OPINIO

Original content

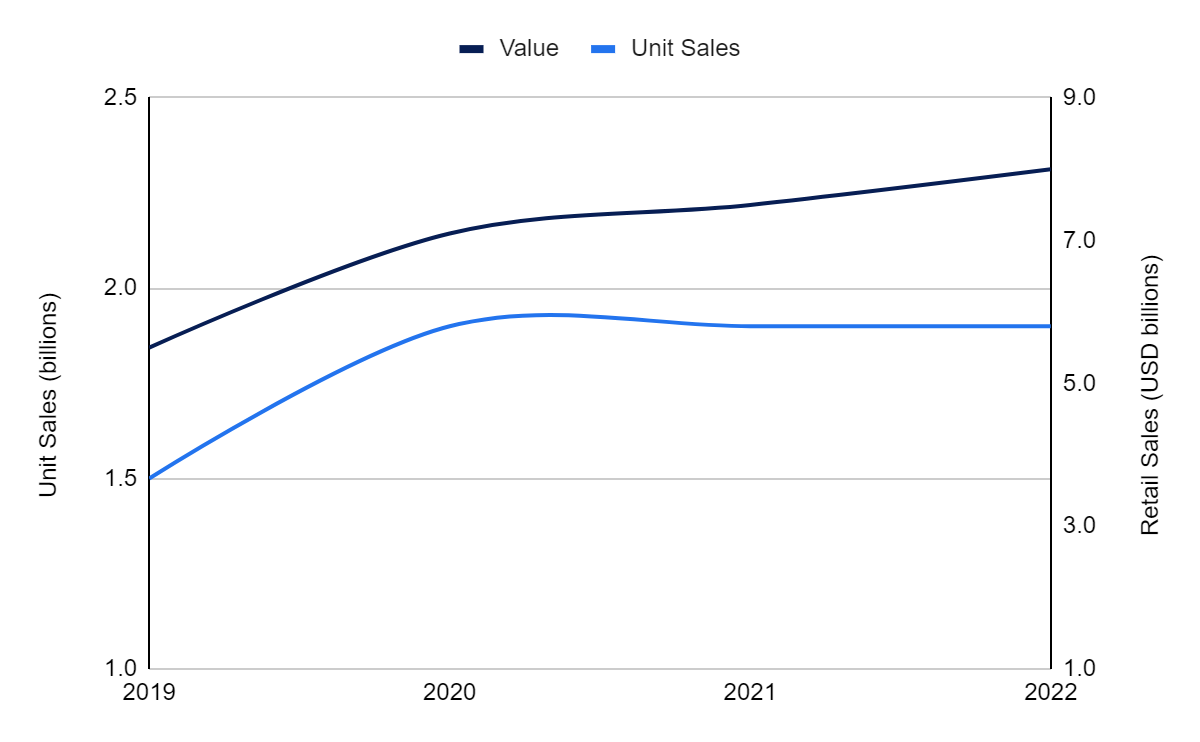

According to the Good Food Institute (GFI), retail sales of plant-based alternatives across the United States (US) was worth USD 8 billion in 2022, with a year-on-year (YoY) increase of 7% in value and a 3% decrease in unit sales. The increase in sales value is a result of price increases as evidenced by the decrease in unit sales. This trend was broadly in line with the total food and beverage and animal-based food sectors. The sales value of PBAs in the US grew at a compound annual growth rate (CAGR) of 13% between 2019 and 2022 and grew 44% in total over the period. Unit sales of PBAs in the US grew at a CAGR of 7% between 2019 and 2022 for a total growth of 23%. Over this three year period, growth in sales value almost doubled that of unit sales, suggesting that prices of PBAs are increasing at a rapid rate.

Figure 1. US plant-based retail sales from 2019 to 2022

In 2022, six in 10 US households purchased plant-based food options as part of their grocery basket. However, plant-based foods made up only 1.4% of total retail food and beverage sales in terms of revenue in the same year. Furthermore, 93% of households that bought plant-based meat in 2022 also bought animal based meat. This suggests that the vast majority of US consumers still primarily engage in animal-based diets, with plant-based food options only making up a small portion of their spending. Thus, there is still considerable room for growth for the plant-based food industry in the US market.

Table 1. US plant-based food sales and growth

As illustrated in Table 1, several plant-based categories in the US market experienced high levels of growth in recent years including creamer, eggs, and cream cheese, sour cream, and spreads. Other notable categories which experienced particular growth in 2022 are protein powders, butter, ready-to-drink (RTD) beverages and baked goods.

