OPINIO

Original content

To protect local processing plants, Ivorian and Ghanaian authorities may offer cheap loans or limit the volumes of beans that global traders can buy. However, despite these measures, local processors may still face difficulties obtaining sufficient cocoa beans at affordable prices, which is currently occurring. Resultantly, major African cocoa processing plants in the Ivory Coast and Ghana have ceased operations because they cannot afford to purchase beans at elevated spot prices.

For instance, state-controlled Ivorian bean processor Transcao has halted bean purchases due to the bullish trend, and other major state-run plants in the Ivory Coast may follow suit. Global trader Cargill also halted operations for approximately a week in Feb-24 due to difficulties sourcing beans for its major processing plant in the Ivory Coast. Additionally, since the season began in Oct-23, most of the eight plants in Ghana, the world's second-largest cocoa grower, have regularly stopped work for weeks. As a result of the lack of beans, the state-owned Cocoa Processing Company (CPC) is only running at about 20% capacity.

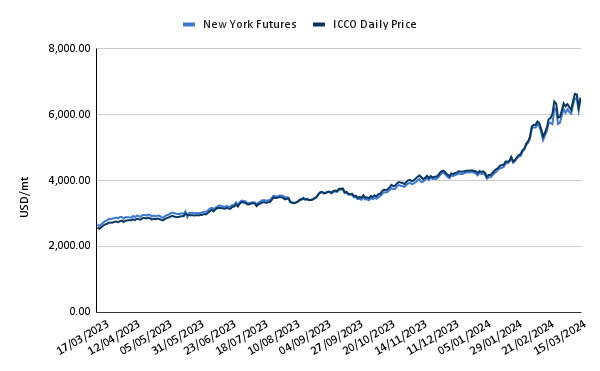

This situation has significant implications for the global cocoa industry, with global cocoa prices increasing further. According to the International Cocoa Organization (ICCO), the ICCO daily price rose to USD 6,523.10 per metric ton (mt) on March 15, rising by 8% compared to USD 6,036.67/mt on March 8, and a significant 157.50% YoY increase from USD 2,533.28/mt. Consequently, cocoa futures have continued their bullish trend, with the London futures rising by 6.1% week-on-week (WoW) to USD 6545.28/mt (GBP 5,162/mt) on March 15 and the New York futures rising by 7.1% WoW to USD 6,468/mt.

Figure 1: ICCO Daily Price and New York Futures (2023 to 2024)

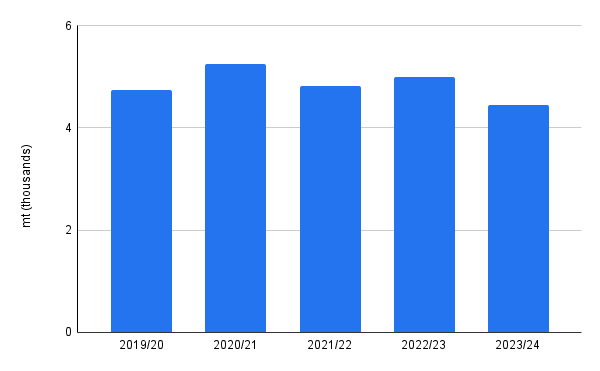

Additionally, the ICCO anticipates a significant decline in global cocoa production, projecting a decrease of 10.9% to 4.45 million metric tons (mmt) in 2023/24. This reduction in production is expected to impact cocoa grindings, a measure of demand, which are forecast to decrease by 4.8% to 4.78 mmt in 2023/24. Processors are struggling to acquire beans, leading them to supply less butter at higher prices to chocolate makers, who subsequently pass on these increased costs to consumers.

Figure 2: Global Cocoa Bean Production (2019/20 to 2023/24)

As a result of the supply-demand mismatch, the market is projected to experience a deficit of 374,000 mt this season, significantly higher than the 74,000 mt deficit recorded last season, according to the ICCO. This deficit will necessitate processors and chocolate firms to rely on cocoa stocks to meet their needs, with the ICCO expecting global cocoa stocks to decline to their lowest levels in 45 years by the end of the season.

Industry insiders like Wateridge of Tropical Research speculate that the cocoa market may experience another deficit the following season (2024/25), given the severity of the bean disease in West Africa. Based on ICCO data, if this happens, there would be a deficit for four years in a row. This would be the first time it has happened since the late 1960s.

Read more relevant content

Recommended suppliers for you

What to read next