OPINIO

Original content

The United States (US) beef industry has faced significant challenges over the past five years, marked by declining production, rising imports, and elevated beef prices. These difficulties stem largely from the prolonged drought that started in 2020, which led to a substantial reduction in cattle herds. Additionally, the recently concluded US elections are expected to influence the industry, with potential shifts in trade policies likely to impact beef production and trade dynamics.

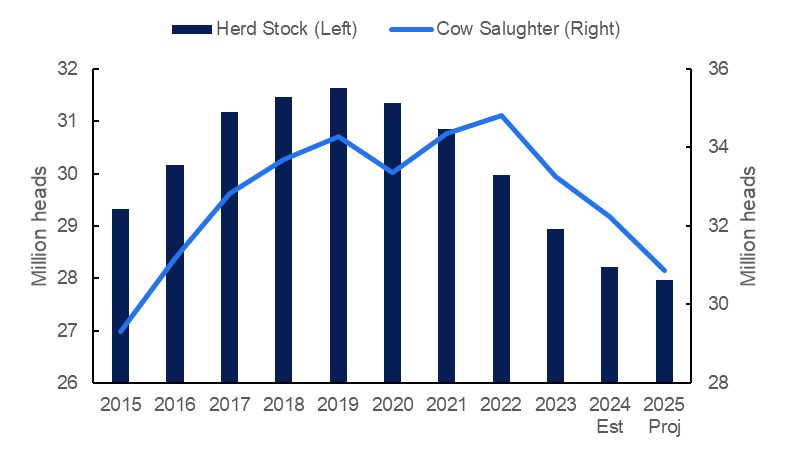

According to the United States Department of Agriculture (USDA), the total US cattle inventory is projected to reach 86 million heads at the start of 2025, reflecting a 1.33% decline from 87.16 million heads in early 2024. This figure also represents an 8.16% decrease compared to 2019, marking the lowest cattle stock levels seen in decades. Similarly, US beef cattle inventory is expected to drop to 27.96 million heads by early 2025, a 0.92% year-on-year (YoY) decline and an 11.63% reduction from 2019 levels.

Figure 1: US Beef Cattle Stock and Slaughter from 2015 to 2025

The bleak outlook for the US cattle industry is largely attributed to the prolonged drought that has persisted since 2020. This created widespread water and forage shortages, particularly in key cattle-producing regions such as Texas, Oklahoma, and Kansas, forcing producers to send their cattle for slaughter. This impact was most pronounced in 2022, with record-high slaughter levels reaching 34.81 million heads. Since then, slaughter numbers have steadily declined and are projected to drop to 30.87 million heads in 2025, marking a 4.25% YoY decrease.

Following relatively stable weather conditions in 2023, the drought condition has reemerged in 2024, with the US Drought Monitor reporting that 62% of cattle were in drought-affected areas at the end of Oct-24, an 8% rise from Jun-24. Ranchers in states like Nebraska and Oklahoma are now dealing with dry pastures and delays in planting grazing crops like wheat. As a result, market experts warn that recovery will be slow, potentially taking several years before herd numbers stabilize and the industry returns to pre-drought levels.

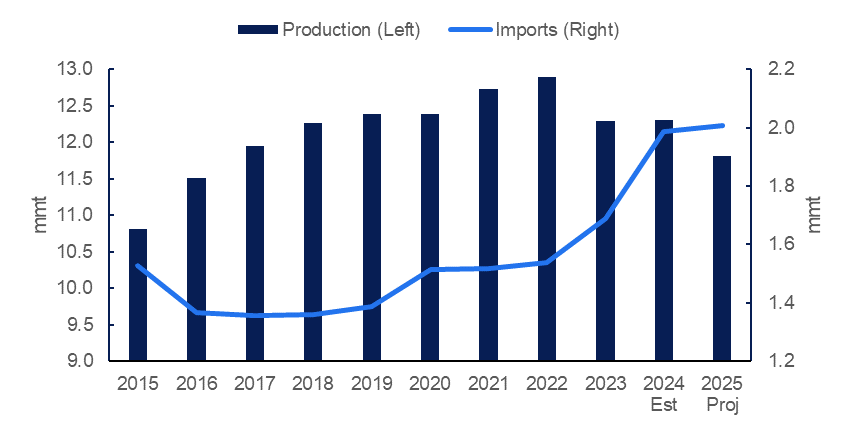

With the ongoing challenges, US beef production is projected to decline to 11.81 million metric tons (mmt) in 2025, representing a 3.98% decrease from the 2024 estimate of 12.3 mmt. Notably, beef production in 2024 has remained relatively stable, with a marginal 0.08% YoY increase, despite lower slaughter numbers. This stability is attributed to higher carcass weights, which have offset the decline in slaughter.

