OPINIO

Original content

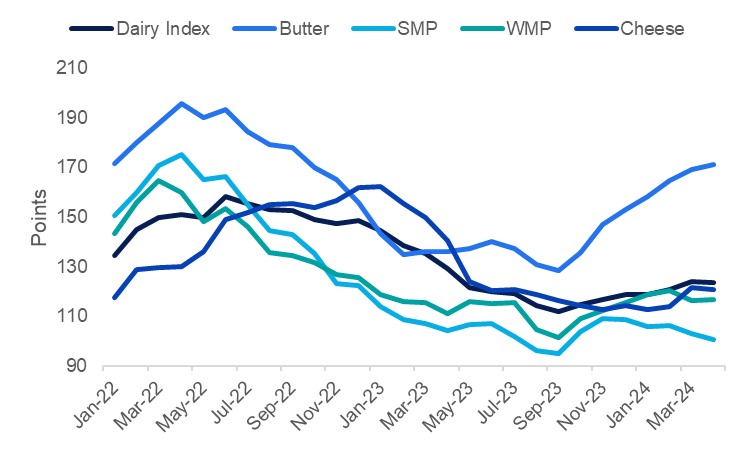

According to the Food and Agriculture Organization (FAO), the global dairy price index averaged 123.73 points in Apr-24, a 0.25% month-on-month (MoM) drop and a 4.24% decline compared to Apr-23. Despite this, the dairy price index has shown a gradual upward trend since Sep-23, after a continuous decline from its record high of 158.16 points in Jun-22. FAO indicates that the recent MoM decline was primarily driven by a 2.17% drop in skim milk powder (SMP) prices due to sluggish import demand amid high exportable availability, particularly in Western Europe, and a 0.59% decrease in cheese prices influenced by the strengthening US dollar.

Figure 1: FAO Dairy Price Index Trend from 2022 to 2024

Conversely, the FAO butter price index registered a 1.17% MoM increase due to steady import demand and marginally tighter butter inventories in Western Europe. Also, the whole milk powder (WMP) index grew by 0.64% MoM, driven by increased demand for medium-term supplies and seasonally declining milk production in Oceania.

The drop in the dairy price index in Apr-24 contradicts earlier projections, which had anticipated a gradual but steady price increase throughout 2024. Rabobank's Q1-24 report indicates that the earlier price rise, noted since the second half of 2023, was driven more by a reaction to previously low prices and a restocking phase rather than a boost in consumer demand across most regions. Rabobank suggests that buyers are now more cautious, anticipating a seasonal peak in Northern Hemisphere milk production. Additionally, the global market faces trade challenges due to China's increasing domestic production, which is expected to reduce dairy product import demand.

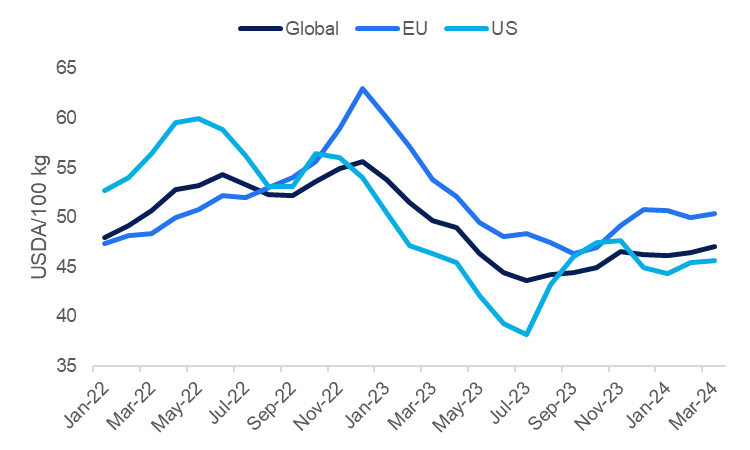

This situation is reflected in the prices of raw milk in top-producing countries like the European Union (EU) and the United States (US). According to Clal.it, an Italian Dairy Economic Consulting firm, global milk prices averaged USD 47 per 100 kilograms (kg) in Mar-24, a 1.21% MoM increase but a 5.45% drop compared to Mar-23. Despite this, prices have remained relatively stable since Nov-23, suggesting a slight recovery in global milk supply amid mixed signals in demand recovery and ongoing pressure on consumers’ purchasing power due to inflation.

Figure 2: Global Raw Milk Price Trend from 2022 to 2024

According to the European Commission (EC), EU milk production amounted to 48.73 thousand metric tons (mt) in Q1-24, a 1.12% drop compared to Q1-23. Despite this, Eurostat reports that raw milk deliveries to processing facilities reached 36.32 thousand mt in the Jan-Mar-24 period, a 1.14% increase over the same period in 2023. Favorable weather conditions in Apr-24 will likely boost EU raw milk production due to improved pasture growth and increased fodder supply.

The United States Department of Agriculture’s (USDA) Dairy Market News reports that Western European milk production is nearing its seasonal peak, with weekly volumes plateauing. Meanwhile, Eastern European milk production continues to rise, with the Baltic States, Czech Republic, Slovakia, Hungary, Romania, and Poland all posting increases in Mar-24 compared to the same period in 2023. This market situation suggests that sufficient milk supply might have led to relatively stable prices. However, the EU dairy industry still faces challenges that could slightly reduce milk production in 2024. These hurdles include long-term declines in farm profitability due to high production costs, environmental constraints, labor shortages, and uncertain weather conditions.

Similarly, the National Agricultural Statistics Service (NASS) data shows that US milk production reached 25.84 thousand mt in Q1-24, a 0.23% increase compared to Q1-23. Dairy Market News also reports that as of the week ending May 17, farmers in the Pacific Northwest and the mountain states of Idaho, Utah, and Colorado saw steady to strengthening production, while milk output in the Midwest and East remained generally steady.

This positive trend in US milk production is attributed to favorable spring weather conditions, contributing to a stable milk supply and relative price stability despite an outbreak of avian influenza in dairy cows in Mar-24. Tridge’s analysis, “Dairy Market Stability Amid H5N1 Bird Flu Concerns,” indicates that consumer behavior and milk prices showed no significant changes following the news of the bird flu outbreak on March 25, 2024. Rabobank also noted no significant market reaction to the outbreak in the US dairy herd since Mar-24.

Looking ahead, global dairy prices are expected to remain relatively stable, supported by optimistic milk production forecasts in the Northern Hemisphere due to favorable weather. However, negative projections for milk production in the Southern Hemisphere, particularly in Australia and New Zealand due to drought and El Niño weather phenomena could complicate the global outlook. As a result, market players are advised to remain cautious in 2024.

Read more relevant content

Recommended suppliers for you

What to read next