OPINIO

Original content

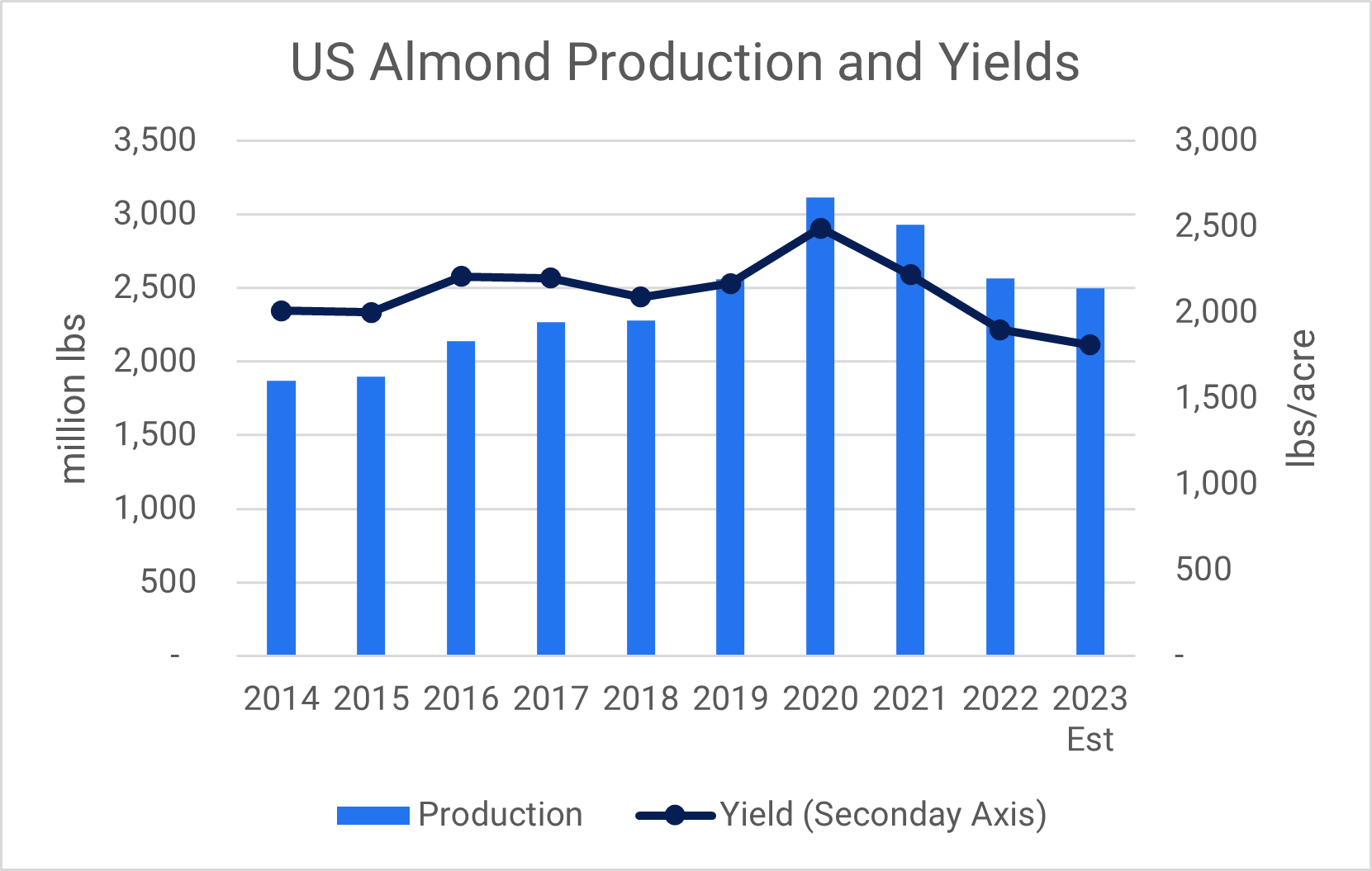

The USDA subjective almond forecast released on May 12 pegs production in 2023 at 2.5 billion lbs. Yields are projected to be the lowest since 2005, after record rainfall, cold and stormy weather impeded the pollination of almonds. While there could be a slight rebalancing of supply and demand, there is still an ample supply of almonds from bumper crops in previous years, and due to the lower demand experienced in the last two years.

Lowest Yields Since 2005

The lower crop estimate doesn’t come as a huge surprise as it results from the unfavorable weather in February. Stormy weather during the almond bloom meant bee flight hours were lower, leading to poor pollination. Industry estimates were all over the place, so the USDA estimate will give some certainty to the market. Yields are forecast to be the lowest in nearly two decades, at only 1,810 lbs/acre, but with the increase in the almond-bearing areas, the drop in production is estimated to be 3% lower than in 2022.

Source: USDA

Estimated carryover from the 2022/23 season

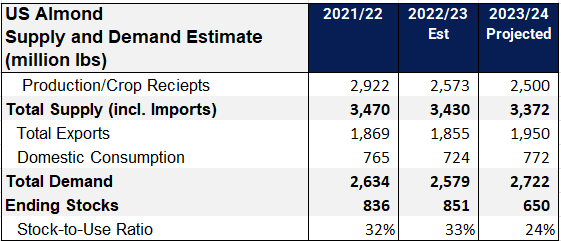

Despite lower production in the 2023 harvest, there will still be enough almonds to meet demand thanks to ample carryover from the 2022/23 season. Ending stocks for the 2022/23 marketing year, as projected on July 31, are 784 million lbs, resulting in a 30% stocks-to-use ratio. Together with the projected production of 2.5 billion lbs, the total supply will still be around 3.3 billion lbs. Although demand will play a significant role in supply-and-demand dynamics in 2023/24, there should be enough almonds to easily meet both domestic and export demand.

