OPINIO

Original content

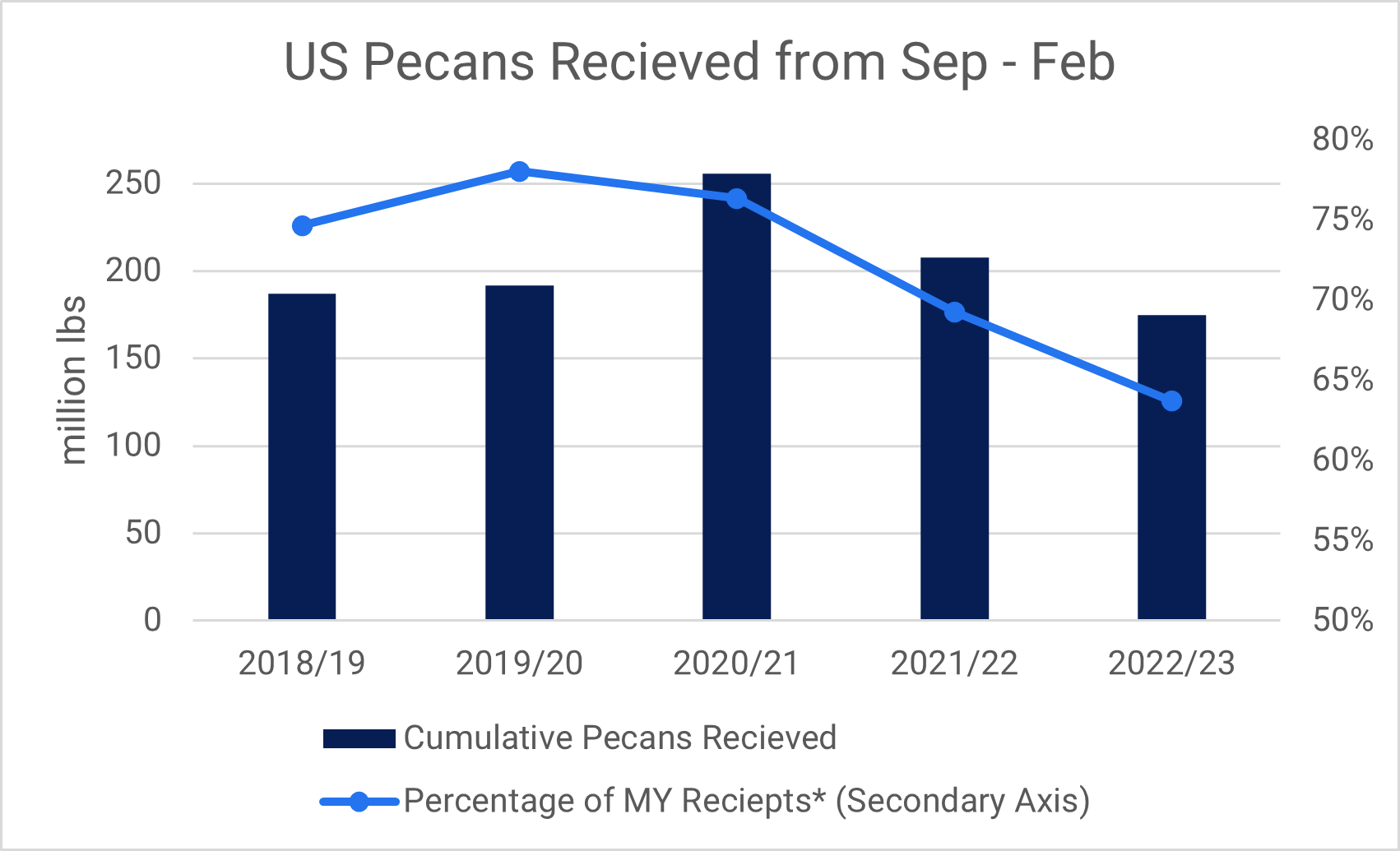

Pecan farmers in the US have opted to hold on to their pecan stocks, in anticipation of better prices. A significant portion of pecan stocks is being held in private storage if total production is compared to deliveries. Pecan production in 2022 was 274.5 million lbs (in-shell) according to the USDA Pecan Production Report released in January. The pecan harvest took place between August and November, and since the estimate is well post-harvest, it could be accepted as accurate. On the other hand, pecans received, as reported by the American Pecan Council have deviated significantly from the norm. Between Sep-Feb, only 174.9 million lbs have been received. This is far lower than the preceding 4 years, for which data is available, which averaged 210.6 million lbs. Given production in 2022 was 4% higher than the 4-year average, it clearly shows a new approach taken by pecan farmers.

*2022/23 as a Percentage of Crop Estimate

Source: APC

A significant volume of pecans is being held by farmers in private cold storage. Since these pecans haven’t passed through handlers, which report pecan receipts to the APC, they haven’t been recorded as received. Many farmers have decided to keep their pecans in storage until prices return to a desirable level. Once, or rather if, pecan prices move higher many of these pecans will be delivered to registered handlers, and a rapid increase in pecan receipts will be reported. Another strategy many farmers have resorted to is to sell pecans directly to consumers, through farmstalls or other direct marketing lines. Pecans can be cracked easily by hand, compared to many other nuts, making them an attractive option for farmers to sell in-shell to end consumers.

