News

Original content

The global beef market is ending 2024 with a significant price recovery, driven by supply adjustments in Brazil as it transitions production cycles and replenishes stocks, reducing meat availability. Regional cattle prices rose sharply, from USD 2.90 per kilogram (kg) to USD 3.85/kg of carcass, reflecting robust demand. Optimism for 2025 remains high, with projections of sustained demand and record prices, though macroeconomic factors like United States (US) inflation and currency fluctuations may create headwinds.

Brazil’s reduced exports have tightened global supply, with key markets like the US and China driving demand. US beef production is expected to decline further, boosting import demand even as protectionist policies may raise costs. While passing higher import prices to consumers is challenging in China, strong demand and limited supply should maintain market stability. Brazilian exporters have already secured higher prices from Chinese buyers, reinforcing expectations of a firm market.

The US and China are set to remain pivotal in sustaining demand. Despite uncertainties, including potential global tariffs and economic fluctuations, reduced supply from major exporters and strong import needs in key regions suggest a positive outlook for the global beef market in 2025.

Global beef supply is projected to decline by 1% year-on-year (YoY) in 2025, marking the first reduction since the COVID-19 pandemic, according to Rabobank. Shrinking herds in major producers like Brazil, the US, China, Europe, and New Zealand drive this projection. Australia expects to be the only top-10 producer to see YoY increases, supported by favorable rainfall. High North American cattle prices, fueled by tight supply and strong demand, are set to influence rising prices in South America, Australia, and New Zealand as global beef trade adjusts. Brazilian producers will likely focus on exports amidst weak domestic demand, while Australian producers will rely on international markets to absorb higher production. US production is constrained by delayed herd rebuilding due to ongoing drought, though recent seasonal cooling offers hope for recovery. El Niño is forecasted to persist through early 2025, transitioning to neutral conditions mid-year, favoring Australian production while maintaining global weather challenges.

Australia’s beef exports significantly rose in 2024, with a 27% YoY increase to 118.89 thousand metric tons (mt). This growth was primarily driven by exports to the US, which surged by 79% to 35.03 thousand mt, accounting for 30% of total exports. North Asian markets remained stable, with South Korea ranking as the second-largest market with a 5% YoY increase to 19 thousand mt. Exports to Japan experienced a slight decline of 2% to 17.52 thousand mt, while shipments to China held steady at 16.34 thousand mt. Meanwhile, Southeast Asia demonstrated remarkable growth, with Indonesia recording a 50% YoY increase, the Philippines receiving an additional 2.43 thousand mt, and Vietnam’s imports doubling to 2.02 thousand mt.

Year-to-date, Australia exported 1.22 million metric tons (mmt) of beef, marking a 25% increase from the first 11 months of 2023 and positioning the country close to its all-time calendar year record set in 2014. High weekly slaughter rates in recent months suggest that the record could be surpassed. According to the Australian Bureau of Statistics, Q3-2024 also set milestones, with beef production rising 4.6% to 658.47 thousand mt compared to Q2-2024. Meat and Livestock Australia (MLA) reported record-high beef production and cattle sales during this period, with slaughter-ready cattle from Aug-24 to Oct-24 generating over USD 4.19 billion (EUR 4 billion). However, the cattle population slightly declined, attributed to herd stabilization after years of rebuilding.

Brazil’s beef exports to the European Union (EU) could more than double with implementing the EU-Mercosur free trade agreement. Under this agreement, Mercosur countries, including Brazil, will be allowed to export 99 thousand mt of beef to the EU at a reduced tax rate of 7.5%, split between chilled and frozen categories, alongside the exemption of the existing Hilton Quota tax. Brazil, already supplying 86% of European beef demand, is well-positioned to capitalize on the new quota despite concerns over compliance with EU standards, including animal welfare and food safety requirements.

The agreement has sparked significant opposition, particularly from EU member states such as Ireland, France, and Poland, as well as consumer and farmer organizations. Critics argue that the EU lacks regulations to ensure imported products meet the same standards as domestic goods, particularly regarding animal welfare and environmental sustainability. This has led to accusations that the deal contradicts the EU’s Green Deal strategy, which aims to promote sustainable consumption and reduce reliance on meat products. Consumer groups warn that the agreement may disproportionately impact consumers, who may face lower-quality products, while farmers could receive financial compensation for potential losses.

Despite these challenges, the European Commission continues to push for the deal’s finalization, with negotiations nearing conclusion. While opposition remains, particularly from countries concerned about agricultural impacts, the agreement is expected to be approved by a qualified majority of member states. If implemented, it could significantly boost Brazil’s beef exports while raising questions about the balance between trade liberalization, sustainability, and consumer protection within the EU.

Data from the Secretariat of Foreign Trade (Secex) revealed that Brazil’s beef exports totaled 228.1 thousand mt, valued at USD 1.11 billion in Nov-24. These figures indicate a significant YoY growth of 21.4% in volume and 28.5% in value compared to Nov-23. According to the Brazilian Association of Meat Exporting Industries (ABIEC), despite a 15.6% MoM decline in export volume, Nov-24 achieved the fourth-best monthly performance of the year.

