excellent supply of competitively priced wheat. Of the total imports, 79.5% came from Argentina, marking the most significant volume in the past six months. Over the 12 months ending in Nov-24, Brazil's total wheat imports reached 6.52 million metric tons (mmt), the highest since the period ending in Nov-20, when 6.53 mmt were imported, according to Secretariat of Foreign Trade (SECEX) data and Center for Advanced Studies in Applied Economics (CEPEA) analysis.

The Bulgarian Ministry of Agriculture has reported a notable improvement in wheat quality, with 73.04% of the 2024 crop classified as milling quality, up from 48.7% last year. This increase is due to favorable weather conditions in the weeks before harvest. This enhancement in quality is expected to strengthen Bulgaria's grain export potential, particularly in Egypt, Algeria, and Morocco, heightening competition in the Middle East and North Africa (MENA) region.

According to data from the Pakistan Bureau of Statistics (PBS), Pakistan's wheat imports declined 100% YoY during the first four months of the 2024/25 Financial Year (FY) compared to the same period last year. In the corresponding period of 2023/24, the country imported over 556,903 mt of wheat, spending USD 166.633 million, whereas it recorded no wheat imports during the same period this year.

The United Kingdom (UK) Agriculture and Horticulture Development Board (AHDB) reports that the 2024/25 wheat harvest is expected to tighten the country's grain balance despite high stocks and a projected rise in imports. The wheat harvest is estimated at 16.64 mmt, marking a 21% YoY decline and the second-lowest figure, following the 2013/14 harvest of 11.05 mmt. This decline is due to reduced sowing area, lower yields, and unfavorable weather conditions throughout the growing season. Meanwhile, imports are forecasted to increase by 163 thousand mt, reaching 2.60 mmt in the 2024/25 season.

Russia projects a similar wheat crop harvest in 2025 as in 2024, with output estimated at 81.5 mmt, slightly exceeding this year's 81.3 mmt. This follows weather-related challenges, including severe drought, which caused a sharp decline in 2024 production and disrupted sowing for 2025, leaving young crops in their poorest recorded condition. Citing data from the state weather forecasting agency, analysts noted that the dry conditions are among the worst historically. Meanwhile, Ukraine's wheat output could increase in 2025 due to expanded planting.