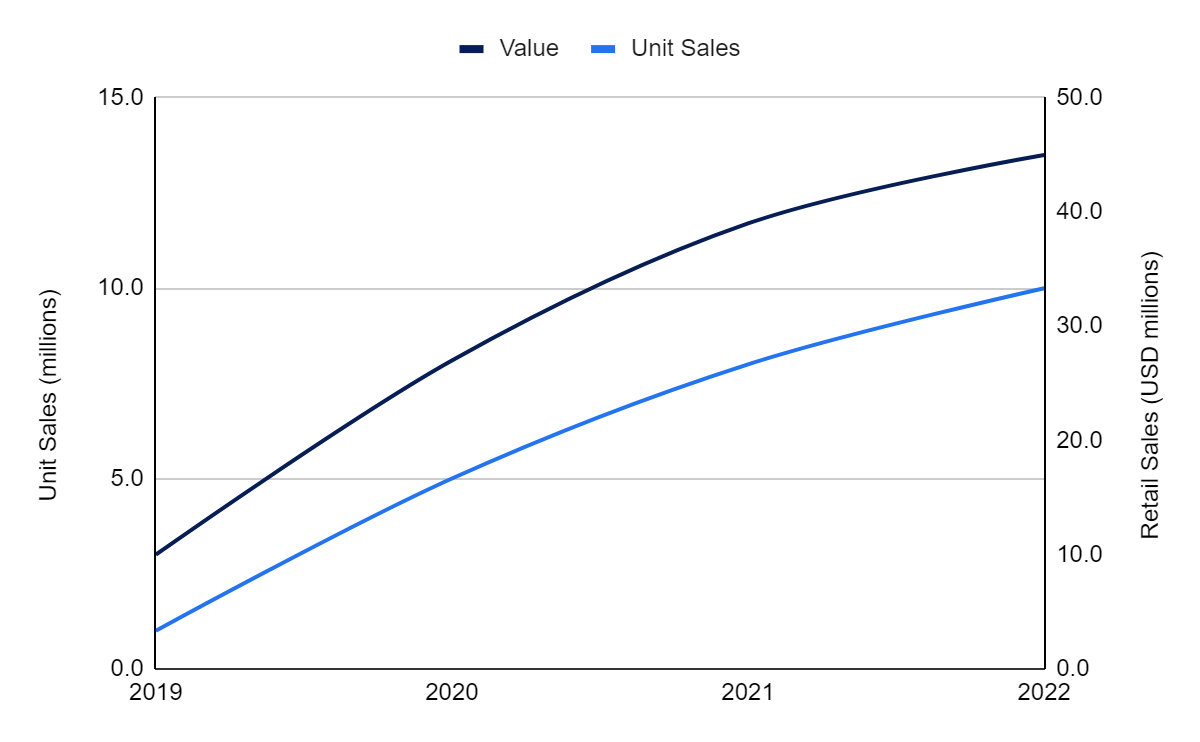

Retail sales of plant-based eggs in the US amounted to USD 45 million in 2022, up 14% YoY and an astounding 348% since 2019. Unit sales exhibited an even more exponential growth pattern, growing 21% YoY in 2022 and 611% since 2019. Plant-based egg unit sales have grown from 1.4 million in 2019 to more than 10 million units in 2022. For comparison, animal-based egg unit sales were roughly 2.3 billion in 2022, decreasing 5% since 2019. The majority of growth in the plant-based eggs category has been rapid and continuous over the past few years as illustrated in Figure 2, with no indication of tapering off or reversing.

Plant-based eggs still hold a minor market share in the total eggs market in the US at 0.5% of value. This share has increased from 0.2% in 2019, growing rapidly albeit from a very small base. Household penetration of plant-based eggs is also very low at 2% in 2022. The low household penetration and low market share of plant-based eggs signals significant room for growth for the category.

The repeat purchase rate among plant-based egg consumers increased 5% in 2022 to 45%, and is up from 20% in 2019. Thus, consumers who purchase plant based eggs more than once a year more than doubled from 2019 to 2022. Thus, the adoption and repeat purchase of plant-based eggs is rapidly increasing in the US as evidenced by the high growth rate in both volume and value.