China remained the primary destination for Brazilian beef shipments. However, market experts are cautious about potential adjustments in Chinese demand. Agrifatto, a leading agricultural market intelligence company, noted that negotiated beef will be shipped in Jan-25 and arrive in China by Feb-25, after the Chinese New Year celebrations. A demand reduction typically marks this period.

Droughts on Canada’s prairies, fueled by global warming, have driven beef prices to record highs, with ground beef reaching USD 13/kg in Sep-24, up from USD 11.69 last year and USD 9 five years ago. Tenderloin rose to over USD 32/kg, while cattle prices in Alberta climbed 7.6% YoY to USD 236.08 per hundredweight, reflecting a 45% to 65% increase over five years. The Canadian cattle population, at its lowest since 1987, has declined due to high feed costs and prolonged droughts, reducing beef supplies. Despite limited availability, strong consumer demand continues, with experts predicting high prices until 2026 as ranchers consider herd expansion amid improved profit margins. Grocery food prices overall have risen 2.7% in the past year, amplifying inflation in the meat sector.

China has lifted trade restrictions on two Australian meat processing facilities, allowing the full resumption of red meat exports to the country. This marks the removal of all 10 abattoir bans imposed between 2020 and 2022 during diplomatic tensions. China is Australia's second-largest market for beef and veal, importing around 200 thousand mt annually, valued at USD 1.5 billion. While the bans were in place, other Australian processors continued to export beef to China. Australian beef exports surged in 2024, mainly to the US and Japan, as US production declined.

Irish beef exports to South Korea have resumed following the lifting of a suspension imposed due to an atypical case of bovine spongiform encephalopathy (BSE) detected in a cow in Sep-24. On December 2, 2024, the Department of Agriculture, Food and the Marine (DAFM) informed Food Business Operators (FBOs) that beef produced at all FBOs approved to export to South Korea from November 29, 2024, could now be shipped to South Korea. The suspension had been enacted on September 19, 2024, after the BSE case was identified. However, following a thorough review by Korean authorities, including receiving and addressing two detailed questionnaires, the suspension was lifted.

