OPINIO

Original content

When Australia commenced its long-awaited wheat planting season 2024/25, the agricultural industry was confronted with uncertainties that could result in reduced wheat production, more expensive grain prices, and distorted trade conditions. As one of the world’s largest wheat exporters, Australia has to consider environmental, financial, and geopolitical factors.

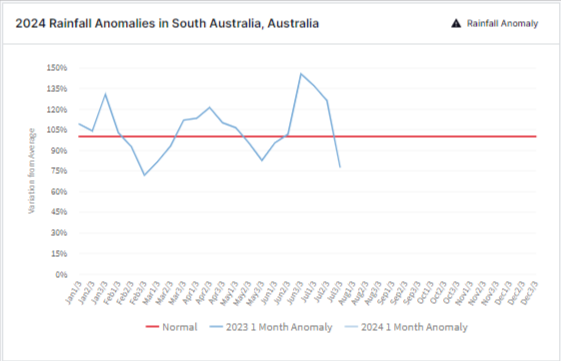

Figure 1: Tridge Weather Data for South Australia

Source: Tridge

The current progress of the planting season is causing worries due to unfavorable weather forecasts and aridity in key wheat growing areas, causing a reduction of moisture in the soil that is needed for the germination of the seeds. There are also reports indicating the intensity of the fall armyworm presence that can severely damage crops and result in yield declines. Moreover, according to the latest United States Department of Agriculture (USDA) Grain and Feed Annual Report, there is an expected drop in wheat production for the upcoming 2024/25 season. Due to dry weather in Western Australia and Southern Australia, the total wheat harvest is predicted to be 25.8 million tons, with yields 3% below the 10-year average.

The world wheat market has been very volatile in recent years because of weather-related conditions in producing countries like Russia and the United States (US). This volatility has been evident during the recent boom of wheat and barley prices in Australia, where most wheat and barley are traded at AUD 412 and 375 per metric ton (mt), a USD 5 to10/mt more than their cereal benchmarks, according to the Australian Government Department of Agriculture, Fisheries and Forestry (ABARES) Weekly commodity price updates.

The increased orders differ significantly from the Chicago Board of Trade (CBOT) wheat futures. These futures reflect a recovery in international wheat prices due to concerns about the 2024 crop and geopolitical tensions.

According to the Australian Bureau of Statistics (ABS), Australia exported 2,573,951 mt of wheat and durum in Mar-24. This marked a 12% month-over-month (MoM) increase from the 2.29 million metric tons (mmt) shipped in February, bringing the total first-half 2023/24 exports to 11,34 mmt. The top three markets for containerized exports were Indonesia (58,828 mt), China (39,034 mt), and Taiwan (25,823 mt).

For wheat specifically, the leading markets in Mar-24 were China (703,355 mt), Indonesia (352,230 mt), and Yemen (343,698 mt), indicating a promising potential for growth in these markets. The Mar-24 export figure represents a notable decline from the 3.8 mmt shipped in Mar-23, primarily due to a smaller harvest in Western Australia. There was a significant decrease in the first half of 2023/24 compared to last year's period, with 11.3 mmt exported this year compared to 16.5 mmt (15.2 million bulk and 1.3 million containerized) from Oct-22 to Mar-23.

Australia’s wheat exports could be affected by the forecasted decrease in wheat production for the forthcoming season, and as a result, trade relationships with other countries might also suffer. On the other hand, the main challenge is the drop in Australia's wheat exports for the 2024/25 season by 13%, projected to be around 17.5 mmt. The nominal value of these exports is anticipated to fall by around 42%, amounting to USD 9.7 billion in 2023/24. The falling imports are directly dependent on the drop in production and export prices, but with the supply above average due to the exportable supply boom of 2022/23, the value remains higher than average.

As winter wheat seeding time approaches, Australia's agriculture faces a number of obstacles that threaten not only this year's production level but also the prices on the markets and the trade balance. The handling of climatic extremes, market fluctuations, and geopolitical hazards remain a highly challenging task; impacting the sustainability of the Australian wheat industry.

Read more relevant content

Recommended suppliers for you

What to read next