News

Original content

According to Embrapa Café, global coffee exports totaled 150 million 60-kilogram (kg) bags between Oct-23 and Sep-24, driven by key coffee-producing regions. South America maintained its leadership with 66.13 million 60-kg bags, a 30.7% increase, led by Brazil's 34.3% growth to 49.03 million bags and Colombia's 13.7% rise to 11.91 million. Asia and Oceania recorded 40.62 million bags (27% of global exports) but saw a 6.7% decline, mainly due to Vietnam's 11.7% drop to 24.96 million bags, the lowest in a decade. Africa grew by 17.3% to 16.02 million bags, with Ethiopia leading this surge (63.5% increase to 5.59 million bags). Meanwhile, Mexico and Central America experienced mixed results, with a 4.1% drop to 14.51 million bags, driven by Honduras and Nicaragua's declines but offset by growth in Guatemala and Mexico. Instant coffee exports grew 11.6% to 12.82 million bags (8.8% of total exports), while roasted coffee sales remained limited to 71,000 bags.

With over 2 billion cups consumed daily worldwide, coffee's production heavily depends on specific climate conditions. Rising temperatures and erratic weather events threaten key producing regions like Latin America, Africa, and Asia, potentially shifting cultivation areas northward and reducing suitable land by up to 50% by 2050. Small-scale farmers who produce most of the world's coffee face challenges like droughts, floods, and diseases like coffee leaf rust. Experts suggest providing technical and economic support for these farmers and exploring the potential for coffee cultivation in new regions like Turkey, South Africa, and New Zealand as traditional areas become less viable.

Despite being the birthplace of coffee and a significant producer, Africa continues to struggle with fully capitalizing on the coffee trade due to challenges like lack of coordination and value addition. During the 64th Inter-African Coffee Organization High-Level Policy Forum in Addis Ababa, Ethiopian officials emphasized efforts to transform coffee production by improving productivity, quality, and market access. Aiming to earn over USD 2 billion in 2024/25, Ethiopia has planted billions of coffee seedlings and prioritized climate resilience and strategic policies. Additionally, discussions highlighted the importance of cooperation among African nations, strengthening regulatory frameworks, and expanding local coffee consumption to combat climate change and market volatility. The forum also proposed leveraging the African Free Trade Area to improve regional trade and address challenges like price fluctuations and financial shortages while encouraging investments in the coffee industry.

Brazil, the world's second-largest coffee consumer, has over 2 million hectares (ha) of coffee cultivation in the 2024/25 harvest. In Nov-24, total coffee exports (green and soluble) reached 4.904 million 60-kg sacks, marking a 21.8% increase compared to Nov-23's 4.027 million 60-kg sacks. This boost translated to an 84.4% rise in revenue, reaching USD 1.467 billion. From Jan-24 to Nov-24, total coffee exports amounted to 44.34 million sacks, up 35.73% year-on-year (YoY), with total revenues increasing by 54.66% to USD 11.219 billion.

The sharp rise in Arabica coffee prices, surging 70% in 2024 and reaching a 40-year high, has plunged major Brazilian producers into financial distress due to escalating margin calls estimated at USD 7 billion in Nov-24. Companies like Atlântica Exportação and Cafebras are seeking debt renegotiations to avoid bankruptcy, with the financial strain exacerbated by logistics costs and reduced crop yields from drought. This crisis parallels earlier commodity market disruptions, reflecting the mounting pressure on global coffee trade dynamics.

Colombia's coffee production is set to reach 13.6 million 60-kg bags in 2024, a 20% increase from 11.3 million bags in 2023, attributed to favorable weather conditions. As the world's third-largest coffee producer, Colombia expects export revenues of approximately USD 3.14 billion, with the United States (US) and Canada accounting for 45% of its exports. Colombia's coffee sector supports 540 thousand families across 842 thousand ha, marking a strong recovery after three years of decline.

Vietnam's coffee market is experiencing unprecedented developments during its peak harvest in Dec-24. Despite traditionally lower prices during this period, a sharp rise is observed, driven by a significant decline in output due to poor harvests and rising domestic and Chinese demand. While export volumes dropped 15.4% YoY in the first 11 months, export turnover surged 32.8% due to high prices. Experts urge caution against overexpansion of coffee acreage, emphasizing financial planning and sustainability amid unpredictable market dynamics.

In Vietnam, the 2023/24 coffee harvest in Đắk Lắk saw a production drop of 23,057 tons due to prolonged drought linked to climate change and pest infestations. Coffee-growing areas decreased by 809 ha to 212,106 ha, with an average yield falling to 2.67 tons/ha. Despite record-high coffee prices, doubling from the previous year, many farmers reported losses of up to 50% in production. Around 18,762.9 ha suffered damage, with over 1,044 ha destroyed. Driven by El Niño and mealybug outbreaks, these challenges have severely affected Vietnam's coffee industry despite efforts to adopt modern farming techniques.

