News

Original content

Global beef prices have risen sharply in the past month, with carcass prices increasing across most markets except Australia. In Belgium, cow prices reached USD 7.36 per kilogram (EUR 7/kg) of slaughtered weight, reflecting a shrinking global beef market. Rabobank predicts declining livestock populations in major beef-producing countries. Brazil and the United States (US) are expected to see significant declines in beef production by 2025, at -5% year-on-year (YoY) and -3% YoY, respectively. Similar drops are anticipated in China, Europe, and New Zealand, while Australia may experience growth. Tightened supply has driven higher cattle prices globally, reshaping trade flows as Australia relies more on exports and Brazil shifts focus to stronger global markets.

Weather patterns are further impacting production. In the US and Brazil, delayed rainfall hinders herd rebuilding, while Australia's recent favorable precipitation could shift with looming droughts. In the United Kingdom (UK), the Agriculture and Horticulture Development Board (AHDB) forecasts a 6.3% drop in slaughter supply by 2030 compared to 2023, driven by a sharp decline in suckler cow numbers. Stable domestic demand is expected to reduce the country’s self-sufficiency in beef, reflecting broader global pressures on the market.

Brazilian representatives in the Mercosur Parliament (Parlasul) will address recent boycotts of South American beef at the upcoming Plenary Session in Dec-24 in Uruguay. Led by French retailers Carrefour and Les Mousquetaires over alleged quality concerns, the boycotts have sparked a backlash from Brazilian officials. Carrefour later apologized to Brazil’s Minister of Agriculture following public criticism and supply chain disruptions. Senators expressed concern over the harm to producers who meet strict export standards, emphasizing the need for action to protect Mercosur’s agricultural sector.

The tension resulted from a European Union (EU) producer opposing the proposed Mercosur-EU free trade agreement, with French protests and inflammatory remarks drawing condemnation from Brazilian officials. The Brazilian president reaffirmed his commitment to advancing the deal through the European Commission (EC), dismissing French resistance. Parlasul representatives plan to advocate for Mercosur producers, urging fair trade practices and stronger dialogue with the EU to counteract the boycotts.

The Eurasian Economic Commission (EEC) Council has approved Russia’s duty-free import of up to 100 thousand metric tons (mt) of cattle meat in 2025 for industrial processing. Other member states of the Eurasian Economic Union (EAEU) will also benefit from allocated import volumes: Armenia up to 9 thousand mt, Belarus 7.5 thousand mt, and Kyrgyzstan 2.5 thousand mt. This measure aims to address the meat deficit in the EEC, reduce production costs for meat products, and curb price increases. Imports will primarily come from Latin America and India. The tariff exemption applies exclusively to meat intended for industrial processing and excludes high-quality beef, which is produced domestically. Importers must verify the intended use of the meat through authorized bodies.

The US is expected to reopen its border to Mexican cattle exports on December 15, 2024, following the containment of the screwworm threat, according to the National Confederation of Livestock Organizations (CNOG). Cattle imports from Mexico were restricted from November 22, 2024. Around 75 thousand cattle are currently under quarantine, incurring an economic impact of USD 75 million due to investments in medication and food. The suspension of Mexican beef exports was triggered by a screwworm case detected in cattle from Central America en route to Nuevo León. However, CNOG clarified that the infestation was not found in Mexican cattle, which are undergoing disinfection protocols as a precaution.

Efforts are underway to treat affected cattle with Ivermectin and to prevent further outbreaks. CNOG called for increased border inspections by the National Guard along the Guatemala-Mexico border to address the illegal entry of an estimated 20 thousand cattle from Central America. The screwworm, caused by larvae of the fly Cochliomyia hominivorax, poses a serious threat by feeding on the living tissue of mammals. Mexico has maintained its screwworm-free status since 1991 through stringent surveillance and measures by the National Service of Health, Safety, and Food Quality (SENASICA). The current emergency response highlights the country’s commitment to protecting its livestock and export reputation.

US meat exports to Cuba are seeing significant growth after years of limited market penetration, driven by increased private-sector purchases. The United States Meat Export Federation (USMEF) recently hosted an educational seminar in Miami to support US companies and Cuban buyers to understand various trade regulations. Through Sep-24, US beef exports to Cuba, primarily canned products, surged over 1,500% YoY, totaling 3.23 thousand mt and valued at USD 5.4 million, up 519% YoY. These numbers reflect growing opportunities in the Cuban market, with US exporters now having access to thousands of buyers rather than being limited to a single importer.