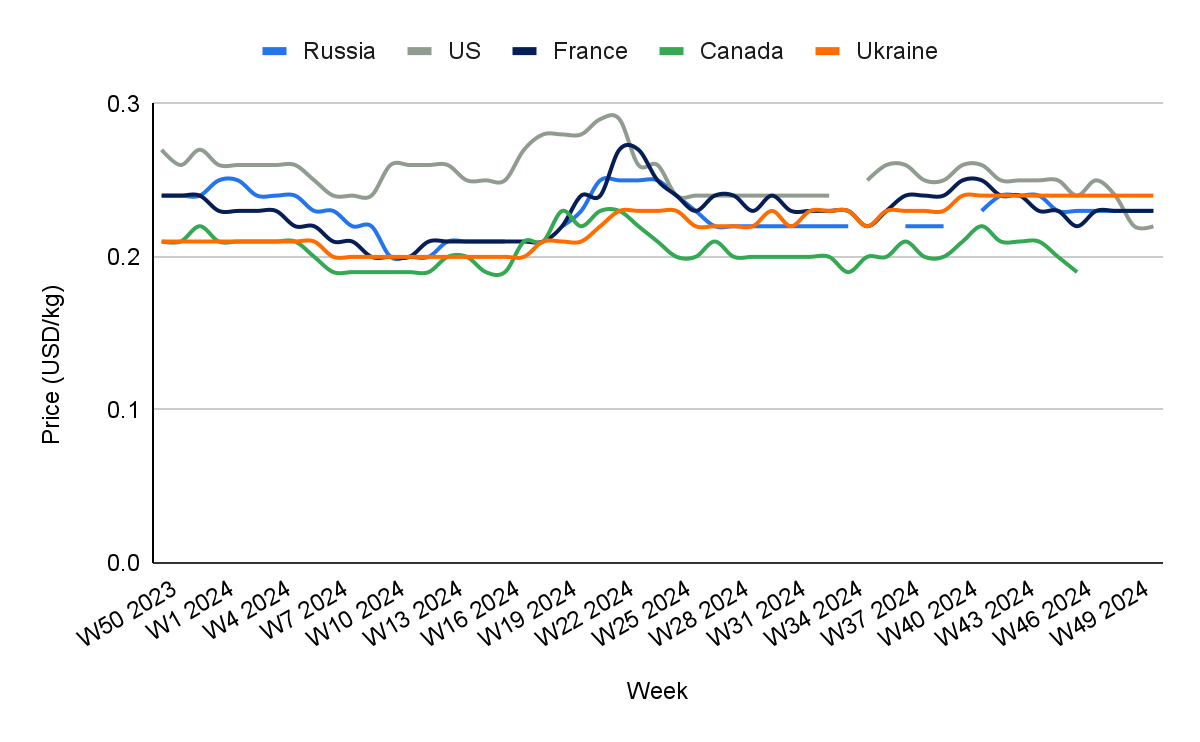

In W50, Russian wheat prices remained stable week-on-week (WoW) and month-on-month (MoM) but declined by 4.17% YoY to USD 0.23 per kilogram (kg). Russia's 2025 wheat harvest forecast was revised upward by 1.5 mmt to 81.6 MMT, driven by a higher winter wheat forecast of 54.3 mmt. This revision is due to an increased harvested area of 15.43 million hectares (ha) and a higher yield forecast of 3.52 mt/ha, supported by favorable growing conditions in Southern Russia. Moreover, prices are also falling in the market due to low international demand and the introduction of new export regulations aimed at controlling domestic prices.

In W50, wheat prices in the United States (US) remained stable WoW at USD 0.22/kg but declined by 12% MoM from USD 0.25/kg in W47. This decline is mainly due to improved crop conditions, with rain and snow in Nov-24 providing the crop with a buffer for the post-dormancy development phases in spring 2025. According to the United States Department of Agriculture's (USDA) winter wheat condition index, there was a record 35-point improvement from late Oct-24 to late Nov-24. Moreover, as of November 24, the USDA reported that farmers had completed 97% of the expected winter wheat planting for the 2025 harvest, matching last year’s rate, though slightly below the five-year average. Significant increases in planting in California and North Carolina were observed, and 16 of the 18 major wheat-producing regions are either finished or near completion of their planting activities.

In W50, French wheat prices remained stable WoW but decreased by 4.17% YoY to USD 0.23/kg. The decline is due to a stronger euro , increased competition from the Black Sea region, and recent tenders from Tunisia and Algeria favoring cheaper Russian wheat. The ruble's depreciation has further enhanced Russia’s competitiveness, while adverse harvest conditions in France, including heavy rainfall affecting crop quality, contributed to the price drop. Also, strained diplomatic relations with Algeria, exacerbated by France’s recognition of Morocco's sovereignty over Western Sahara, have reduced wheat purchases from France.

In W50, Ukrainian wheat prices remained stable WoW and MoM at USD 0.24/kg but rose 14.29% YoY. This increase is due to concerns over drought conditions affecting winter wheat planting for the 2025 harvest. The ongoing war and adverse weather patterns have reduced the area sown for winter wheat in Ukraine, with an estimated 4.2 million ha for 2024, down from 4.4 million ha in the previous year. With a smaller expected harvest and reduced carryover stocks, Ukraine’s exportable surplus will likely be constrained, putting upward pressure on prices as global demand remains strong.

Bulgaria's improvement in wheat quality presents an excellent opportunity to strengthen its export position in the MENA region. Countries like Egypt, Algeria, and Morocco, major wheat importers, are highly competitive markets, particularly for high-quality wheat. Bulgaria should focus on marketing this improved wheat as a high-quality product, positioning it as a reliable and competitive choice in these regions. Moreover, Bulgaria could enhance its product offering by introducing specialty wheat varieties, such as soft red winter wheat, known for its high milling quality, making it appealing to the MENA markets that value consistency in flour quality for bread and pasta production. Working on certifications and increasing transparency about the wheat's origins can further bolster Bulgaria's presence in these markets.

Brazil witnessed significant growth in wheat imports, primarily from Argentina, which accounted for 79.5% of its total wheat imports in the past year. Given the risks of over-reliance on a single supplier, Brazil should diversify its wheat import sources to ensure a stable supply. Expanding imports from countries like Russia, Ukraine, and the US would not only spread the risk but also provide Brazil with competitive prices and a broader range of wheat varieties. Russian wheat, tough red winter wheat, is an excellent alternative due to its quality and competitive pricing. Similarly, Brazil can look into the high-protein hard red spring wheat from the US for specific industrial uses. By diversifying suppliers, Brazil can avoid disruptions caused by geopolitical tensions or fluctuations in one region's market conditions, maintain a stable wheat supply, and keep prices competitive in the domestic market.

Ukraine is facing significant challenges in wheat production due to ongoing droughts and the impact of the war, which have led to a reduction in sown areas and lower yields. To counteract these issues, Ukraine should invest in climate-resilient wheat varieties more resistant to drought and extreme weather conditions. Varieties like drought-tolerant spring wheat (such as Karat or Albatross) can help reduce yield losses during dry spells. Furthermore, Ukraine should adopt modern irrigation technologies to improve water management, assisting crops to maintain optimal growth even in less favorable weather conditions. Collaborating with agricultural research institutions and focusing on seed breeding programs for drought-resistant varieties will be crucial for preserving wheat production stability. These measures will help mitigate the risks of extreme weather and strengthen Ukraine's competitiveness in global wheat markets.

Sources: Tridge, Hellenic Shipping News, Portal Do Agronegócio, UkrAgroConsult, Zol

Read more relevant content

Recommended suppliers for you

What to read next