Original content

The free trade agreement between the European Union (EU) and Mercosur, aimed at boosting South American rice imports into the EU, has been criticized by European rice growers for lacking reciprocity measures. They argue that the deal would allow agri-food imports that fail to meet the EU's strict environmental and food safety standards. The agreement introduces a zero-duty quota starting at 10 thousand metric tons (mt) in the first year, gradually increasing to 60 thousand mt annually, raising fears of unfair competition from South American exporters with lower costs and regulatory requirements. France is leading opposition efforts, seeking a blocking minority in the European Council (EC) to amend the agreement. Italy, a major rice producer in the EU, is under pressure to push for stricter provisions to protect European rice growers from potential negative impacts.

The Rio Grandense Rice Institute (IRGA) reports that 95.04% of the planned rice sowing area in Rio Grande do Sul for the 2024/25 harvest has been completed, covering 901,361 hectares (ha) out of the estimated 948,356 ha. However, progress in the central region lags at 68.87%, delayed by the May-24 floods. Despite this, IRGA's Rural Extension remains optimistic that planting in all areas except the central region will conclude by W51.

The Philippines experienced a surge in rice imports, reaching a record 4.35 million metric tons (mmt) by early Dec-24, surpassing the previous high of 3.61 mmt in 2023. This increase is primarily due to the government's decision to reduce tariffs on rice imports from 35% to 15% until 2028 to manage inflation. The Philippine Department of Agriculture (DOA) projects rice imports to reach 4.5 mmt in 2024, driven by a forecasted decline in domestic production. Vietnam has been the leading supplier, accounting for 76.8% of total imports, followed by Thailand and Pakistan.

Thailand's milled rice production for 2024/25 is forecasted at 20 mmt, up from 19.7 mmt in 2023/24, driven by improved yields and increased precipitation, according to the United States Department of Agriculture's (USDA) Foreign Agricultural Service (FAS). Thailand, the world's second-largest rice exporter, shipped 7.45 mmt in the first nine months of 2024, a 22% year-on-year (YoY) due to increased demand after India restricted its export on white and parboiled rice. Moreover, for the entire 2023/season, exports are expected to reach 9.2 mmt, a 5% YoY rise. However, 2024/25 exports are projected to decline by 18% to 7.5 mmt as India and Vietnam re-enter the market. Despite this, Thailand's premium fragrant rice offers substantial export opportunities.

With an average export price of USD 627.9/mt, Vietnam's rice exports reached 8.5 mmt and USD 5.31 billion in the first 11 months of 2024, marking a 10.6% and 22.4% YoY increase, respectively. The Philippines remained the largest market, accounting for 46.1% of exports, followed by Indonesia at 13.5% and Malaysia at 8.2%, with notable growth in all three markets. Vietnam's export value exceeded USD 5 billion for the first time in 2024, driven by a focus on high-quality and fragrant rice, which now makes up 20% of exports, alongside 70% of white rice. Investments in infrastructure and processing have helped Vietnam differentiate its rice industry, even as India's return to the export market has impacted lower-grade rice. Meanwhile, Thailand's rice exports are projected to surpass 9 mmt, valued at over USD 6.4 billion.