Similarly, US beef exports to South Korea showed positive trends. Sep-24 shipments reached 18.08 thousand mt, up slightly YoY, with a value increase of 10% YoY to USD 175.5 million. From Jan-24 to Sep-24, South Korea remained the top value market for US beef, with shipments valued at USD 1.6 billion, a 2% YoY increase despite a 10% YoY drop in volume to 169.15 thousand mt. This demonstrates strong demand for US beef in high-value markets alongside emerging opportunities in Cuba.

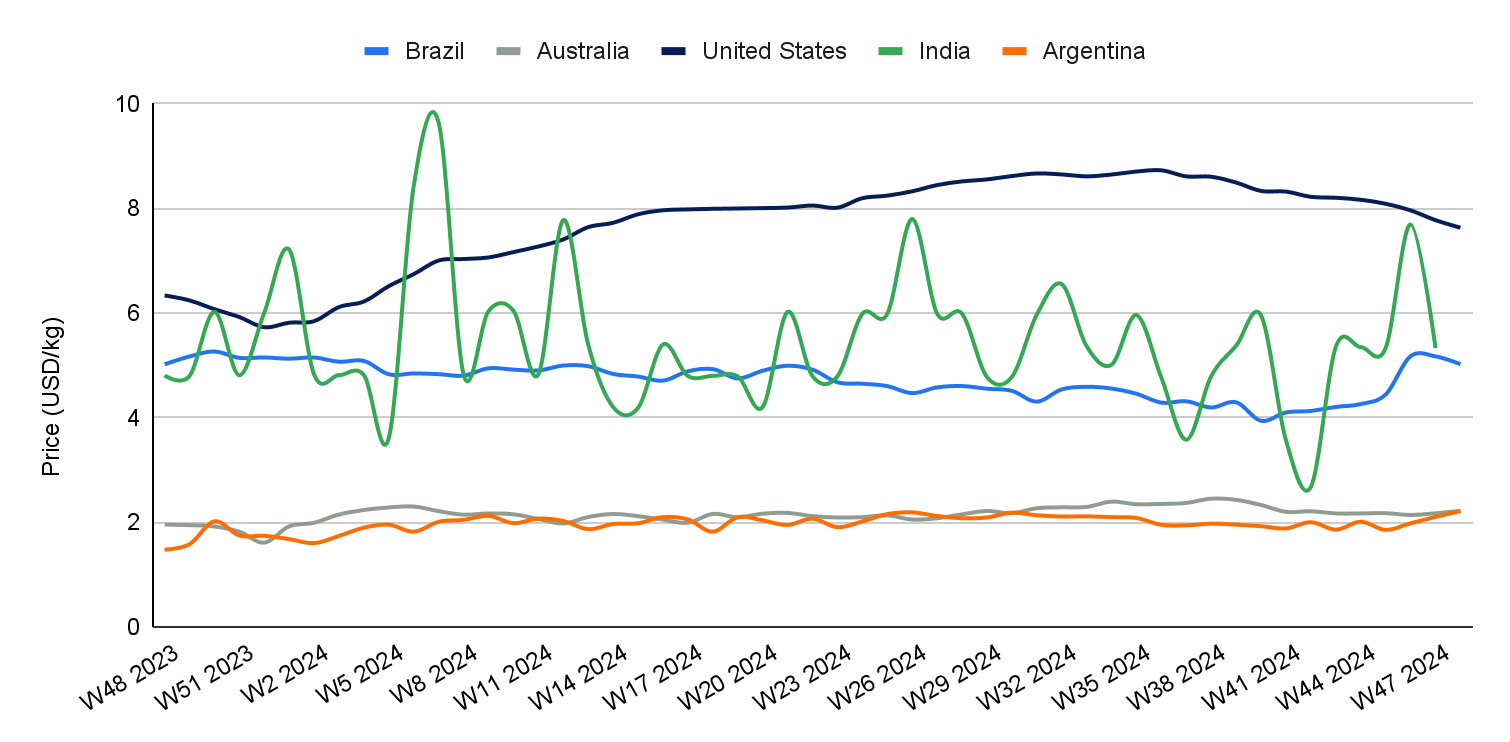

In W48, Brazil's wholesale price for boneless rear beef decreased by 2.91% week-on-week (WoW), reaching USD 5.02/kg. However, this still represents a 13.02% month-on-month (MoM) increase and a slight 0.04% YoY rise. In Brazilian real, the price remained steady at BRL 30/kg, suggesting that the price drop in USD was linked to fluctuations in the exchange rate. According to Safras and Mercado, the wholesale beef market showed higher prices early in the week, with expectations of short-term price adjustments. However, the limited purchasing power of the Brazilian population continues to hinder more consistent price increases. A drop in purchasing power towards the end of Nov-24 slowed meat sales at both wholesale and retail levels, limiting the rise in cattle prices. Additionally, the recent uptick in cattle and beef prices further contributed to the slowdown in sales, which is expected to continue until wages are paid.

