OPINIO

Original content

The 2022/23 almond marketing year (MY) is drawing to a close and will wrap up on July 31. Export sales have been decent under the circumstances and have helped to rebalance supply and demand slowly. But domestic consumption remains weak and has not contributed to lowering inventory to a more desired level.

Weak Domestic Demand

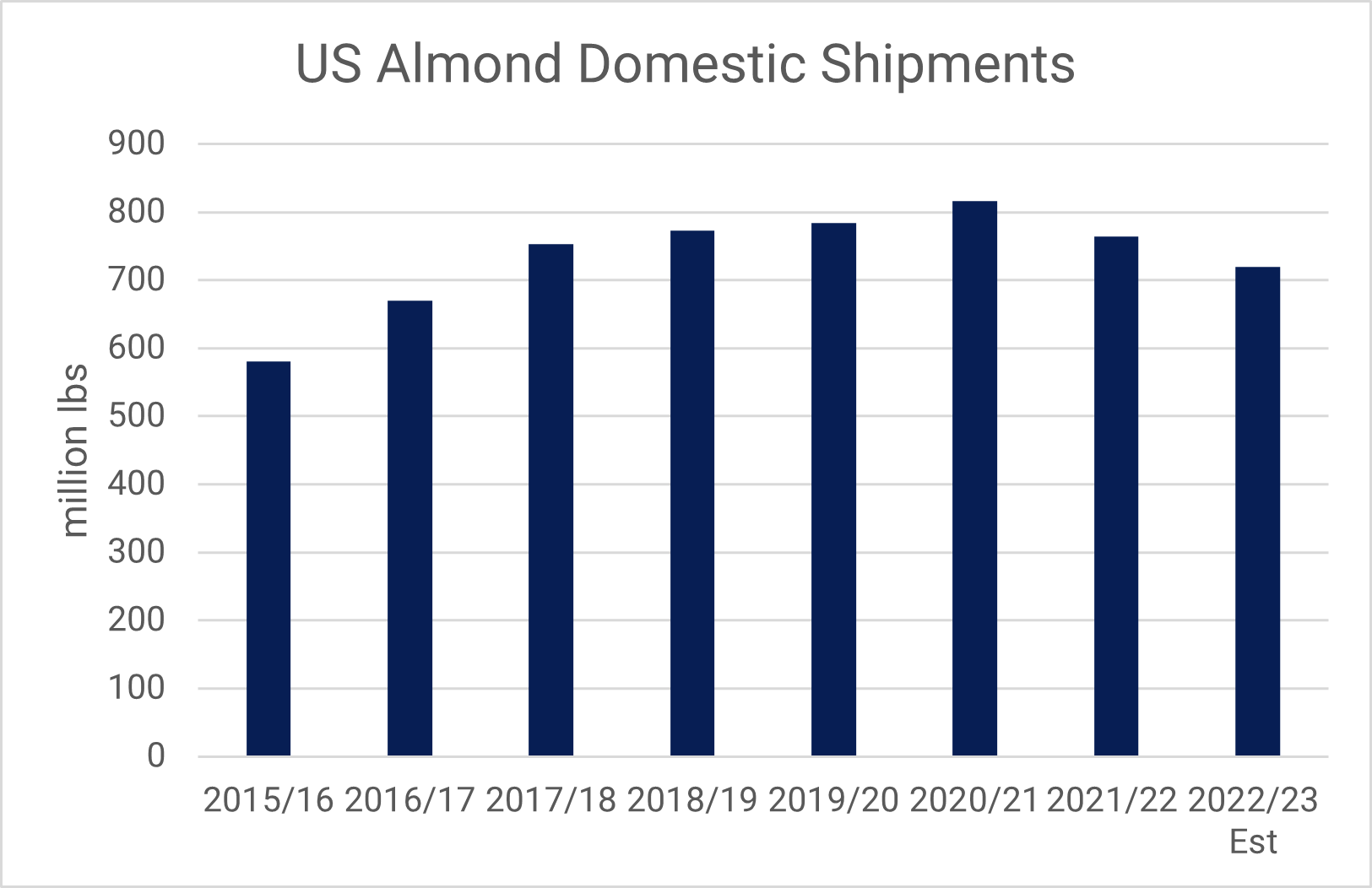

Domestic almond shipments in the United States (US) are estimated to reach a mere 720 million lbs when the 2022/23 MY comes to an end on July 31. This will be the lowest domestic consumption since 2016/17. Domestic consumption has dropped over the last two marketing years as end consumers are still tightening their belts under high inflation and increased living costs. The focus on healthy eating during the Covid-19 pandemic, which led to increased almond consumption in 2020/21, has also faded. Fewer households are willing to spend extra on healthy snacks like nuts and even consumption of almond milk has decreased (see the Tridge Plant-Based Dairy Overview 2023 for more information). Even at lower retail prices, domestic consumption remains subdued. Wholesale prices fell to decade lows by the end of 2022 and have continued decreasing since. However, retail prices have been slow to adjust accordingly. It was only in the second quarter of 2023 that retail prices started to decline, with generic brand almonds currently retailing at approximately ~USD 8.00/30oz, compared to ~USD 9.70/30 oz in Q1-23.

