Original content

The International Olive Council (IOC) projects global olive oil production to rise by 32% to 3.375 million tons for the 2024/25 season, driven by improved yields in key producing regions. IOC member countries are expected to contribute 95% of the total, with European Union (EU) producers collectively increasing output by 29% to 1.973 million tons. Spain leads this growth with a 51% increase, reaching 1.29 million tons, while Greece anticipates a 43% rise. In contrast, Italy forecasts a significant 32% decline in production.

After severe droughts in Europe caused olive oil prices to soar, Brazilian consumers may see relief by mid-2025. Heavily reliant on imports from Portugal and Spain, Brazil faced supply shortages as European olive production plummeted by 40% in 2022/23 due to extreme weather. This year, European production is set to rise by 29%, with Spain leading the recovery, producing 1.3 million tons, a 50% increase. European prices have already dropped in 2024, but the impact on Brazil will be delayed due to existing high-cost inventory. Experts predict significant price reductions, exceeding 20%, around Easter 2025. While logistics will delay price stabilization, improved European climate conditions are expected to sustain production growth and ease global prices.

With 10 million acres of land suitable for olive cultivation, Pakistan has been actively promoting the crop since 2010, producing 861 tons of table olives annually for domestic consumption. In a webinar organized by the Pakistan Horticulture Development and Export Company (PHDEC), experts discussed modern agricultural practices to boost olive yield and quality, targeting 4,600 tons of olive oil production by 2030 to reduce imports. Key challenges such as sapling shortages, agronomic practices, and limited oil extraction facilities were addressed, with calls for government support and technological advancements to unlock the potential of regions like Potohar, Balochistan, and Khyber-Pakhtunkhwa.

In Turkey’s prominent olive-producing region of Balıkesir, farmers in Burhaniye anxiously await Tariş Olive and Olive Oil Union’s announcement of olive oil prices but it was delayed this year until January. At the general assembly of the Burhaniye Olive and Olive Oil Cooperative, it was highlighted a surplus in production both in Turkey and internationally, particularly in Spain, emphasizing the necessity of exports due to limited domestic consumption. Turkey’s olive oil output is projected at 475,000 tons, while domestic consumption is only 170,000 tons. Akova called for increased government support for producers and urged cooperative members to advocate for higher subsidies.

In 2023, Kazakhstani companies QVM Technology, Ordabasy Group, and Yervira, in collaboration with Georgian company Olive Georgia, signed an agreement to experiment with planting olive tree saplings in the Zhetysu, Turkestan, and Mangistau regions. A total of 6,080 saplings were planted, with 99.7% showing good survival rates. The harvest is expected in five years, with 1,000 hectares (ha) set to be planted by the end of 2025. The project will involve scientific support, including soil and climate analysis from the University of Córdoba. QVM Technology plans to launch an olive oil processing plant by 2030.

_15.22.18.png)

