OPINIO

Original content

China has witnessed an evolving butter market over the past decade, transforming from a niche dairy segment to a stable in urban households and the foodservice industry by 2024. This significant transformation has been spurred by the increasing demand for butter, driven by the rising popularity of Western diets and a growing interest in home baking.

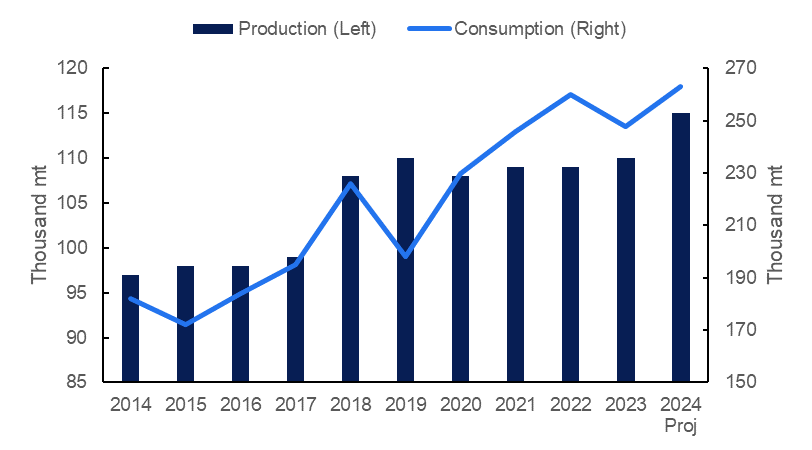

According to the United States Department of Agriculture (USDA), China’s butter consumption is projected to reach 263 thousand metric tons (mt) in 2024. This marks a 6.05% year-on-year (YoY) increase and a substantial 44.51% growth over the past decade. This consumption surge is driven by China's rapid urbanization and the growing popularity of Western-style pastries, bread, and desserts, particularly among younger consumers in metropolitan areas. Notably, Generation Z and millennials, who are more exposed to global culinary trends due to increased internet connectivity, are more willing to experiment with new recipes and products. Additionally, the home baking trend has contributed significantly to the regular use of butter as a key ingredient in households.

Figure 1. China’s Butter Production and Consumption from 2014 to 2024

Due to rising demand, China has seen increased butter production over the past decade. The USDA forecasts that China’s butter production will reach 115 thousand mt in 2024. This reflects a 4.55% YoY increase and an 18.56% rise compared to 2014. This growth is largely driven by increased investment in butter manufacturing. However, despite a current boost in raw milk production, most industries in China prioritize powdered milk production, limiting the expansion of butter output relative to demand. Another challenge facing domestic butter production is quality concerns. According to the USDA, unlike imported cream, domestically produced cream struggles to form the desired foams when whipped, which impacts its use in high-end products. Consequently, China heavily relies on imported products to meet its domestic demand.