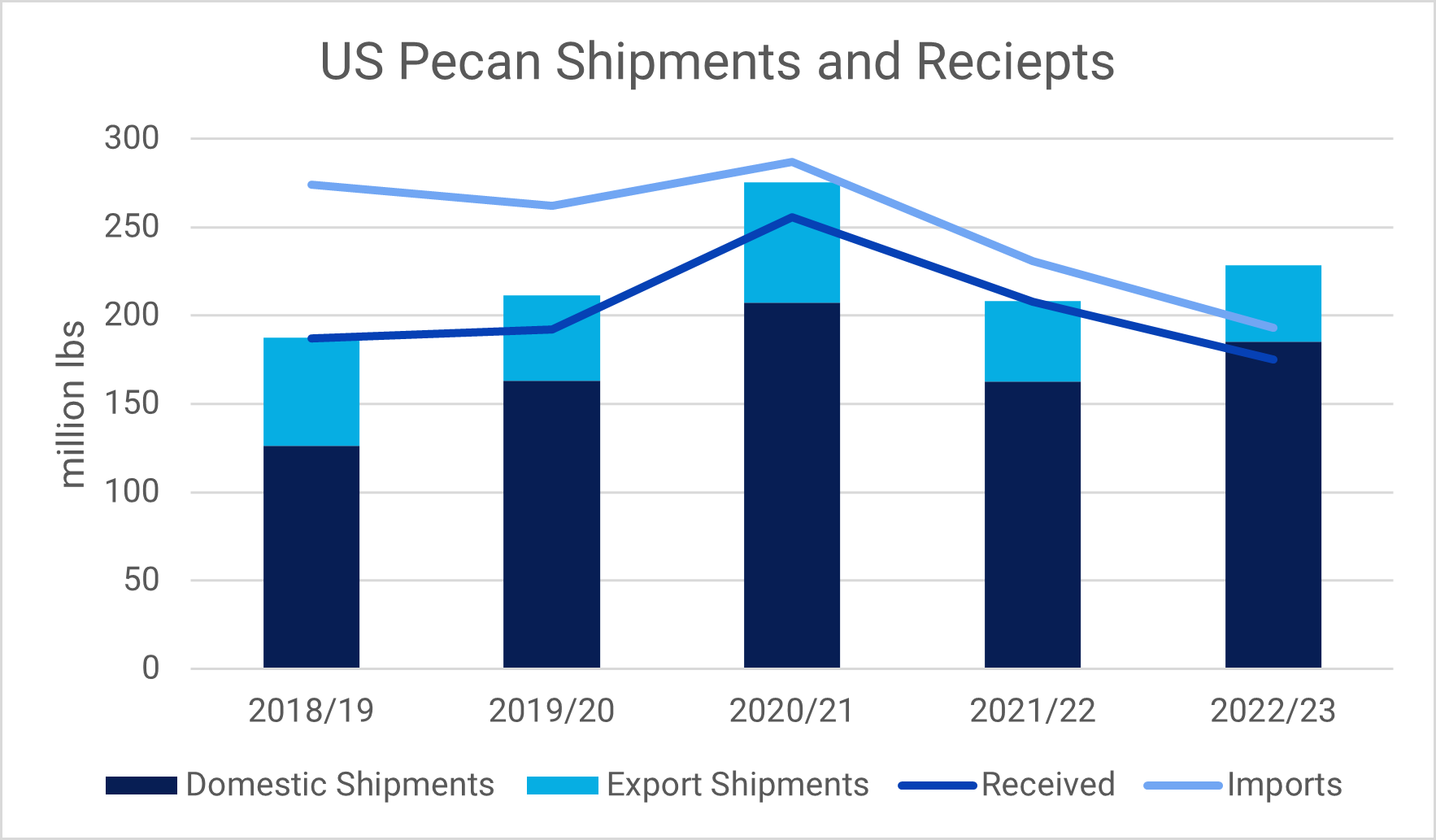

When considering the supply and demand situation in the US in isolation, holding on to pecan stocks makes sense. Domestic demand has been comparatively strong, and domestic shipments between Sep-Feb were 185.1 million lbs (converted to an in-shell basis), which is 8% higher YoY. This more than offset a 4% YoY decrease in cumulative exports to 43.6 million lbs. Most importantly, total shipments, of 228.7 million lbs, are far more than receipts, even when imports of 18 million lbs so far this season, are added to the supply. The balance has taken a big chunk, of 36 million lbs, out of pecan stocks. Pecans stocks at the end of February were 190 million lbs according to the APC’s calculations. More price support is expected after India recently reduced the import tariff on pecans from 100% to 30%, and an increase in export demand is expected.

Source: APC, USDA

However, it should be kept in mind that pecan prices in the US are subject to external price drivers, like global nut supply and demand, and holding on to pecan stocks might not pay dividends in the long term. US imports, of only 18 million lbs, are far below the average of 53 million lbs and imports from neighboring Mexico could increase rapidly to increase supplies. Mexico, the globe’s largest pecan producer, has ample stocks available and the Mexican industry is very closely connected to that of the US. Additionally, demand from Europe, the largest importing region, could continue to be weak amid economic uncertainty. Furthermore, there is a global oversupply of nuts, with large inventories of almonds, walnuts, and pistachios, not only in the US, but globally. While pecans are a more expensive nut in general with a comparative niche market, pecan prices are still subject to the price movements of other nuts, which could hold down pecan prices.

Read more relevant content

Recommended suppliers for you

What to read next