Figure 2. US plant-based eggs retail sales from 2019 to 2022

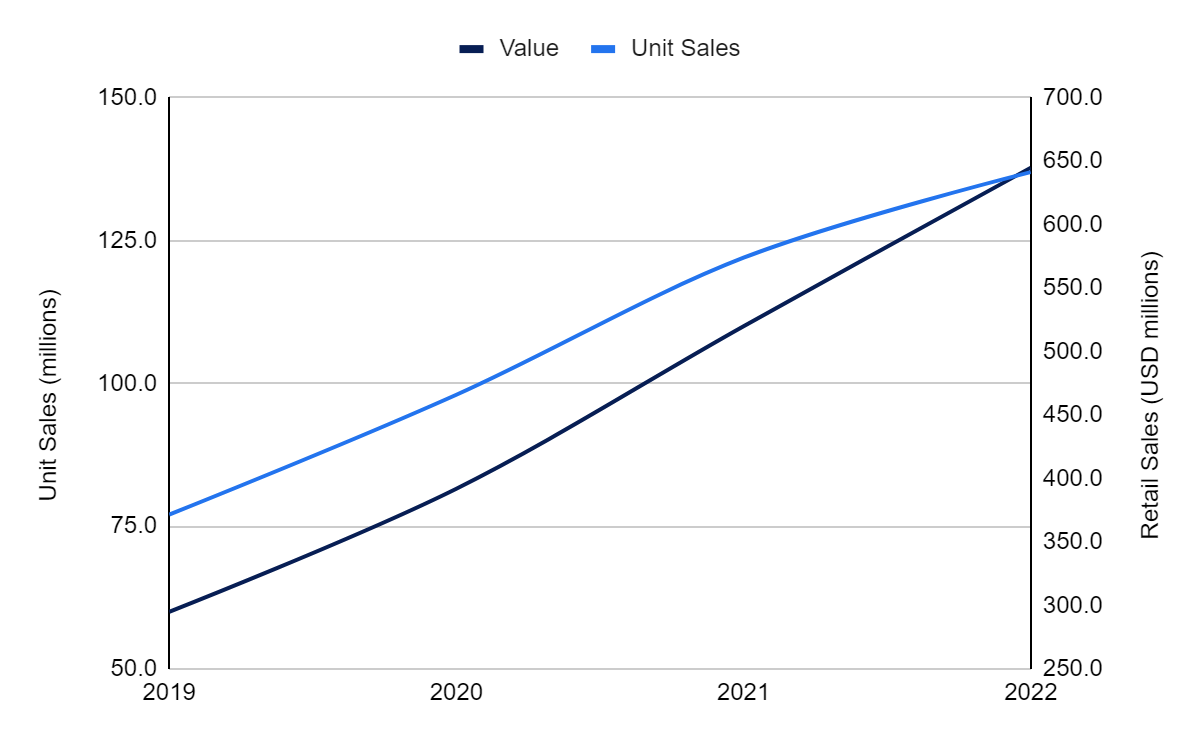

Plant-based creamer is the third largest plant-based food category in the US at USD 645 million in retail sales in 2022, up 24% YoY and 119% since 2019, making it the second fastest growing category in recent years. However, this category lags far behind the two largest categories, plant-based milk and meat, in terms of retail sales value. Unit sales also grew significantly, albeit at a slower pace, rising 12% in 2022 and 77% since 2019.

Plant-based creamer’s market share of the total creamer market in the US has increased to 12% of dollar sales in 2022, up from 7% in 2019 and slightly up from 11% in 2021. Plant-based creamer’s 3-year value growth since 2019 is four times higher than that of animal-based creamer at 25%, albeit from a much smaller base. The 3-year unit sales growth of plant-based creamer of 77% is also significantly higher compared to the 5% for animal-based creamer.

The growth of plant-based creamer in the US market may have benefitted from product and ingredient similarities to plant-based milk, which is the most developed plant-based food category that most consumers have the greatest familiarity with.