In W48, Australia’s National Young Cattle Indicator averaged USD 2.22/kg, reflecting a 2.13% WoW increase, a 2.03% MoM rise, and a notable 13.43% YoY gain. According to Meat and Livestock (MLA), the cattle market remained stable, although yardings decreased by 13.54 thousand heads. Throughput at some saleyards was subdued due to favorable rainfall in the past week. The Feeder Steer Indicator rose, with Dalby recording the highest cattle yarding in the country at 7.47 thousand heads. Prices eased across eastern states, with limited competition between feeders and restocker buyers. While the availability of well-finished cattle helped stabilize prices, the market appeared erratic for domestic and export buyers.

In W48, the price of lean beef (92% to 94%) in the US averaged USD 7.63/kg, marking a 1.86% WoW decline and the twelfth consecutive week of price drops, reaching its lowest level since W12. This also represents a 5.66% MoM decrease. Despite the recent drop, prices remain 20.44% YoY higher, driven by a tightening domestic supply due to a shrinking cow herd. The price decline aligns with the typical seasonal dip in demand during winter, following the peak consumption in summer. However, the continued limited production keeps lean beef prices relatively high overall.

In W48, Argentina's average steer beef price increased to USD 2.21/kg, reflecting a 5.27% WoW rise, a 19.38% MoM increase, and a 49.99% YoY uptick. This marks the third consecutive weekly price hike, likely driven by increased demand and a seasonal drop in supply. According to the latest report from the Argentine Feedlot Chamber, the occupancy rate at the beginning of Nov-24 was 66%, lower than the past seven months and also lower than Nov-23, a year marked by abundant supply. However, it was higher than the same period in 2022, 2021, and 2020, where the average occupancy was 53%. Market trends indicate that this seasonal decrease in supply follows a typical pattern, with calves sold between January and May for rearing and fattening starting to be available from June and July, and volumes declining by November. Experts predict that prices will remain sustained until February, when new wintering lots begin to enter the market next year. However, they note that this year saw unique demand-side factors that prevented the validation of further price hikes.

As global beef production faces declines, particularly in major producers like the US, Brazil, and Argentina, countries should consider diversifying their trade relations and beef sourcing strategies. Establishing stronger trade agreements with emerging markets such as Asia, the Middle East, and Africa can reduce reliance on traditional markets and mitigate the effects of shrinking herds. Investments in sustainable farming practices, such as drought-resistant feed and water-efficient technologies, will also be crucial in adapting to shifting weather patterns.

In light of the beef boycott and tensions surrounding the Mercosur-EU trade deal, Brazil should strengthen its brand reputation by showcasing adherence to strict international quality standards. Additionally, diversifying its export markets beyond Europe by focusing on growing demand in Asia and the Middle East will help mitigate the impacts of EU trade tensions. Greater diplomatic engagement with EU stakeholders, addressing concerns transparently, can open new growth opportunities.

EAEU member countries, including Russia, should seize the opportunity provided by the EEC’s decision to allow duty-free imports of cattle meat in 2025. This policy can help stabilize domestic meat markets by filling the deficit gap. It is recommended that these countries strengthen their local processing capabilities to maximize value-added production, reduce dependence on imported raw materials, and boost the competitiveness of domestic meat products.

US beef exporters should focus on capitalizing on the significant growth in emerging markets, particularly in Cuba and South Korea. Increasing educational efforts, such as seminars and trade events, will help US companies navigate complex trade regulations while building relationships with private sector buyers in Cuba. Simultaneously, strengthening partnerships with South Korean buyers and maintaining high-value product exports will further solidify the US’s position as a leading supplier of premium beef in these growing markets.

Sources: Tridge, Agromeat, BR Money times, Kvedomosti, The Cattle Site, Veeteelt

Read more relevant content

Recommended suppliers for you

What to read next