OPINIO

Original content

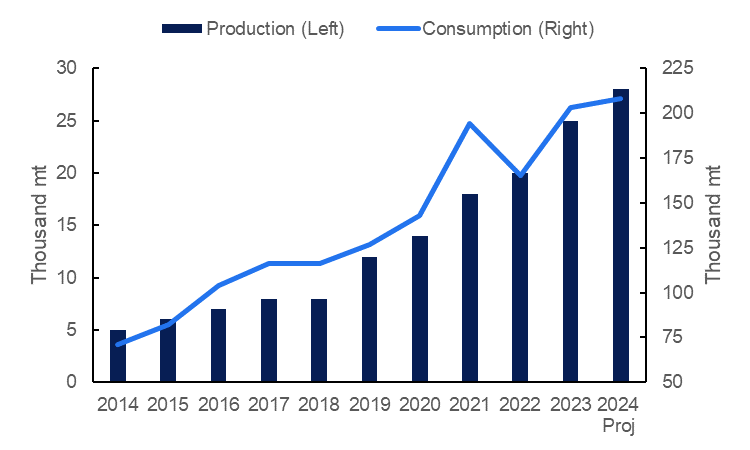

The Chinese cheese market is poised for substantial growth in 2024, offering significant opportunities for domestic and international manufacturers. According to the latest data from the United States Department of Agriculture (USDA), China's domestic cheese consumption is projected to reach 208 thousand metric tons (mt) in 2024. This marks a 2.46% increase from the 2023 figure of 203 thousand mt and a significant 192.96% increase over the past decade.

The consistent growth in cheese consumption can be attributed to several factors, including increased consumer demand driven by the expansion of quick-service restaurants, bakeries, tea shops, and continuous product innovation. Rabobank forecasts that China's cheese demand will continue to grow at a compound annual growth rate (CAGR) of 9.1% from 2023 to 2030, with total demand expected to reach 495 thousand mt by 2030. This optimistic outlook is fueled by rising disposable income among middle-class consumers and the growing popularity of Western-style quick-service restaurant chains.

A rise in domestic production and product imports strongly supports the expected increase in cheese consumption in China. According to the USDA, China's cheese production is forecasted to reach 28 thousand mt in 2024, a 12% year-on-year (YoY) growth and a significant 460% increase over the past decade. This production surge is driven by sustained investments in the country's cheese manufacturing sector. It is worth noting that domestic production primarily focuses on processed cheese products, such as slices, spreads, and cheese sticks, which are particularly popular among younger consumers and within the foodservice industry.

Figure 1: Cheese Production and Consumption in China from 2024 to 2024

Despite this growth, China's domestic cheese production still falls short of meeting the rising demand. The industry is characterized by small-scale operations, dominated by a few large players, with several new entrants seeking to capitalize on the burgeoning market. This gap between production and demand has made significant cheese imports essential for China.

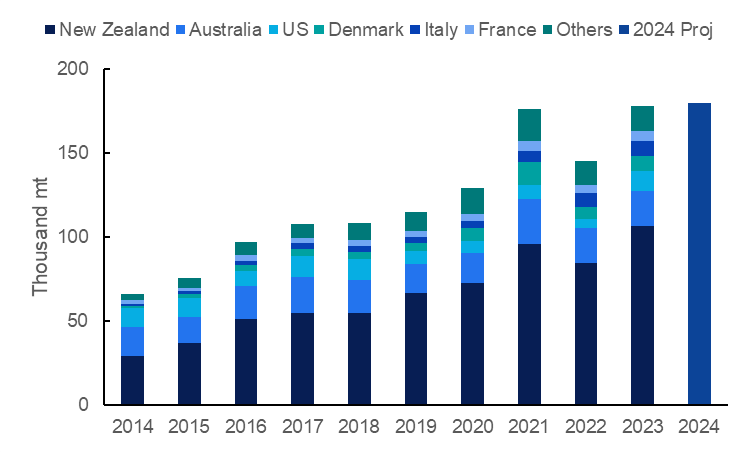

Data from the International Trade Center (ITC) Trade Map shows that China's cheese imports under HS code 0406 (cheese and curd) totaled 178.20 thousand mt in 2023, a 22.49% YoY increase and a substantial 170.12% rise from 2014. This trend highlights the growing appetite for cheese among Chinese consumers, fueled by an expanding middle class, evolving dietary preferences, and the increasing influence of Western cuisine.