Figure 2: US Beef Production and Imports from 2015 to 2025

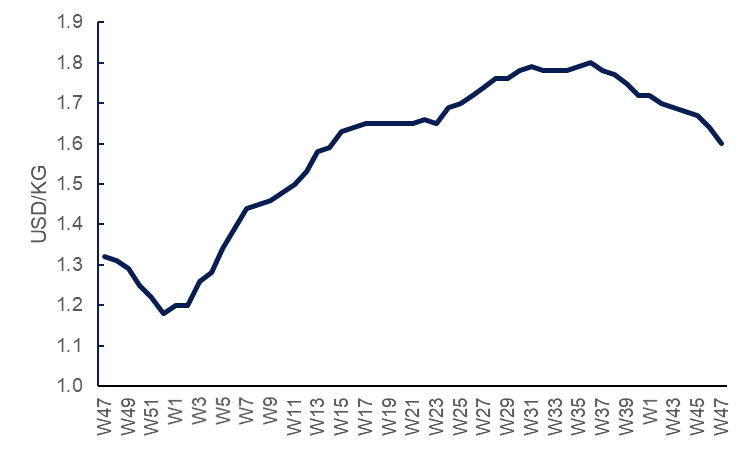

However, domestic beef supply has been tight in 2024, pushing prices to record highs. According to Tridge, US lean beef (92% to 94%) prices reached USD 1.80 per kilogram (kg) in W36, a 23.29% increase compared to the same period in 2023. This surge was driven by limited supply and heightened demand during the summer season, the peak consumption period. As of W47, prices had averaged USD 1.60/kg, marking the 11th consecutive weekly decline as seasonal demand dipped towards winter, a period where beef demand reduces. Despite this drop, prices remained 21.23% higher YoY, underscoring the persistently tight market conditions.

Figure 3: US Wholesale Beef Prices from 2023 to 2024

On the export front, limited exportable supplies have driven US beef export prices higher throughout 2024. As indicated in Tridge’s Nov-24 meat outlook report, the average free-on-board price for fresh, chilled, or frozen beef reached USD 9.74/kg in Oct-24, a slight 0.21% increase from Sep-24's price of USD 9.72/kg, continuing the upward trend observed since Jan-24.

Constrained beef production in the US has driven a surge in imports, with the USDA projecting a record-high purchase volume of 2.01 mmt in 2025, a 1.01% increase from the 2024 estimate of 1.99 mmt. If realized, this would represent a consistent rise from 2017, increasing by a significant 47.79%. This rising import demand has created lucrative opportunities for major beef exporters, particularly Australia. According to Meat and Livestock Australia (MLA), the US became the top destination for Australian beef in Oct-24, with exports rising by a 64% YoY to 45.34 thousand metric tons (mt), marking the second-highest monthly shipment to the country. Brazil has also benefitted, with shipments to the US reaching a historic high of 117.9 thousand mt from Jan-24 to Sep-24, making the US Brazil’s second-largest beef importer.

However, the outcome of the recently concluded US elections could influence global trade policies, with potential implications for the beef sector. The US president-elect's campaign promises to implement protectionist measures, including increasing import tariffs by 10% to 20%, raising concerns about restricted market access. For Brazil, such measures could make it challenging to expand its beef export quota to the US, currently capped at 65 thousand mt and subject to a 26.4% surcharge. If these tariffs are implemented, they would potentially limit beef imports to the US, potentially driving up domestic beef prices due to tighter supply and increased costs. This highlights the broader risks that shifting US trade policies pose to global agricultural markets.

Looking ahead, the US beef industry is expected to face continued price elevation due to a projected decline in production. The anticipated changes in trade policies under the incoming government could further exacerbate this situation, potentially leading to higher prices and even more restricted supply. To counter these challenges, the government should implement policies to shield producers from extreme market volatility. Options such as price stabilization funds or government procurement programs could help manage fluctuations in beef prices, providing producers with much-needed stability. To mitigate risks associated with trade policies, it is essential to diversify beef import sources. Strengthening trade relationships with major beef exporters like Australia, Brazil, and Canada will be key to ensuring a steady, competitive supply of beef, reducing reliance on a single market and improving resilience in the US beef sector.

Read more relevant content

Recommended suppliers for you

What to read next