Source: Almond Board of California

Large Carry Over and Oversupply

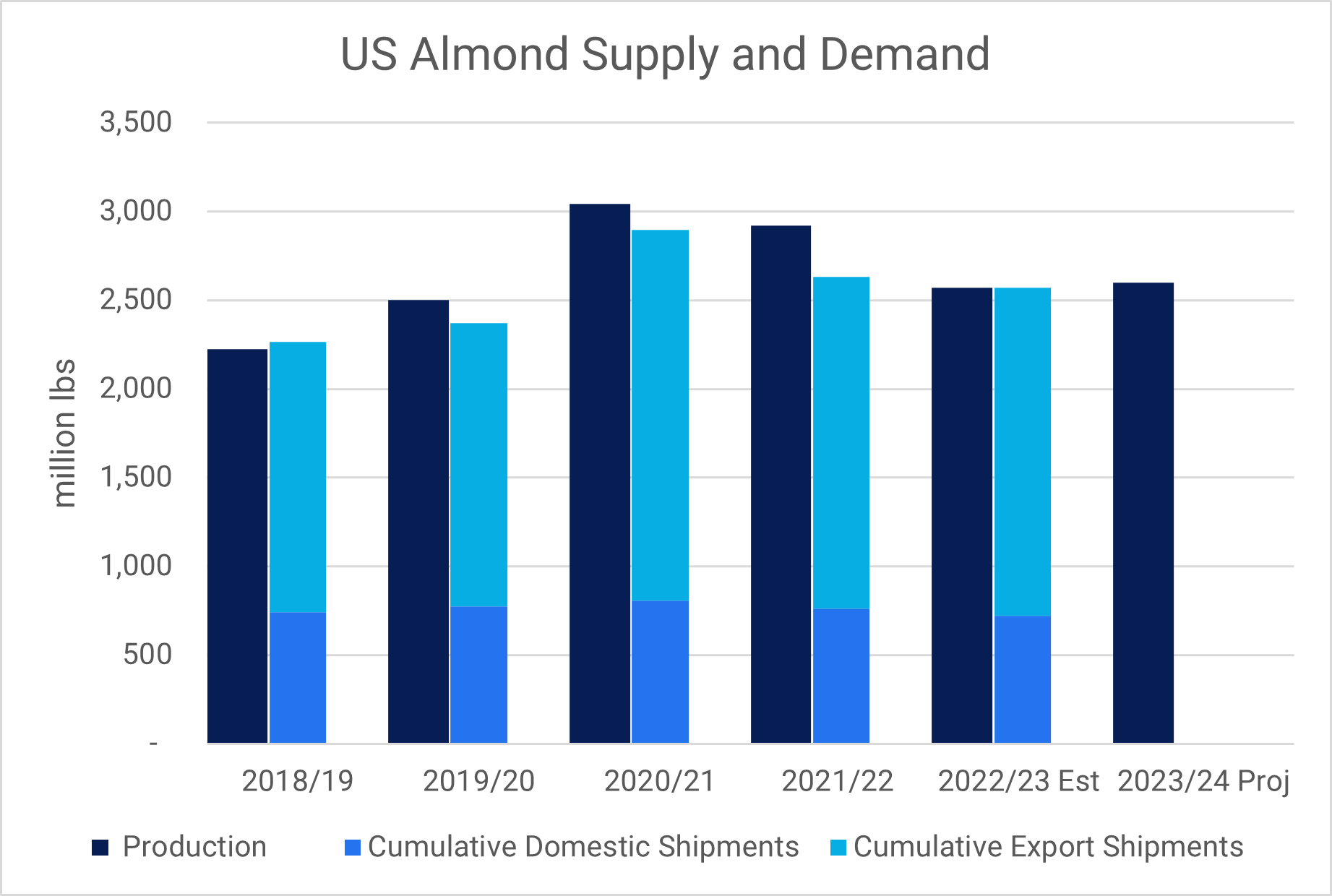

Since the record crop of 3.1 billion lbs harvested in 2020, handlers were forced to carry large inventories. The 2020/21 marketing year was a record year in terms of exports of 2 billion lbs and domestic shipments of 800 million lbs as more consumers paid attention to healthy diets worldwide. Despite the strong demand, at the end of the 2020/21 MY, ending stocks topped 600 million lbs. Since then, production declined, but so did exports and domestic consumption, and the market remains oversupplied. At the end of the 2022/23 season, on July 31, inventories are expected to be as high as 850 million lbs (386 000 mt). To put that into perspective, the inventory held in the US when the 2023 harvest starts is equal to worldwide production from all other countries combined.

Source: USDA, Almond Board of California

Another Bumper Crop on the Way

US almond production has steadily increased YoY and the last five years have all yielded crops higher than 2.5 billion lbs. The United States Department of Agriculture (USDA) Objective Almond Measurement, released on July 12, puts the 2023 crop at 2.6 billion lbs, higher than the Subjective Estimate of 2.5 billion lbs released in May and also higher than market expectations. With another bumper crop to be harvested from August onward, the oversupply of almonds is poised to persist throughout at least the first half of the 2023/24 MY. The absence of substantial recovery in both domestic and export demand exacerbates this. Prices are projected to remain at their already comparatively low levels, with little potential to increase. The average export price of almond kernels in 2023 has been a mere USD 4.28/kg, in contrast to the average of USD 4.84/kg in 2022 and the five-year average of USD 5.61/kg.

Read more relevant content

Recommended suppliers for you

What to read next