OPINIO

Original content

The plant-based food industry in the Asia Pacific (APAC) region is growing rapidly but continues to face several barriers to increasing consumption of plant-based foods. Several organizations have conducted research to uncover the underlying reasons why consumers are not engaging in higher levels of plant-based consumption, including the alt-protein think tank Food Frontier and the Good Food Institute (GFI). The most widely reported barriers to consumption include the high cost of plant-based protein, nutritional value, taste, availability, variety, and processedness.

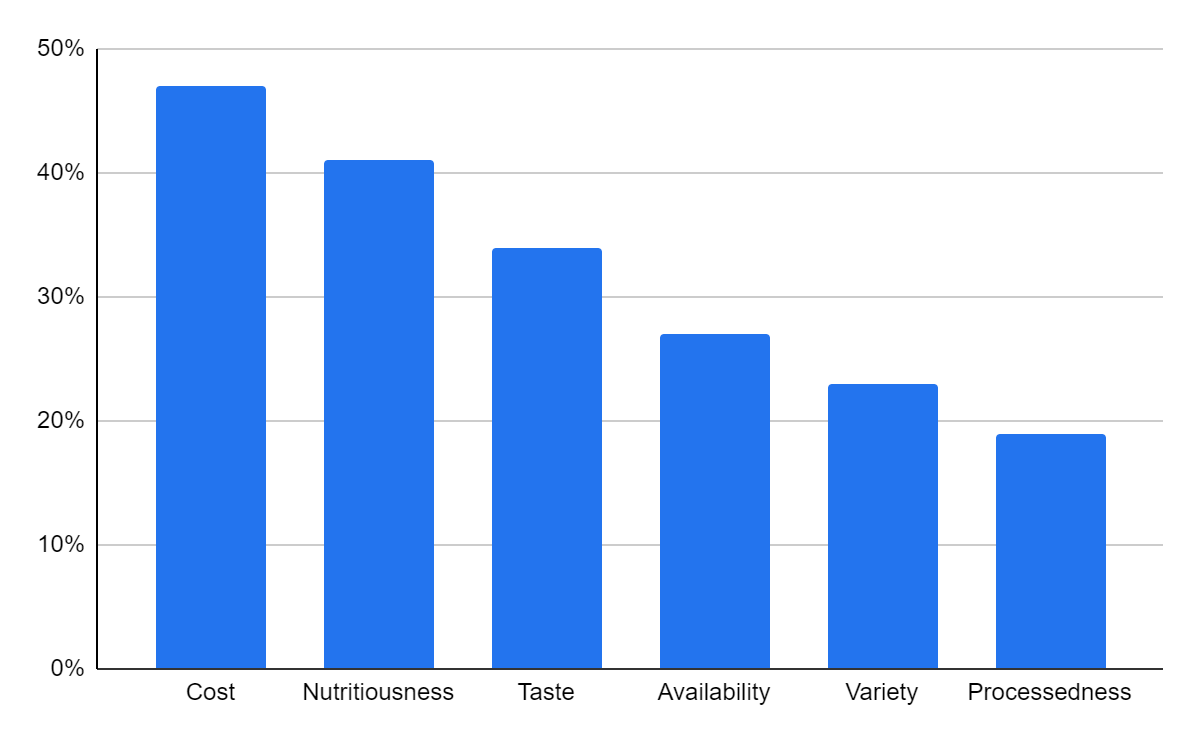

Based on the survey it conducted among 5,971 respondents across Southeast Asia, GFI identified the high cost of plant-based alternatives as the most significant barrier to consuming plant-based food options. 47% of overall respondents cited that they would consume more plant-based meat if it were more affordable. The effect was more pronounced among consumers new to and curious about plant-based foods and less pronounced among established plant-based consumers. It appears that the more engaged consumers are with plant-based products, the less of a role cost plays in their purchase decisions. This finding was echoed by Food Frontier, which found that plant-based consumption is concentrated among high-income households and younger consumers.

On average, plant-based meat products are 35% more expensive than conventional meat in Southeast Asia, with minces, flakes, and meatballs all nearly or more than double the price of conventional meat. Thus, until plant-based foods reach price parity with their animal-based counterparts, the high cost of plant-based food options will continue to deter current and future consumers. Thus, plant-based companies should invest in technology and production processes to reduce the cost of production and ultimately the retail price of plant-based food options.

