OPINIO

Original content

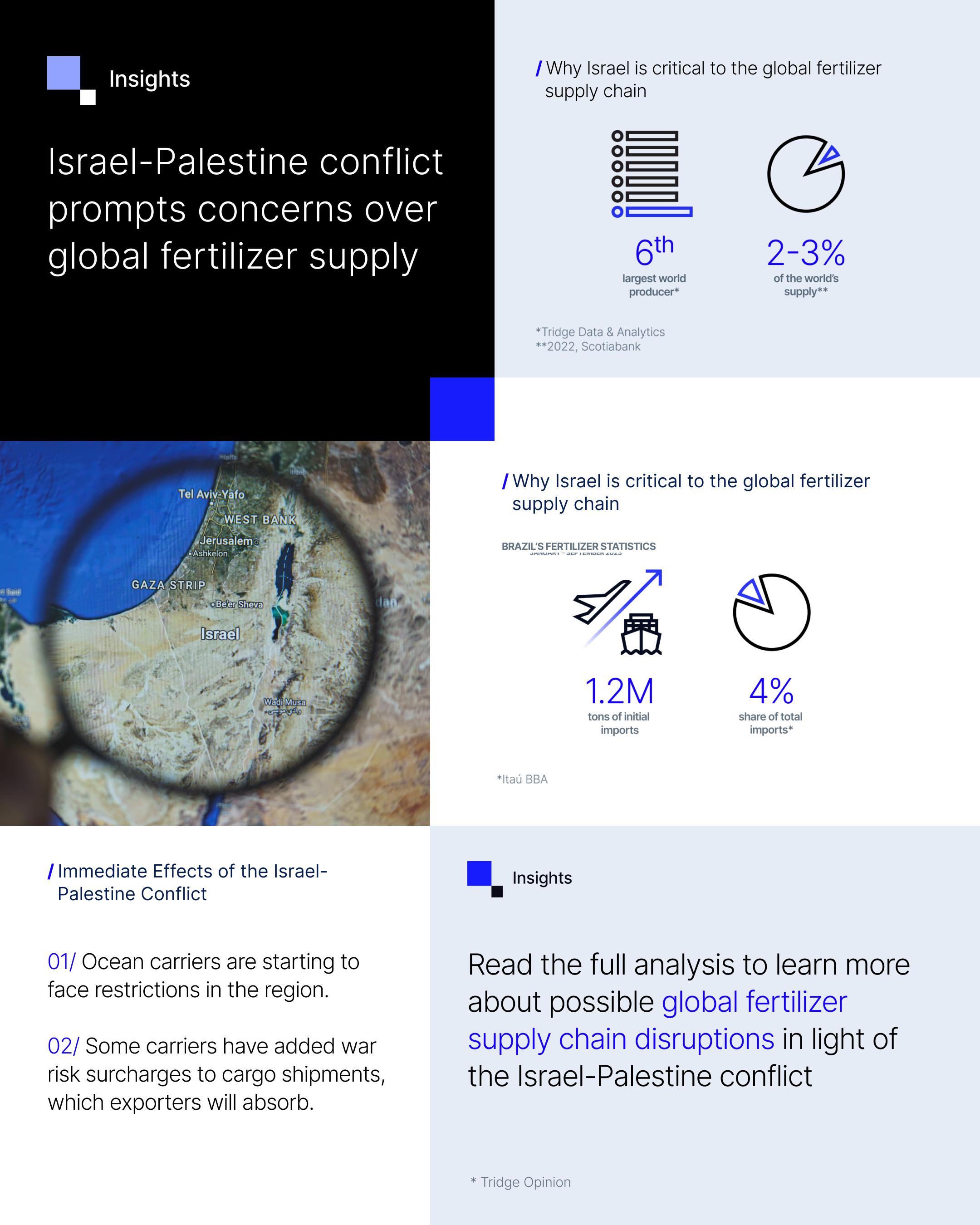

The recent escalation in the Israel-Palestine conflict has transformed into an all-out war, creating a ripple effect that carries significant potential risks for global trade. The conflict, pitting Israel against the militant Palestinian group Hamas, has raised a red flag regarding potential disruptions in the global fertilizer supply chain and the looming threat of price shocks.