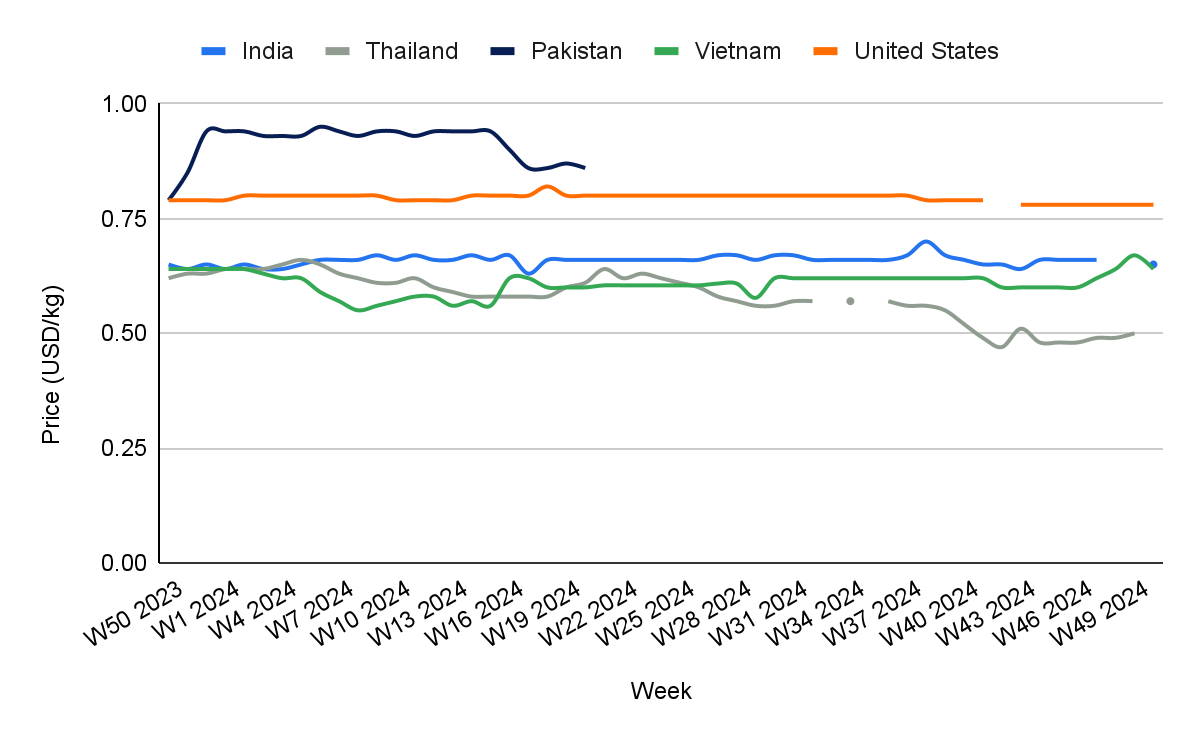

In W50, India’s wholesale rice prices fell by 2.99% week-on-week (WoW) and 1.52% month-on-month (MoM), reaching USD 0.65 per kilogram (kg). This marks a 15-month low, driven by the depreciation of the Indian rupee (INR) and increased supply. India’s rice stocks have reached a record high in Dec-24, over five times the government’s target, fueled by a 120 mmt harvest during the 2024 summer season, accounting for 85% of the country’s total rice production. This has led to a boost in international shipments. Meanwhile, the weakening INR has prompted traders to lower export prices. Demand from African countries has been strong, as they can now purchase rice at much lower prices than a month ago. In response to these market conditions, India removed the export tax on parboiled rice and lifted the floor price of USD 490/mt for non-basmati white rice to stimulate exports.

In W50, Vietnamese rice prices fell by 4.48% WoW, dropping to USD 0.64/kg from USD 0.67/kg in W49. White rice prices are under pressure due to increased global competition, with other origins vying for market share. In contrast, Vietnam’s fragrant rice varieties face little to no competition. While prices have softened, they haven’t fallen drastically, as demand remains low, except for government contracts like those with Indonesia. Supply is tight until the next harvest in Feb-24 or Mar-25, though some Cambodian paddy may be used in the interim. Furthermore, most buyers, except the Philippines, have secured their yearly rice needs. Prices could rise if demand picks up locally, as many exporters are running short ahead of the new crop.

In W50, the wholesale price of milled white long rice in Arkansas, US, was USD 0.78/kg, showing a 1.27% YoY decrease. This drop is due to increased rice production in the US, which reached around 7.6 mmt for the 2024/25 marketing year (MY). The higher supply has placed downward pressure on prices. Moreover, reduced global demand, particularly from key importers such as Mexico, the Philippines, and Indonesia, has further contributed to price instability. The strong US dollar (USD) has made US rice less competitive than other exporting countries.

Countries like India and Brazil should improve rice quality and reduce post-harvest losses by upgrading their infrastructure, particularly storage, drying, and milling facilities. By investing in modern processing technologies and improving logistical networks, rice producers can enhance the quality of their rice, reduce wastage, and increase competitiveness in international markets. For example, India could reduce the impact of fluctuating prices by offering higher-quality rice for export markets, potentially boosting its standing in premium price segments.

Rice-exporting countries like Vietnam, Thailand, and India should explore new and untapped markets to reduce reliance on a few major buyers. These countries can increase their market share and profit margins by expanding exports to regions such as Africa, where demand for affordable rice is growing, and investing in value-added rice products like organic or fortified rice. For instance, Vietnam's success in premium fragrant rice exports could be extended to other high-value rice varieties, such as red or black rice, providing a buffer against fluctuations in demand for bulk rice. Thailand and India could also expand their niche market presence by exporting rice products such as parboiled or specialty aromatic rice to diversify their export portfolio.

As climate change continues to impact rice production, countries like Thailand and Brazil should promote climate-resilient farming practices and invest in research for drought-tolerant rice varieties such as IR 64, Swarna Sub1, and DT 10. These varieties have been developed to withstand water stress and can provide stable yields even during periods of drought. Moreover, diversifying crops to include drought-resistant alternatives like sorghum or millet, which are more resilient to dry conditions, can help mitigate the risks of unpredictable weather patterns. Training farmers on sustainable water management techniques, such as improved irrigation systems and using moisture sensors or drip irrigation, will also ensure that rice production remains viable under increasingly erratic climatic conditions.

Sources: Tridge, Agricolae, Brecorder, Foodmate, Gmanetwork, Portal Do Agronegócio, UkrAgroConsult, Zol

Read more relevant content

Recommended suppliers for you

What to read next