Figure 1. Barriers to Consumption for Southeast Asian Consumers

The nutritional value of plant-based food is another major barrier to consumption. Nutritiousness was cited as the second largest reason for not eating more of these products in the GFI survey. On average, 41% of respondents cited that they would consume more plant-based meat if it were more nutritious. Similar to cost, the effect was more pronounced among consumers new to and curious about plant-based foods and less pronounced among established plant-based consumers. This suggests that those unfamiliar with or just entering the plant-based meat market are cautious about whether plant-based food options are healthy and provide the required nutrition. Food Frontier uncovered a similar finding indicating that Asian consumers, especially Chinese consumers, have limited knowledge about the nutritional composition and health impact of plant-based food.

To address this issue, plant-based companies operating in Asian countries should focus on health messaging around plant-based foods and highlight their nutritional value. For example, it should be highlighted if a plant-based meat alternative provides the same protein content as its animal-based counterpart. Plant-based companies should also focus on developing healthy and nutritionally complete products that compare with their animal-based counterparts in terms of nutritional value.

Taste is also a major barrier to increased consumption of plant-based food, with the GFI survey finding that 34% of respondents would consume more plant-based meat if it tasted better. Furthermore, 28% of respondents indicated they would consume more plant-based meat if it tasted more like animal-based meat. Similar to the other factors, taste is less important to consumers who are more engaged with plant-based meat than new consumers to the product category. Food Frontier furthermore observed that plant-based food often does not meet the taste expectations of consumers and that the format and texture is often not palatable.

To address this issue, plant-based food companies should focus on developing products that taste better and similar to their animal based counterparts, especially in the case of plant-based meat. Diversification of raw materials and advancements in the production processes of plant-based meat are leading to improvements in the taste and texture of plant-based meat and companies should take advantage of these developments.

The availability of plant-based meat options is also a barrier to consumption for Southeast Asian consumers. GFI found that 27% of Southeast Asian respondents cited that they would consume more plant-based meat if it were more readily available. Contrary to the barriers discussed above, availability is more important for established plant-based consumers while less important to new entrants to the market. It can be assumed that once consumers are established plant-based consumers and develop specific taste preferences, they start looking for products that fit their preferences and needs in the locations where they shop for groceries. Thus, in order to increase consumption among established plant-based consumers, companies should focus on ensuring that their products are available at the primary end purchase destinations that consumers opt to purchase their groceries.

Although only around half as important as the affordability of plant-based products in the GFI survey, variety in choice is still a significant barrier to increased consumption, cited by 23% of respondents. Similar to availability, variety is most important among established plant-based consumers and plays less of a role for new and curious consumers. Choice becomes an important consideration when consumers become established plant-based consumers. Variety will likely become an increasingly important factor as the plant-based industry in the APAC region develops and more consumers become established consumers in this segment. Therefore, companies that operate in the plant-based market in Asian countries should consider increasing the diversity of their offerings to meet the ever-evolving and expanding needs of consumers. One possibility is the introduction of customized and localized food options.

The fact that plant-based meat is too processed and not raw, natural products is another major reason consumers choose not to consume more of these products. 19% of respondents in the GFI study cited that they would consume more plant-based meat if it were less processed, with the effect most pronounced among established consumers in the plant-based market. The nature of how plant-based food items are made, especially plant-based meat, involves heavy processing of raw materials, and consumers do not appreciate this fact. The perception of plant-based food being overly processed was also observed by Food Frontier as a barrier to consumption. Thus, similar to the nutritional aspect of plant-based food, companies and organizations should focus on highlighting that the processed nature of plant-based food does not by nature detract from how healthy or nutritious it is for consumers.

In conclusion, price, nutritional value, and taste are the most important barriers to address for plant-based companies and are the most important among new and curious consumers. These issues are important to address if the market wishes to attract new consumers. On the other hand, availability, variety in choice, and processedness are important factors for established consumers and should be addressed by companies hoping to increase consumption among existing consumers.

Read more relevant content

Recommended suppliers for you

What to read next