Demand and a Return to “Normal” Seasonality

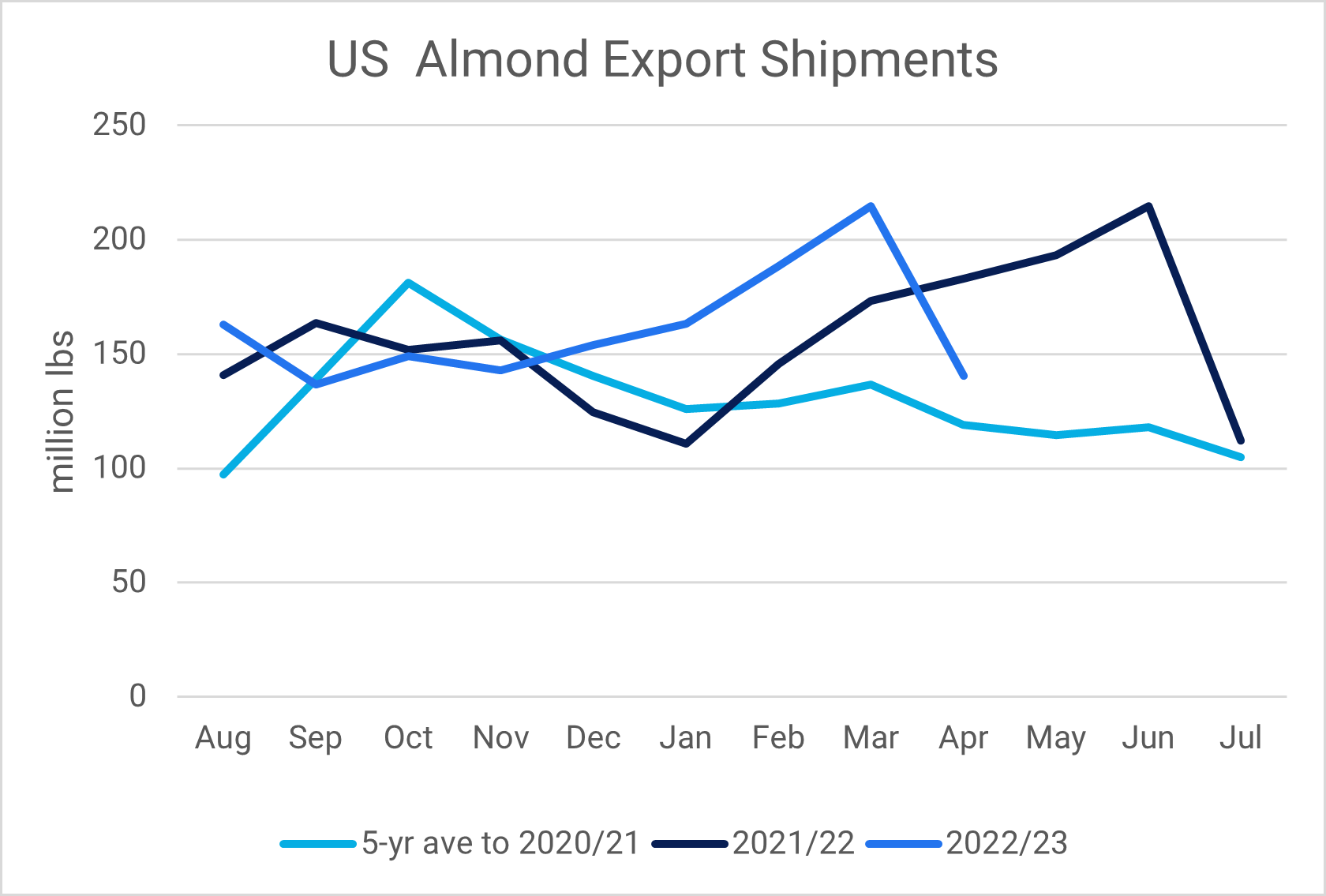

In 2021, disruptions to global supply chains caused a deviation from the usual US almond export season, which normally peaks in October and gradually decreases until the next harvest. However, due to export delays in the 2021/22 marketing year (MY), exports peaked in June. As there was an oversupply of almonds globally, buyers didn't need to plan their purchases far ahead, and the 2022/23 MY followed a similar trend. With supply and demand now balancing out, buyers will be more cautious in planning their purchases, which could mean that the bulk of US exports will be during the harvest season.

Record export shipments in January, February, and March gave an unwarranted impression of a demand recovery, as was proven by the poor exports in April. By the end of April, cumulative export shipments for the 2022/23 MY totaled 1,451 million lbs, up 7% from 2021/22, but down 11% from 2020/21. Total export shipments in 2022/23 could end up being close to 1,855 million lbs.

While it is too early to predict demand for the 2023/24 season, a benchmark based on historical exports is 1,950 billion lbs. Drivers behind demand for 2023/24 include a possible recovery in European almond demand, particularly with a poor production outlook in Spain, and the slightly lower-than-expected crop in Australia.

Source: ABC

Supply and Demand Estimate

Ending stocks for the 2022/23 MY is estimated at 851 million lbs, and with a crop of 2,500 million lbs, the total supply is projected at 3,372 billion lbs. Based on historical data, domestic demand and exports are forecast to be 772 million lbs and 1,950 million lbs respectively. This means that ending stocks at the end of 2023/24 could be 650 million lbs. This is still a healthy inventory with a stock-to-use ratio of 24%.

Source: Tridge, ABC, USDA

Read more relevant content

Recommended suppliers for you

What to read next