OPINIO

Original content

The food and beverage industry is shaped by inflationary pressures, shifting consumer preferences, and the need for sustainable growth. Companies increasingly focus on strategies that balance cost efficiency with investments in innovation, marketing, and digital transformation to stay competitive in a challenging market.

One notable trend is the growing emphasis on demand generation through increased marketing investments. Across the industry, companies recognize the importance of brand visibility and consumer engagement in driving topline growth. For example, Nestlé recently announced plans to increase its marketing and advertising spend to 9% of total sales by 2025, up from 7.7% in 2023. This shift reflects a broader industry pivot toward reinvigorating core brands and regaining market share after a period of cautious spending during the pandemic. Nestlé's focus on flagship brands like Nescafé and Maggi highlights how companies are doubling down on their most substantial assets to drive growth.

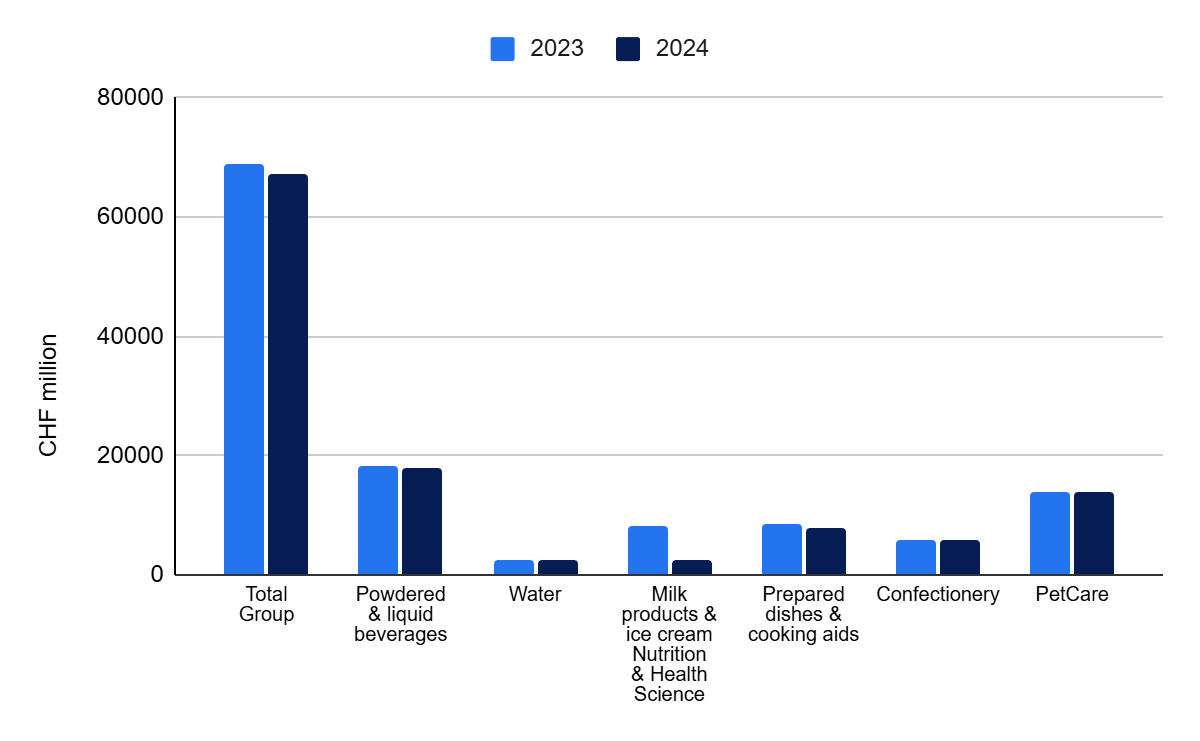

Figure 1: Nestlé Nine-Month Sales Overview by Product 2023 vs 2024

Source: Nestlé

At the same time, cost-saving initiatives are becoming a critical enabler for reinvestment in growth platforms. Many companies are implementing structural cost reductions to fund innovation and marketing efforts. Nestlé, for instance, has outlined a USD 2.84 billion cost-saving plan to be achieved by 2027, targeting procurement, structural costs, and commercial investments. This dual focus on cost discipline and growth investment mirrors a broader industry trend as companies seek to maintain profitability while battling inflationary headwinds.

Unilever is also taking significant steps to accelerate cost cuts, particularly given the upcoming detachment of the ice cream segment. It reiterated its EUR 800 million savings and EUR 300 million in material cost savings.

Another key trend is the optimization of product portfolios to focus on high-growth categories. In the case of Nestlé, the company is prioritizing segments like coffee and pet care, which are expected to grow faster than the broader food and beverage market. This aligns with a wider industry movement toward concentrating resources on categories with strong consumer demand and higher margins.

However, the industry is also struggling to balance pricing strategies amid rising input costs. Elevated prices for commodities like cocoa and coffee have pressured companies to manage consumer affordability while protecting margins. Nestlé's recent acknowledgment of the impact of price increases on sales growth reflects a broader industry concern about maintaining consumer loyalty in an inflationary environment.

In addition to these financial and operational strategies, digital transformation is emerging as a cornerstone of growth for many companies. Data and artificial intelligence are becoming increasingly common to create connected, real-time enterprises. Nestlé's decision to accelerate its digital transformation efforts is part of a larger trend in the industry, as companies seek to enhance operational agility and improve decision-making through technology.

On the other hand, Unilever's growth action plan is producing results, and it has extended its strategy to 2030 while underlining that it is still in its early days. Unilever has focused its resources on its 30' power brands', which account for 75% of sales, but it will now target its top 24 geographies, which account for 85% of total sales. This new market segmentation aims to provide further focus and impact.

In Q3 24, Unilever achieved its highest volume growth in Europe in a decade, and its United States (US) business has been altered by the increased weight of its rapidly rising Prestige cosmetics and health arm. It anticipates its global market share performance to improve in 2025. Management was also notably optimistic about India, which it sees as Unilever's single most significant near-term opportunity, and stated that it will do whatever it takes to defend and strengthen its business there.

Figure 2: Unilever 30 Power Brands

Source: Unilever

Finally, portfolio restructuring and strategic carve-outs are gaining traction as companies look to unlock value and focus on core competencies. Nestlé's plan to establish its water and premium beverages businesses as a standalone global unit by Jan-25 exemplifies this trend. Similar moves by competitors, such as Unilever, suggest that these restructurings could pave the way for spin-offs or external partnerships, enabling companies to streamline operations and focus on growth areas.

While these strategies offer a roadmap for sustainable growth, success will depend on how well companies can navigate short-term challenges, such as inflation and shifting consumer behavior, while staying focused on long-term transformation. For instance, Nestlé's goal of achieving over 4% organic sales growth in the medium term will require careful execution of its marketing, cost-saving, and portfolio optimization initiatives.

As the food and beverage industry evolves, companies that can balance innovation, cost efficiency, and consumer-centric strategies will be best positioned to thrive. Nestlé's recent announcements provide a case study of how one major player addresses these challenges, but the broader industry will be watching closely to see how these strategies play out in practice.

Read more relevant content

Recommended suppliers for you

What to read next