OPINIO

Original content

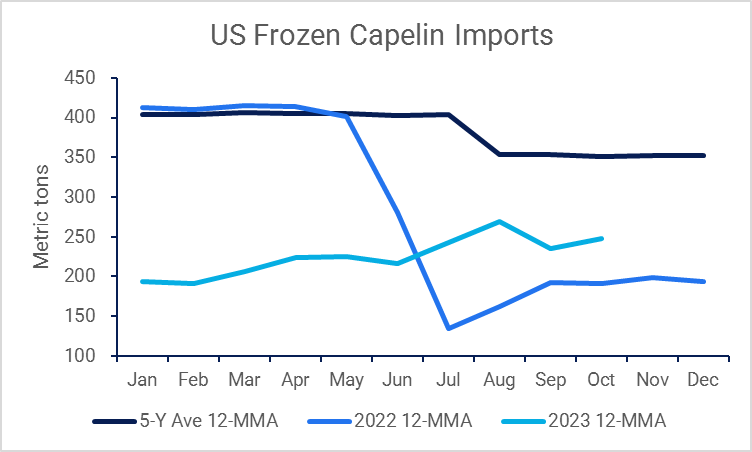

According to data from the United States Department of Agriculture (USDA), the United States (US) imported a total of 2.83 thousand metric tons (mt) of frozen capelin from Jan-23 to Oct-23. This was valued at USD 3.5 million, representing an average price of USD 1.25 per kilogram (kg). Volume imported during the aforementioned period rose 29% year-on-year (YoY), while its value grew by 38% YoY as the average price rose by 7% YoY. While the increase was significant, it’s worth noting that it comes from an abnormally low base in 2022. Volume and value were down by 30% compared to their five-year average, while the average import price is also down by 11%.

Overall inflationary pressure affected the market in 2022 despite a higher supply. The bulk of US imports came from Canada and occurred in July and August (just after the Canadian harvest season). Capelin imports from 2012 to 2018 remained virtually unchanged at an average of around 5.5 thousand mt a year. Imports fluctuated from 2019 to 2021 at lower levels but plunged to decade lows in 2022. In 2021, the US imported 2.65 thousand mt in July and August. However, during the same months in 2023, the US imported only 1.23 thousand mt, less than half of the amount of the previous year.

In 2021, the total allowable catch (TAC) for capelin was 9.29 thousand mt in the Gulf of St. Lawrence and 14.53 thousand mt in the coasts of Newfoundland and Labrador in Canada. For 2022, the TAC for St. Lawrence rose to 10.23 thousand mt, while the one for the other Canadian locations remained the same.

Aside from Canada, other large import origins include Norway and Iceland. In 2021, Norwegian and Icelandic fisheries in the Barents Sea reopened after a two-year ban. This development, coupled with the slightly higher supply in Canada, led to a high supply during 2022. This was reflected in US import prices from Canada, which declined by 50% and 53%, respectively, during Jul-22 and Aug-22. Nonetheless, demand fell as overall inflationary pressures led the US market to seek cheaper substitutes such as sardines.

This year, prices remained mostly unchanged from the previous year during July and August, but as overall inflation eased, demand picked up again. However, it’s worth noting that the 2024 price outlook seems bullish.

Source: USDA, Tridge

Lower imports from Canada this year and the previous were partly offset by more imports from Iceland. Yet, Iceland’s supply will substantially decrease in 2024.

2024 TACs for Barents Sea Triple from 2023, but Zero TAC expected for Iceland.

In late October of this year, Norway and Russia agreed on fishing quotas in the Barents Sea for 2024. According to the Barents Observer, the capelin quota was set at 196 thousand mt, which represents almost three times compared to this year. It's worth noting that the increase in the capelin quota comes with a decline of the cod quota. Capelin is a food source for cod.

Meanwhile, according to the Fisker Forum, in early Oct-23, the Iceland Marine and Freshwater Research Institute advised a catch of zero capelin for the 2023/2024 winter season. However, the advice is set for a revision in early 2024 (January/February). The Fisker Forum mentioned that the capelin juveniles figure was estimated at around 48 billion, which falls short of the 50 billion threshold to advise a non-zero catch. The previous TAC had been 275 thousand mt. The net effect would be a decline in capelin supply, which is why prices will face upward pressure in the upcoming year.

Read more relevant content

Recommended suppliers for you

What to read next