Figure 2: China’s Cheese Imports from 2014 to 2024

In 2023, the majority of these imports were sourced from New Zealand, supplying 106.76 thousand mt, a 26.75% YoY increase. Australia was second with 20.92 thousand mt (-1.34% YoY), followed by the United States (US) with 11.56 thousand mt (+125.43% YoY), Denmark with 9.32 thousand mt (+25.22% YoY), Italy with 8.55 thousand mt (+7.21% YoY), and France with 6.19 thousand mt (+20.07% YoY). Notably, Chinese consumers prefer imported cheese due to its perceived higher quality. Looking ahead, the USDA anticipates that China's cheese imports could reach 180 thousand mt in 2024, a modest 1.01% YoY increase, underscoring the continued reliance on imports to satisfy domestic demand.

China's domestic market features a blend of international and domestic brands offering a diverse array of cheese products. Increasing urbanization, Western influences, and evolving consumer preferences drive this variety and availability expansion.

Among the leading international brands is Anchor, owned by Fonterra, a New Zealand-based dairy cooperative. Anchor offers a range of products, including mozzarella, cheddar, and cream cheese, which are highly favored for their quality. Anchor also caters to the foodservice industry, providing bulk packaging options for restaurants and cafes. US’ Kraft is another prominent international brand that offers cheeses tailored to local tastes, such as cheese slices, spreadable cheeses, and cheese snacks. French brand President is also well-known for its premium natural cheeses like Brie, Camembert, and Emmental, appealing to consumers seeking high-quality, authentic cheese varieties.

Figure 3: Anchor’s Cheddar Processed Cheese

Domestic cheese brands in China have experienced rapid growth as they strive to increase their market share by producing products tailored to local tastes and preferences. One prominent brand is Bright Dairy, which is recognized for its affordability and active efforts to promote cheese consumption nationwide. Bright Dairy offers a variety of products, including cheese slices, cheese spreads, and natural cheeses like cheddar and mozzarella. Yili is another prominent player, which produces a range of cheese products designed for convenience and appeal to younger consumers. Yili's offerings include cheese sticks, slices, and spreadable cheeses, catering to the growing demand for easy-to-consume and versatile dairy options.

Figure 4: Yili Cheese Sticks

Beyond the traditional categories of processed and natural cheeses, other segments like cheese snacks, flavored, and fusion cheeses are gaining popularity in China. Consumers are increasingly craving for products like cheese sticks, cheese cubes, and cheese-flavored snacks, which busy urban consumers and children particularly prefer.

Demand for flavored and fusion cheeses is also growing due to their diverse taste profiles, nostalgic appeal, and added nutritional benefits. A notable example of fusion cheese is Haytea's cheese tea, which was launched in 2012 as the first of its kind, combining authentic tea with real dairy cheese. This product presents a unique combination of tea topped with a layer of creamy, savory cheese foam, appealing to younger, trend-conscious consumers. In 2018, Haytea expanded its product line by developing a series of teas that blend real fruit with a whipped cheese layer on top.

As part of its global expansion strategy, Haytea opened a pop-up store in Paris, France, during the 2024 Olympics to introduce its cheese tea brand to the international market. During its operation in Paris, running from July 12, 2024 to August 15, 2024, Haytea made a significant impact, drawing in crowds and attracting over a thousand customers daily. Krasia, a platform giving in-depth insights and analysis on the latest trends and developments in Asia's technology and innovation sectors, indicates that Haytea sold more than a thousand cups of tea on its opening day, generating approximately USD 11,000 in sales. Two Olympic-themed badge products were particularly popular, selling out almost immediately.

Figure 5: Haytea Cheese Tea

In conclusion, urbanization, Western dietary influences, and a shift toward health-conscious choices are set to drive significant growth in China’s cheese market in the coming years. To stay competitive in the market, cheese manufacturers need to invest in research and development to continuously innovate their product offerings, aligning with evolving consumer tastes and preferences while enhancing nutritional value. The rising popularity of cheese in China is closely tied to its availability and accessibility, highlighting the importance of strong marketability. This underscores the need for greater investment in both existing and emerging distribution channels. Companies should focus on strengthening their presence in supermarkets, specialty stores, and e-commerce platforms, as well as leveraging online platforms and social media channels to reach a broader audience.

Read more relevant content

Recommended suppliers for you

What to read next