OPINIO

Original content

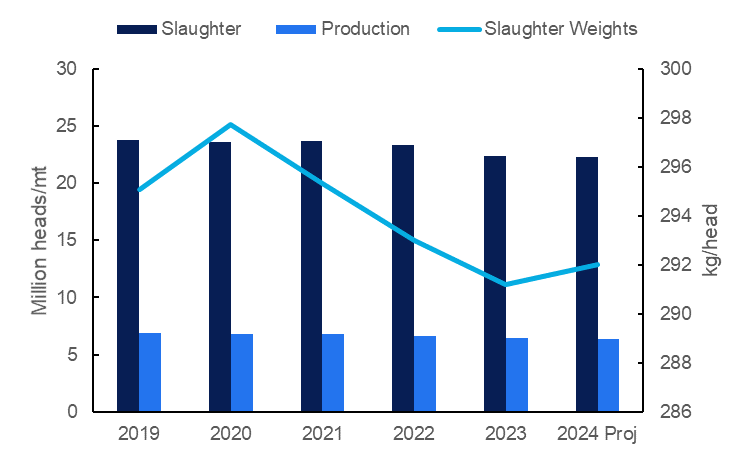

According to the United States Department of Agriculture (USDA), beef production in the European Union (EU) is anticipated to reach 6.4 million metric tons (mmt) in 2024, a 0.47% decrease compared to the 6.43 mmt recorded in 2023. This negative projection is attributed to a declining beef cow herd, which is expected to total 10.39 million heads in 2024, a 0.57% year-on-year (YoY) drop. Moreover, cows entering the herd are estimated to reach 9.56 million heads in 2024, indicating a 4.11% YoY decrease.

Figure 1: EU Beef Production and Slaughter from 2019 to 2024

These declines are attributed to diminished profit margins resulting from high production costs, driven by elevated feed, energy, and labor costs. Additionally, new regulations in the EU mandating financial investments and changes in farm management practices contribute to uncertainty and hinder farmers' ability to invest. Notably, the low production in 2023 was exacerbated by lower slaughter weights, with the European Commission (EC) reporting an average beef slaughter weight of 291.19 kilograms (kg) in 2023, a 0.61% YoY decline. Projections suggest a slight recovery in EU beef slaughter weights in 2024 from the low level recorded in 2023.

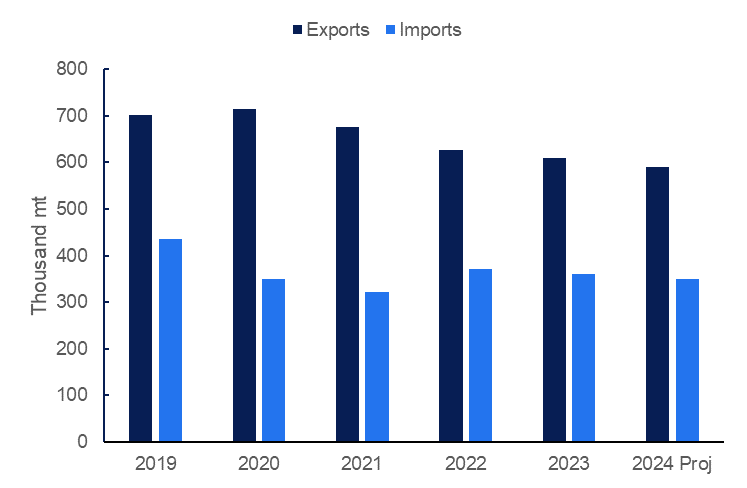

The USDA estimates EU beef exports at 590 thousand metric tons (mt) in 2024, a 3.28% YoY decrease from the 610 thousand mt recorded in 2023. This pessimistic forecast is attributed to limited exportable supplies expected in 2024 due to anticipated low beef production levels. Notably, Ireland, the Netherlands, and Poland are the leading EU member states in beef exports. While Irish and Dutch beef shipments are forecasted to decline in 2024 due to reduced supplies, Polish beef exports are expected to rise. This is owing to comparatively lower production costs in Poland and a decrease in beef availability from other EU producers, stimulating beef exports both within the EU and to non-EU markets. According to the EC, EU beef exports were predominantly directed to the United Kingdom (UK) with 318 thousand mt (+0.47% YoY), and Turkey with 126 thousand mt (+409.3% YoY). The USDA anticipates continued growth in EU beef shipments to Turkey in 2024, supported by robust demand.

Figure 2: EU Beef Trade from 2019 to 2024

The USDA expects EU beef imports to reach 350 thousand mt in 2024, a 7.89% decrease from the Jan-24 estimate of 380 thousand mt and a 2.78% YoY decline. This downward revision is attributed to import tariff quotas that have rendered the EU partially locked, sluggish demand amid challenging economic conditions, and constrained supplies from the UK, a primary supplier. It is worth noting that UK beef shipments to the EU totaled 97 thousand mt in 2023, indicating a significant 13.4% YoY decline due to constrained supplies. Other top sources of EU beef imports included Brazil with 67 thousand mt (+0.27% YoY), Argentina with 49 thousand mt (-22.47% YoY), and Uruguay with 32 thousand mt (-11.6% YoY).

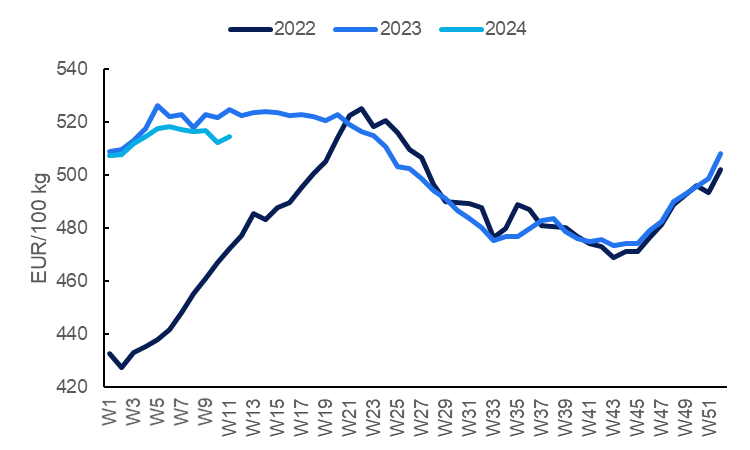

According to EC data, steer beef carcass prices in the EU averaged EUR 514.66/100 kg in W11, a 0.44% week-on-week (WoW) increase but a 1.94% decline compared to the same period in 2023. Steer beef prices have continued rising in 2024, a trend noted since W43, primarily due to limited market supplies resulting from decreased production, albeit remaining below the corresponding levels in 2023. These heightened beef prices are anticipated to dampen product demand within the EU, given the sluggish economic recovery, likely leading consumers to continue shifting towards more affordable protein sources like chicken. Nevertheless, EU beef prices are expected to stay elevated throughout 2024, driven by projected reductions in both production and imports.

Figure 3: EU Steer Beef Price Trend from 2022 to 2024

In conclusion, the EU beef industry is bracing for a challenging landscape in 2024, marked by anticipated reductions in production and imports alongside elevated prices. Moreover, beef exporters in the region are poised to encounter intense competition from global counterparts like Brazil, given the constraints on exportable supplies. Furthermore, sluggish demand is likely to persist within the EU beef sector, driven by high prices prompting consumers to seek more cost-effective alternatives.

Read more relevant content

Recommended suppliers for you

What to read next