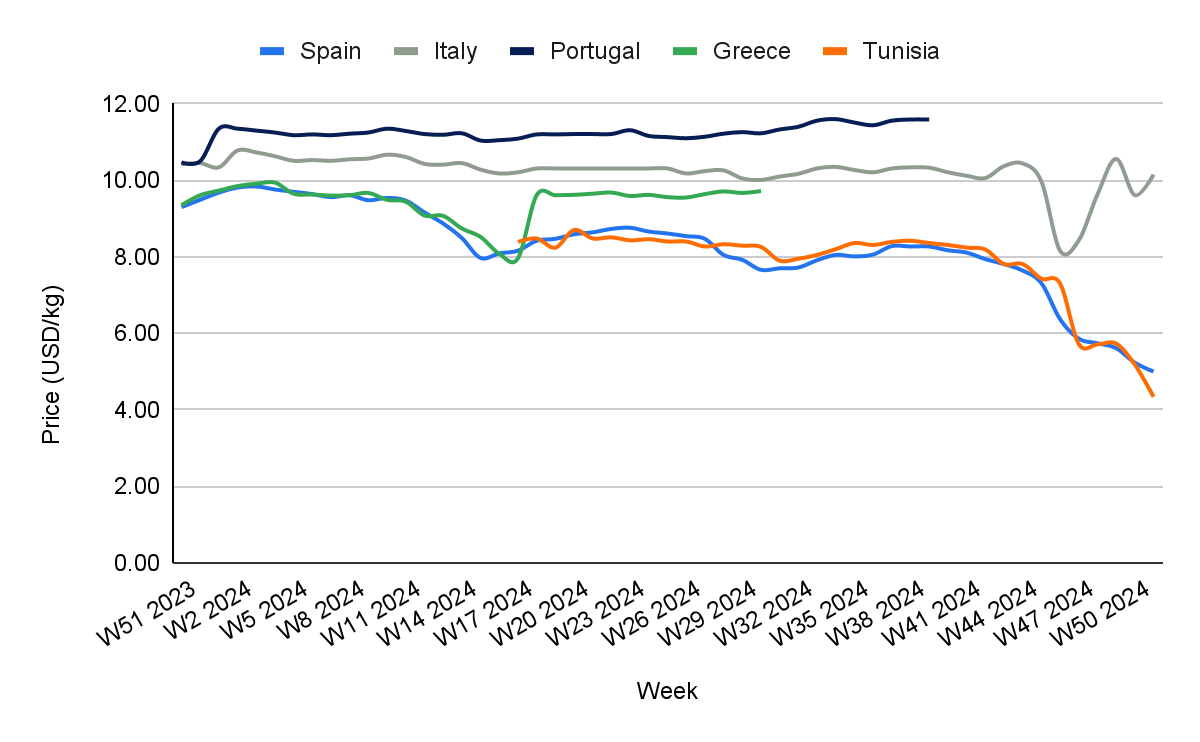

In W51, Spain's olive oil prices experienced a significant drop, falling to USD 5 per kilogram (kg), marking a week-on-week (WoW) decrease of 4.40%, a month-on-month (MoM) decline of 12.89%, and a sharp year-on-year (YoY) reduction of 46.24%. This decline is primarily driven by improved production forecasts and declining domestic consumption. The 2024/25 season's olive oil production is projected to increase by 51% YoY to 1.29 million tons, aided by favorable autumn rainfall, which has boosted yields. However, consumption in Spain is on the decline, falling by 2 to 3% annually, as younger generations shift their preferences due to persistently high prices. This combination of higher supply and weakening demand has led to a sustained downward pressure on prices. Furthermore, cooperative efforts to maintain steady production and meet industry targets have contributed to an oversupply of olive oil, causing prices to drop.

In W51, olive oil prices in Italy reached USD 10.15/kg , marking a 5.62% WoW increase and a 5.40% rise MoM, driven by supply constraints from summer droughts, autumn rains, and labor shortages, which have reduced production. These challenges are compounded by a forecasted 32% decline in Italy's olive oil production for the 2024/25 season, tightening supply further. The holiday season's high demand, particularly for household use and gifting, has also contributed to the price increase. However, compared to the same week last year, prices are 2.59% lower, reflecting a more balanced supply and demand this season despite ongoing challenges.

Olive oil prices in Tunisia dropped to USD 4.34/kg in W51, reflecting a 16.22% decrease WoW and a 23.99% decline MoM. The price drop is largely attributed to the stabilization of global olive oil production, including improved yields in key producing regions, with global production expected to rise by 32% to 3.375 million tons in the 2024/25 season. This increase in supply, including from Tunisia, is expected to continue easing prices, offering financial relief to consumers. The price reductions indicate a more balanced supply-demand dynamic, contrasting with the volatility seen earlier in the year.

In light of global production increases, particularly from Tunisia, Pakistan, and Kazakhstan, stakeholders should invest in olive oil production and processing capabilities in these emerging regions. This will diversify supply sources and reduce dependency on traditional markets like Spain and Italy, ensuring a more resilient supply chain. Additionally, Pakistan’s growing efforts to boost domestic production through improved agricultural practices present opportunities for collaboration and investment.

Given the forecasted 32% increase in global olive oil production for the 2024/25 season, it is crucial to sell out existing stock before prices drop due to the expected rise in supply, especially from major producers like Spain, Italy, and Tunisia. As production stabilizes and supply increases, prices will likely decrease, particularly in the upcoming months. To avoid potential losses, businesses should prioritize selling stock during high-demand periods to capitalize on current prices before the market adjusts. This proactive approach will help secure better margins and mitigate the risk of holding inventory at lower prices.

Sources: Tridge, Cuaderno Agrario, Elaias Karpos, G1, IHA, Son Dakika, Oli Merca, Oli World RU, UKR Agro Consult

Read more relevant content

Recommended suppliers for you

What to read next