OPINIO

Original content

In the United States (US), the crop seed industry has become increasingly concentrated, with fewer, larger firms dominating the market in recent decades. Expanded intellectual property rights and structural changes have driven seed and biotechnology companies to boost research and development (R&D) spending, leading to significant agricultural innovations. Concurrently, seed prices have risen sharply, particularly for GM varieties, reflecting the enhanced value of improved seed varieties and the increased market power of leading seed companies.

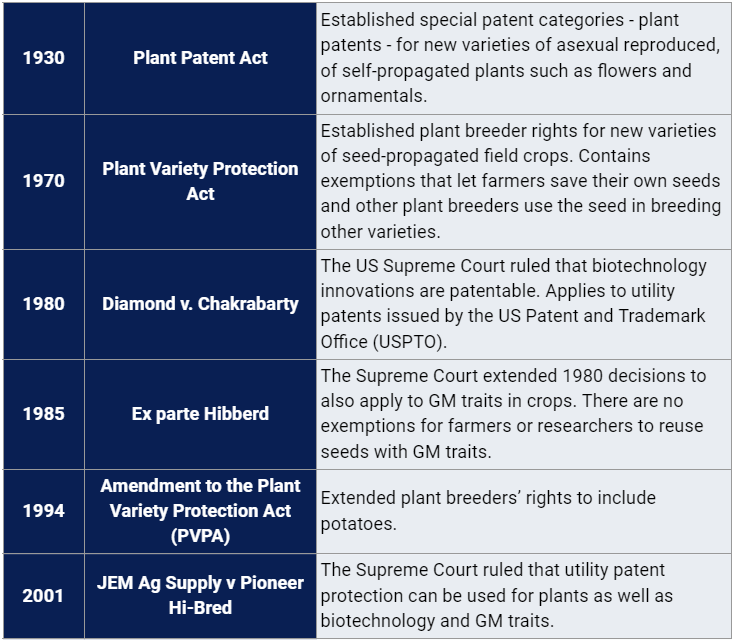

Crop breeding involves altering plant genes to meet changing environmental, nutritional, and market needs. Before 1970, public institutions primarily handled crop breeding, while private seed companies focused on seed multiplication and distribution. Farmers often saved seeds from their harvests, occasionally purchasing new seeds to maintain quality or adopt improved varieties. Some specialized in "bin-run seed," which are seeds collected directly from the field after harvest, cleaned, and treated grain sold for planting. This practice provided little financial incentive for private seed companies to invest in crop R&D, as they transferred the ability to reproduce the technology to farmers without legal restrictions.

Produced by careful pollination of selected two different varieties of plants, hybrid seeds were an exception. They do not reproduce true-to-form, necessitating yearly repurchases from seed companies, thus incentivizing private investment in hybrid crops like corn (maize). However, most other crops continued to be grown using self-pollinated or clonal seeds, which reproduce true-to-form.

The 1970 Plant Variety Protection Act (PVPA) encouraged seed companies to enhance crop varieties by allowing breeders to obtain Plant Variety Protection certificates (PVPCs) for their new varieties. Farmers could still save seeds for personal use but could no longer sell bin-run seeds without a license from the certificate owner, leading to uneven private R&D investment across crops.

Biotechnology advancements allowed specific inheritable traits to be transferred to different crop varieties, creating genetically modified (GM) varieties. Initially, limited intellectual property protection under the PVPA discouraged private investment. However, the 1980 Supreme Court ruling in Diamond v. Chakrabarty and the 1985 Ex parte Hibberd decision allowed biotechnology innovations and GM traits to be patented. These utility patents offered strong protection, preventing farmers from saving patented seeds and companies from using them in breeding without a license.

The 2001 JEM Ag Supply v. Pioneer Hi-Bred ruling further extended patent protection to plants. Consequently, companies now use both patents and PVPCs to safeguard their intellectual property in new crop varieties, including inbred parent lines for hybrid seed production.

Table 1. Timeline of actions establishing intellectual property rights for new plant varieties and traits

The US has three types of intellectual property rights that protect new plant varieties:

1. Plant Variety Protection (PVP) certificates: Created by Congress in 1970 and issued by the USDA, these protect new varieties of seed crops, such as peanuts and potatoes. They include exemptions for breeders to use the varieties in further breeding and for farmers to save seeds for personal use.