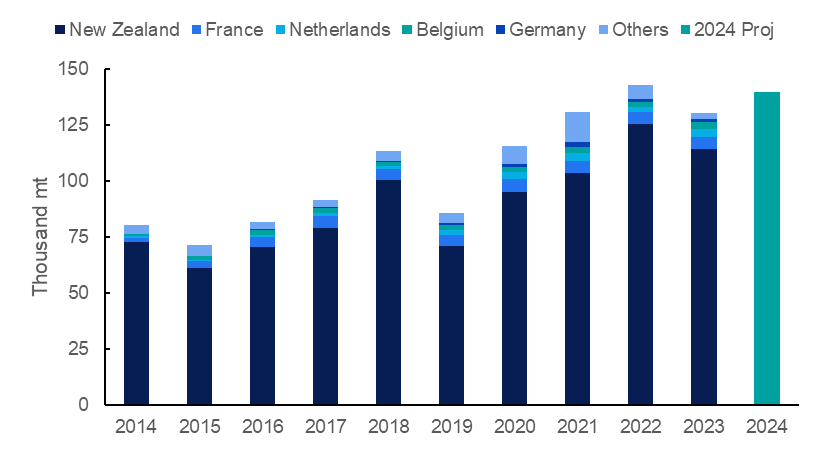

According to International Trade Center (ITC) Trade Map data, China’s butter imports under HS code 0405 (butter and other fats and oils derived from milk; dairy spreads) totaled 130.56 thousand mt in 2023. Despite an 8.65% YoY decline in 2023, Tridge expects China's butter imports to exceed 140 thousand mt in 2024, as the country imported around 70.33 thousand mt in the first half of the year, marking a 9.11% increase compared to the same period in 2023. The 2023 shipments were primarily sourced from New Zealand, which held approximately 87% of the market share with 114.22 thousand mt, despite a 9.00% YoY decrease. Other key import sources included France, with 5.51 thousand mt (+0.27% YoY), the Netherlands with 3.59 thousand mt (+61.11% YoY), Belgium (+33.42% YoY), and Germany with 1.26 thousand mt (+14.00% YoY).

Figure 2. China’s Butter Imports from 2014 to 2023

Due to its reliance on imported butter, China’s butter market often faces challenges such as price fluctuations driven by global dairy market volatility and geopolitical factors like trade tensions and tariffs. For example, Chinese authorities launched an anti-subsidy investigation into European dairy imports on August 21, 2024, following a complaint from the country’s dairy industry on July 29, 2024. This move is seen as retaliatory, coming just a day after the European Commission (EC) announced revised duties on Chinese electric vehicles, citing concerns over artificially low prices that threatened jobs in Europe’s automotive sector. China’s investigation will scrutinize 20 subsidy programs supporting the production of milk, cream, and cheese in eight European Union (EU) countries: Ireland, Austria, Belgium, Italy, Croatia, Finland, Romania, and the Czech Republic. These subsidies include those for dairy storage, allowances for young farmers, and supplementary income and subsidy schemes within the Common Agricultural Policy (CAP).

China’s butter market features a mixture of domestic and international brands, catering to diverse consumer tastes and preferences. Among the domestic brands, Yili, Megniu, and Bright Dairy have notably expanded their product lines to include butter, focusing on aligning with local tastes while offering affordable options. On the international side, brands like New Zealand’s Anchor, France’s Président, and Denmark’s Lurpak command a significant market share. Particularly popular in China, New Zealand’s butter is renowned for its high quality, consistent flavor, and the natural pasture-based farming practices of the country’s dairy industry. Meanwhile, European brands are favored for their rich flavor, smooth texture, and premium image, attracting consumers who seek high-end butter products.

Besides branding, China's butter market is increasingly characterized by the presence of private labels and artisanal offerings. This trend is largely driven by expanding distribution channels, competitive pricing, brand differentiation, and the rising demand for premium and unique products. Notable private labels in China include Walmart’s Great Value, which offers options like Sweet Cream Salted Butter, Tesco’s Tesco Butter, and Costco’s Kirkland Signature, such as Kirkland Salted Sweet Cream Butter. These private labels primarily try to provide good quality products at competitive prices, appealing to budget-conscious consumers.

Figure 3: Kirkland Salted Sweet Cream Butter

The artisanal butter market in China is also growing, particularly in affluent urban areas, driven by consumer demand for high-quality, unique, and locally-produced products. Notable artisanal butter producers include Frenzy Artisanal Butter, Shanghai Creamery, and Gansu Pastures. As consumers increasingly seek out small-batch, handcrafted butters with distinctive flavors, they are more willing to pay a premium for these exclusive offerings.

Another emerging segment in China’s butter market is flavored and specialty butter. These products are infused with ingredients like garlic, herbs, honey, or spices, offering diverse taste profiles, nostalgic appeal, and added nutritional benefits. They particularly resonate with gourmet consumers seeking unique, high-quality options for cooking and spreading.

In conclusion, China’s butter market is set for significant growth in 2024, driven by increasing consumption influenced by Western diets, urbanization, and the home baking trend. This positive outlook presents opportunities for butter manufacturers, who must continue to invest in research and development to align their offerings with evolving consumer tastes and preferences. Manufacturers and retailers should also focus on strategic marketing, including private labeling, innovative packaging, and nutritional profiling. Furthermore, enhancing distribution channels such as supermarkets and specialty stores and leveraging emerging avenues like e-commerce and social media will be crucial for capturing market share.

Read more relevant content

Recommended suppliers for you

What to read next