_21.18.57.png)

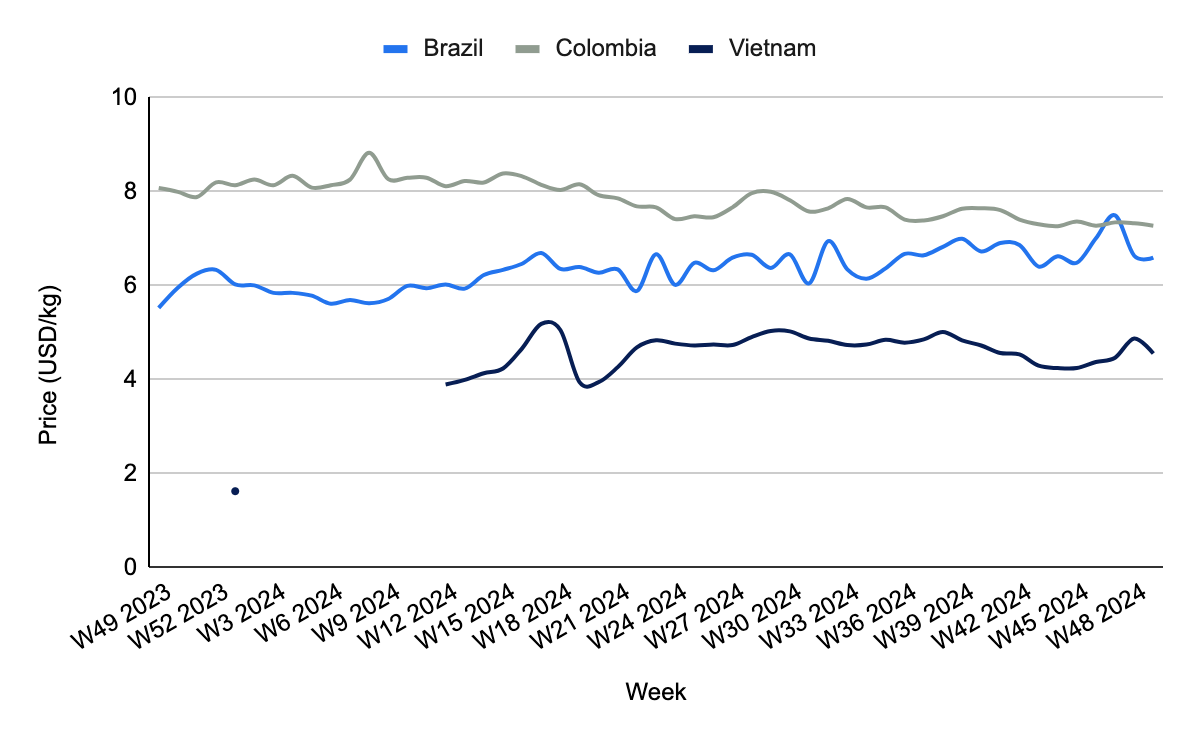

Coffee prices have shown relative stability week-over-week (WoW), with a slight decrease of 0.60% in W49. Prices have dropped by 5.85% month-over-month (MoM) as the market adjusts following a peak observed in W47. Despite these recent fluctuations, prices have remained elevated compared to historical norms, with a 19.35% increase YoY. This YoY rise is driven by global supply concerns, primarily droughts in key coffee-producing countries, including Brazil, and the introduction of the European Union Deforestation Regulation (EUDR), which adds geopolitical risk to global supply chains. Furthermore, fears of further declines in Brazil's Arabica production for 2025 due to ongoing weather disruptions and a tightening supply chain are adding pressure to markets. Additionally, strong international demand has bolstered the upward trend. The 2024 market growth suggests that the industry might continue to grow in 2025.

Coffee prices in Colombia have shown relative stability in both WoW and MoM. WoW prices dropped slightly by 0.68%, while MoM prices remained unchanged, reflecting market steadiness. Despite this, YoY prices have fallen by 9.90%. This YoY decline is primarily driven by increased production. Colombia's coffee output is expected to reach 13.6 million 60-kg bags by 2024, a 20% rise from 2023, thanks to favorable weather conditions. This recovery signals improved productivity following three years of decline. The increasing supply will aid in easing pricing in the upcoming months if demand remains stable.

Vietnam's coffee prices dropped by 6.56% WoW in W49, as they stabilized after peaking in W48. Despite this, prices increased by 4.11% MoM, driven by supply challenges from poor harvests, climate issues, and pests. The 2023/24 harvest in Đắk Lắk dropped by 23,057 tons due to drought, El Niño, and mealybugs, with yields falling to 2.67 tons/ha. Coffee-growing areas shrank by 809 ha. International demand remains high, further influencing higher prices this year due to supply constraints and strong global consumption.

Coffee importers, multinational coffee companies, and roasters should prioritize building diversified supply chain networks by partnering with multiple coffee-producing regions. This will reduce dependency on single areas vulnerable to droughts, supply disruptions, or geopolitical risks. Additionally, strengthening logistics partnerships will ensure a stable flow of coffee supplies, even during market fluctuations. Establishing long-term agreements with emerging markets will provide stability and security in meeting global demand.

Coffee exporters and trade organizations should intensify efforts to tap into growing international markets by targeting regions such as Southeast Asia, China, and North America. Strategic partnerships with local distributors and retailers can create smoother entry points into these markets. Additionally, promoting coffee products through marketing campaigns focused on sustainability, ethical sourcing, and specialty coffee options will align with consumer preferences and drive demand growth in these regions.

Financial hedging tools and strategic market monitoring are essential for coffee traders and large companies to manage price volatility, particularly in markets like Vietnam. Implementing futures contracts can mitigate the risk of sudden price swings caused by weather events or supply disruptions. Regularly tracking weather patterns, harvest forecasts, and market shifts can allow proactive responses to supply chain disruptions. Technological innovations in supply chain operations and production methods should also be adopted to maintain competitive costs.

Sources: Tridge, All Africa, Canal Rural, Dan Viet, EkoTrent, Nong Nghiep, Noticias Agricolas, Portal do Agronegocio, Son Dakika, VHO Online, Vina Net

Read more relevant content

Recommended suppliers for you

What to read next