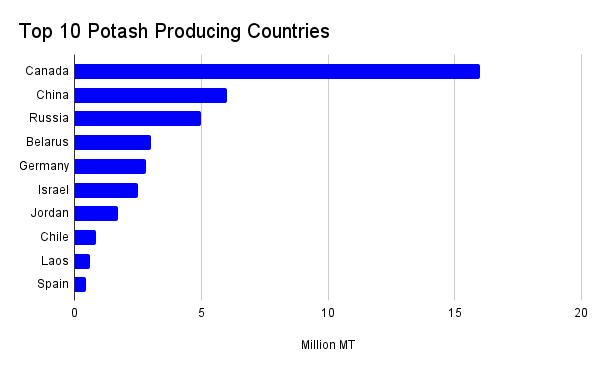

Amid this conflict, the strategic Port of Ashdod, situated approximately 30 miles from the volatile Gaza border, has been forced to operate in "emergency mode." This precarious situation renders it vulnerable to missile attacks, heightening concerns of a potential bottleneck in fertilizer shipments. The immediate concern is the global fertilizer supply, given that Israel is a prominent supplier of potash. In recent years, Potash production in Israel has displayed relative stability, consistently falling within the range of 2 million to 2.5 million metric tons (mt) since 2017. This consistency has positioned Israel as the world's sixth-largest potash producer. Within its borders, the country hosts the operations of the sixth-largest global potash-producing company, Israel Chemicals. According to estimates by Scotiabank, approximately 2% to 3% of the world's fertilizer supply now hangs in the balance due to the ongoing conflict.

Source: World Bank, Tridge

The implications of this crisis are particularly concerning to several major fertilizer markets, most notably Brazil. Israel stands as the sixth-largest fertilizer supplier to Brazil, contributing a substantial 1.2 million tons and holding a 4% share of the total imported within the first nine months of the year, totaling a notable 28.7 million tons, as reported by Itaú BBA. While the repercussions of this situation are starting to be felt in the form of price volatility, it's unlikely to cause a massive price surge akin to what occurred at the onset of the Russia-Ukraine conflict in 2022. This divergence from previous crises is due to lower global demand and increased production in countries like Belarus and Russia, which have worked to keep the potash supply balanced.

Nonetheless, the international fertilizer market is not the sole industry feeling the tremors of this conflict. It's important to note that while Israel's Ashdod Port, a critical gateway for potash exports, remains operational, the domain of ocean carriers is significantly restricted. As a result, some carriers have resorted to implementing "war risk" surcharges on cargo shipments, which the exporters subsequently absorb. To put this into perspective, the renowned Israel-based container shipping giant, ZIM Integrated Shipping Services Ltd (ZIM), is now charging an exorbitant sum of up to $120 per twenty-foot equivalent unit (TEU).

As global trade remains interconnected, the evolving situation in Israel holds the potential for far-reaching implications. The impacts on the fertilizer market are already sending ripples through agricultural and supply chain networks. The world is closely monitoring the conflict's progression, especially its potential expansion beyond the borders of Israel to Iran and Egypt. The consequences could potentially be far more severe, encompassing not just the fertilizer industry but also critical shipping routes. Such developments could introduce more substantial risks and disruptions to vital shipping choke points, including the Suez Canal and the Strait of Hormuz. The extent of these effects hinges on the course and duration of this ongoing conflict, underlining the broader repercussions of regional conflicts on the global trade landscape. Nevertheless, the extent of these repercussions remains closely tied to the trajectory of the conflict, its expansion, and its duration.

Read more relevant content

Recommended suppliers for you

What to read next