2. Utility patents: Issued by the US Patent and Trademark Office (USPTO), these protect new varieties of seed crops and plant traits without exemptions for breeders or farmers. Both utility patents and PVP certificates can be issued for the same crop variety.

3. Plant patents: Established in 1930 by the USPTO, these protect asexual, self-propagating plants, excluding potatoes, and are mainly used for flowers, ornamentals, and some tree crops.

Expanded intellectual property rights incentivized private companies to invest in seed-biotechnology research and development. Companies with promising GM traits often merged with or acquired those possessing seed genetics and marketing assets. Soybeans, corn, and cotton GM varieties were introduced in the US in 1996 and quickly became the dominant choice among farmers. Subsequently, GM varieties were also widely adopted for canola and sugar beets, with increasing use in alfalfa, fruits, and vegetables. By 2020, approximately 55% of US-harvested cropland utilized varieties with at least one GM trait, primarily herbicide tolerance and insect resistance.

Seed markets for peanuts and other crops involve complex interactions among developers, retailers, and suppliers of improved parent lines, seed treatments, biotech traits, and services. Companies often license technologies from each other to produce proprietary seed varieties. For example, Monsanto, an early developer of biotech traits, licensed these traits to other seed companies. Cross-licensing agreements between firms allow them to reduce or avoid paying royalties.

GM traits can be sold separately from seeds and incorporated into multiple crop varieties. These markets are highly concentrated, though specific public information is limited. A single variety may contain multiple GM traits licensed from different companies. Regulatory approval for GM traits must be maintained in each country where the seed is grown and for its intended use (food or feed) in importing countries. The patent holder or licensee usually covers the cost of maintaining these approvals.

Market concentration for crop seeds with popular GM traits (such as canola, sugar beets, and alfalfa) is high, but lower for markets dominated by conventional seed varieties, public-sector varieties, and farmer-saved seeds, such as peanuts and other small grains. The vegetable seed market is diverse, with significant investments from large seed-chemical companies like Bayer and Syngenta, alongside midsized companies with a strong presence in specific vegetable seed markets.

Consolidation in the US seed industry has intensified, with Bayer and Corteva controlling over half of the soybean, corn, and cotton retail seed sales between 2018 and 2020, according to the USDA. The industry, which saw six firms dominating the crop seed and agricultural chemical markets in 2015, is now led by four major companies: Bayer, Corteva, Syngenta, and BASF.

This consolidation traces back to the expansion of intellectual property rights in the 1970s and 1980s, incentivizing private R&D in biotechnology and leading to the first genetically modified crops. Mergers among companies specializing in pesticides, seed treatments, and seed traits have further integrated the industry.

A 2023 USDA study highlighted that the US corn seed market's retail value rose from USD 2.1 billion annually from 2000 to 2003 to USD 7.91 billion from 2018 to 2020, with the top companies controlling 83.9% of the market. In soybeans, the market value increased from USD 1.5 billion to USD 4.74 billion annually, with the top firms holding a 78.1% market share. Cotton seed sales saw a similar trend, with the top four companies controlling 93.5% of the market from 2018 to 2020.

Furthermore, a high market concentration in canola, sugar beet, and alfalfa seeds is due to the popularity of GM traits, while markets for crops like wheat, peanuts, and dry beans, where conventional seeds predominate, remain less concentrated. Vegetable seeds are dominated by private-sector varieties, with significant investments from large seed-chemical companies like Bayer and Syngenta, alongside several midsized companies.

The increased market power of seed companies, driven by patents and PVPCs, has significantly influenced seed cost dynamics. Intellectual property rights grant firms a legal monopoly over their inventions, allowing them to set prices that reflect the R&D investments and commercialization costs. This shift from publicly financed inventions to privately owned technologies has altered the financial landscape of agricultural innovation, with users now bearing the cost through price premiums.

The expanded intellectual property protection and market concentration have enabled seed companies to increase their R&D spending, introduce new high-productivity seed varieties, and charge higher prices for improved seeds. The advent of GM varieties has been a pivotal factor. From 1990 to 2014, R&D spending by the seven largest seed companies: Bayer, Corteva, Syngenta, BASF, Limagrain, KWS, and Rijk Zwaan, surged from under USD 2 billion to over USD 7 billion, paralleling revenue growth from seed and agrochemical sales. These companies allocate approximately 10% of their agricultural revenues to R&D, driving ongoing advancements in crop improvement.

Read more relevant content

Recommended suppliers for you

What to read next