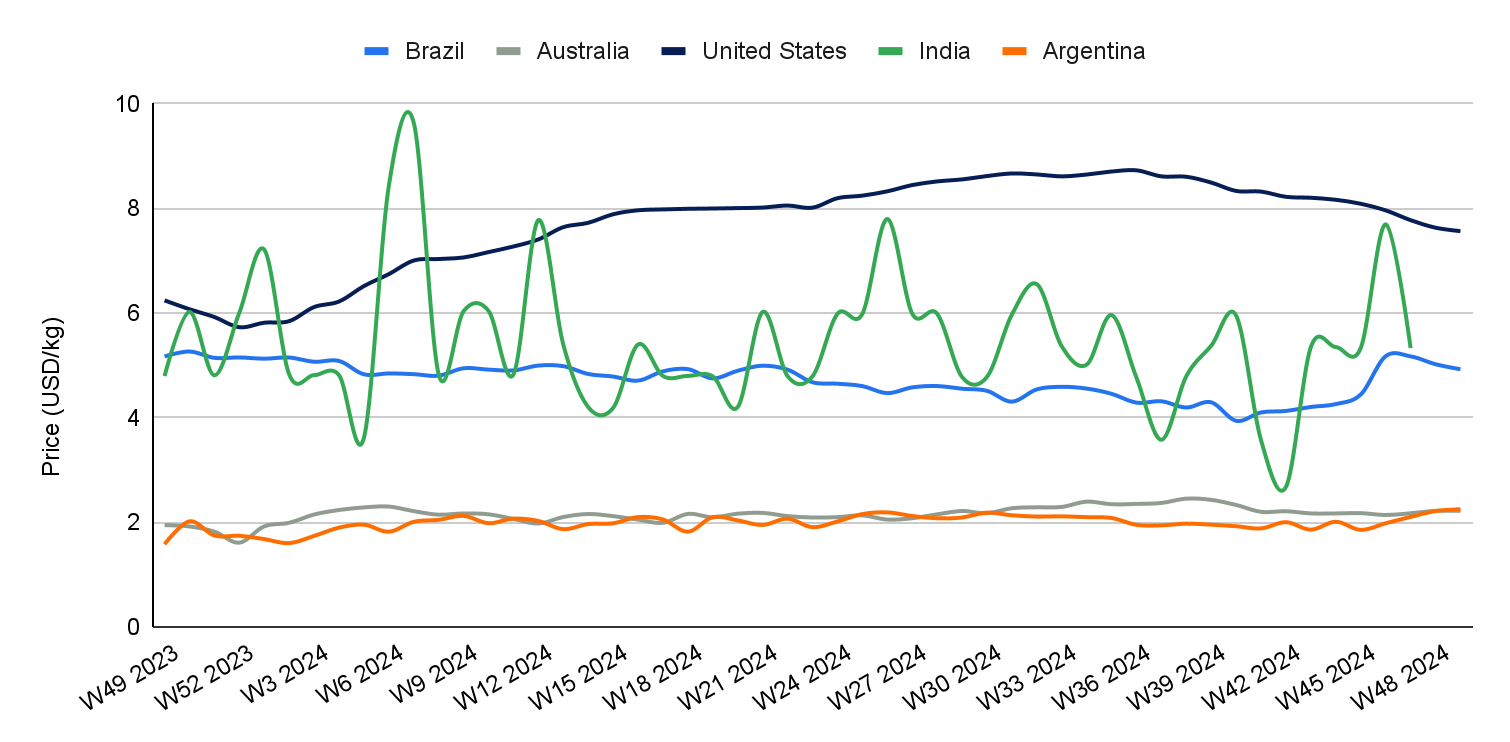

In W49, Brazil's wholesale price for boneless rear beef decreased by 1.92% week-on-week (WoW), reaching USD 4.92/kg. This also reflects a 4.82% month-on-month (MoM) decline and a 4.73% YoY drop. However, when measured in Brazilian real, the price remained stable WoW at BRL 30/kg, indicating that the price drop in USD was primarily due to fluctuations in the exchange rate. According to Canal Rural, wholesale prices in Brazil remain firm, with limited room for further price increases. This is due to challenges in passing on price hikes to end consumers, even amid high demand, as well as increasing competition from alternative proteins, particularly chicken meat.

In W49, Australia's National Young Cattle Indicator averaged USD 2.22/kg, showing a slight 0.03% WoW decrease. However, the price saw a 3.67% MoM increase and a 14.06% YoY rise. According to MLA, the cattle market remained firm, following the trends observed in the previous month. The heifer market experienced an uptick, with steers also following suit, maintaining a 28% gap between restockers. Although feeder steer prices rose, reduced yardings indicated a softening demand for feeder animals.

In W49, the price of lean beef (92% to 94%) in the US averaged USD 7.57/kg, marking a 0.86% WoW decline and the thirteenth consecutive week of price drops, reaching its lowest level since W12. This also represents a 4.98% MoM decrease. Despite the recent drop, prices are still 21.22% YoY higher, driven by a tightening domestic supply due to a shrinking cow herd. The price decline follows the typical seasonal dip in demand during winter, after the peak consumption in summer. However, the continued limited production keeps lean beef prices relatively high overall.

In W49, Argentina's average steer beef price rose to USD 2.25/kg, reflecting a 1.60% WoW increase, a 13.51% MoM rise, and a 42.34% YoY uptick. This marks the fourth consecutive weekly price hike, likely driven by increased demand and a seasonal drop in supply. The cattle market is reactivating with significant price increases, particularly for young bulls, females, and steers, which reached historic highs across several categories. Market trends indicate that the seasonal decrease in supply follows a typical pattern, with calves sold between January and May for rearing and fattening becoming available from June and July and volumes declining by November. Experts predict that prices will remain stable until February, when new wintering lots are expected to enter the market. However, they note that unique demand-side factors this year prevented further price hikes from being validated.

As Brazil’s beef exports to the EU are set to rise due to the EU-Mercosur free trade agreement, it is crucial for Brazilian producers to ensure full compliance with EU standards, particularly regarding animal welfare and food safety. Given the EU’s scrutiny, addressing concerns raised by member states and consumer groups will be pivotal in sustaining access to the European market. Brazil should invest in transparent certification processes and regular audits to guarantee that beef exports meet the EU’s stringent quality standards, minimizing risks of trade disruptions.

Canada’s beef prices have surged due to prolonged droughts and a declining cattle population. In response, it is essential for Canadian ranchers to focus on sustainable herd management practices, such as improving feed efficiency and adopting drought-resistant grazing techniques, to stabilize supply in the long term. Furthermore, incentivizing the expansion of cattle herds through financial support for ranchers will help increase beef production, ensuring supply meets the ongoing high demand and mitigating the effects of extreme weather conditions on the industry.

Australia has seen significant increases in beef exports to Southeast Asia and North Asia, with markets such as Indonesia and the Philippines recording impressive growth. To sustain this upward trajectory, Australian beef producers should focus on expanding their footprint in emerging markets outside of traditional North Asian partners. Strengthening ties with countries in Africa, the Middle East, and Latin America could diversify export sources, reduce dependency on a few key markets, and further boost export growth. Targeted marketing and building long-term trade relationships with these regions will ensure continued demand stability.

Sources: Tridge, Agri Land, Agro meat, Canal Rural, Elagro, Euro Meat, Farmer.pl, Irishtimes, MLA, Portal Do Agronegócio, The Cattle Site

Read more relevant content

Recommended suppliers for you

What to read next