Figure 3. US plant-based creamer retail sales from 2019 to 2022

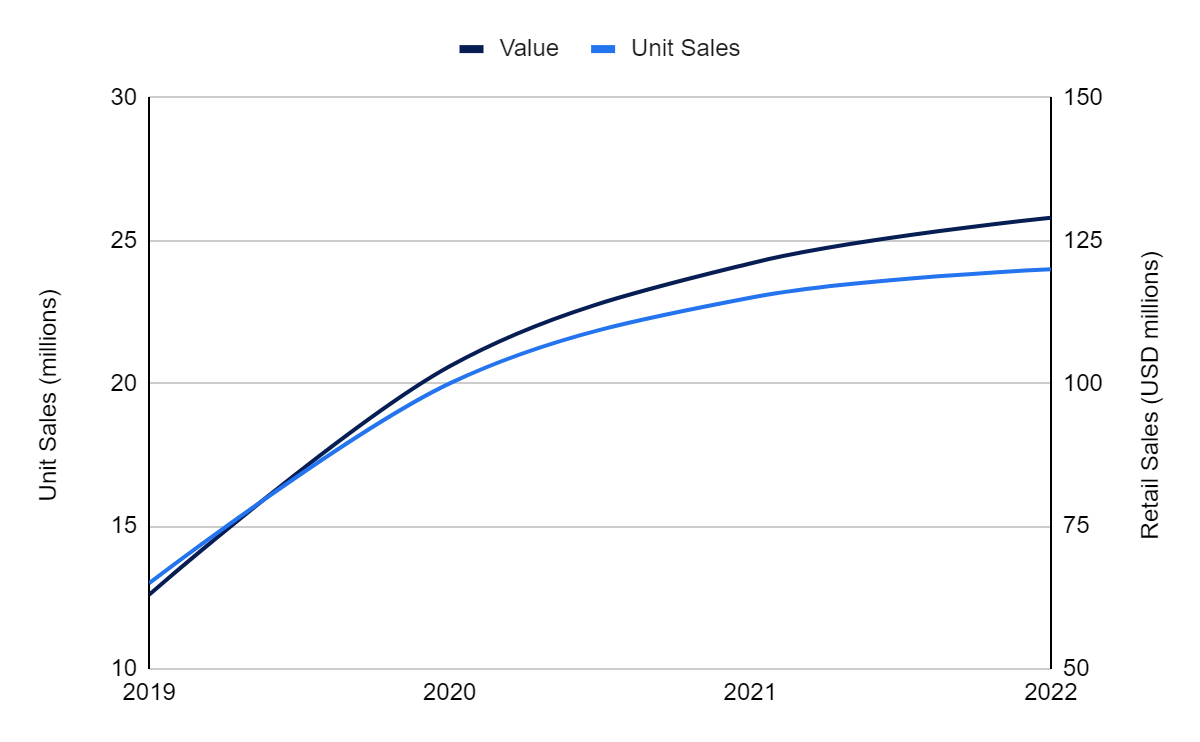

The plant-based cream cheese, sour cream, and spreads market grew 104% in value terms between 2019 and 2022, with only 7% of that growth occurring in 2022. This category exhibited the third fastest growth rate between 2019 and 2022 of all plant-based food categories in the US market. Unit sales experienced a similar but more subdued growth of 86% since 2019 with only 2% of that growth concentrated in 2022. As evidenced in Figure 4, the majority of this growth occurred in 2020, after which growth started tapering off in 2021 and even more in 2022.

Figure 4. US plant-based spreads retail sales from 2019 to 2022

The plant-based food industry in the US experienced significant growth until 2020 when the COVID-19 pandemic hit. The fallout from the COVID-19 pandemic and the resultant economic difficulties in the years to follow resulted in subdued growth in the plant-based food industry, not just in the US, but worldwide. Plant-based food options have also become increasingly expensive in recent years due to high levels of inflation, as evidenced by the 44% growth in value of the plant-based industry in the US between 2019 and 2022, coinciding with only 23% growth in unit sales. This suggests that a large portion of the growth in value terms is driven by higher prices and not by increased sales.

Despite the recent slowdown in growth in the US plant-based industry, Bloomberg Intelligence predicts that the North American plant-based protein market will grow to USD 40 billion by 2030. Taking into account an economic recovery in the coming years, Tridge predicts that the plant-based meat industry in the US will grow at least at 10-15% per year until 2030 to around USD 20 billion. This is based on the large scope for growth in most plant-based food categories, the increased health and environmental consciousness among consumers, as well as technological breakthroughs expected to increase the quality, taste and texture of products as well as reduce the cost of production and ultimately retail costs.

For a detailed analysis of the US plant-based alternative industry, read the US Plant-based Market: Analysis And Opportunities report on Tridge's website.

Read more relevant content

Recommended suppliers for you

What to read next