OPINIO

Original content

The European Union Deforestation Regulation (EUDR) has become a major concern for stakeholders across seven commodity products, namely soy, beef, palm oil, wood, cocoa, coffee and rubber, all of which are major drivers of deforestation. Deforestation and forest degradation continue at an alarming rate contributing more than 10% of global greenhouse gas emissions. Agricultural production is by far the primary driver of global deforestation, accounting for 80% of total forest conversion. The EU alone is responsible for importing products that account for between 13 and 16% of deforestation associated with global trade, resulting in 203,000 hectares (ha) of cleared forests and 116 million metric tons of CO₂ released into the atmosphere.

To combat the effects of deforestation and the role the EU plays, the European Commision introduced a roadmap for feedback on the initiative to tackle global deforestation in June 2020. This led to the development and ultimate adoption of the EUDR in December 2022. The EUDR will enter into effect on 30 December 2024 for large businesses and in June 2025 for small and medium enterprises and will have significant implications for several global agricultural industries, including palm oil.

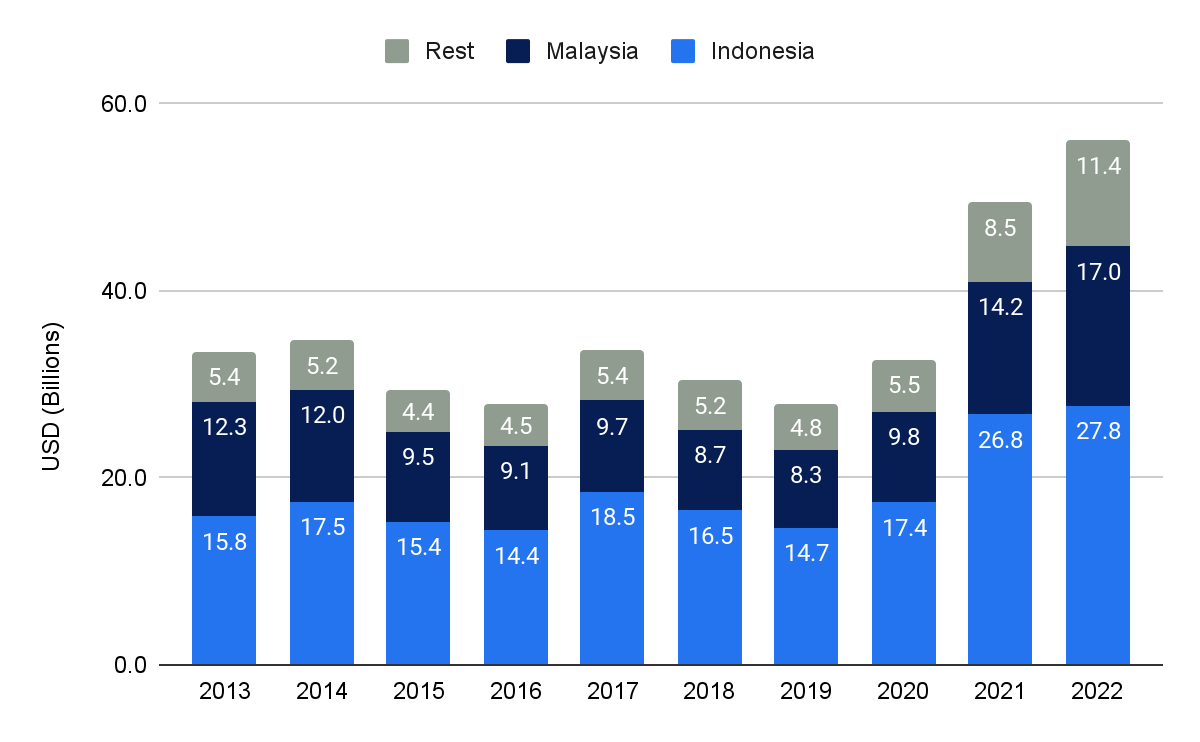

Malaysia and Indonesia are the two largest global palm oil producers globally and will be significantly affected by the new regulations. Indonesia and Malaysia are by far the two largest global palm oil exporters, respectively accounting for 49.47% and 30.3% of global export value in 2022. The exports of these two countries account for nearly 80% of global palm oil exports. Global palm oil exports grew by 67.22% in the past 10 years, from USD 33.6 billion in 2013 to USD 56.1 billion in 2022. As illustrated in Figure 1, this growth primarily occurred in 2021 and 2022.

Figure 1. Global Palm Oil Export Value from 2013 to 2022

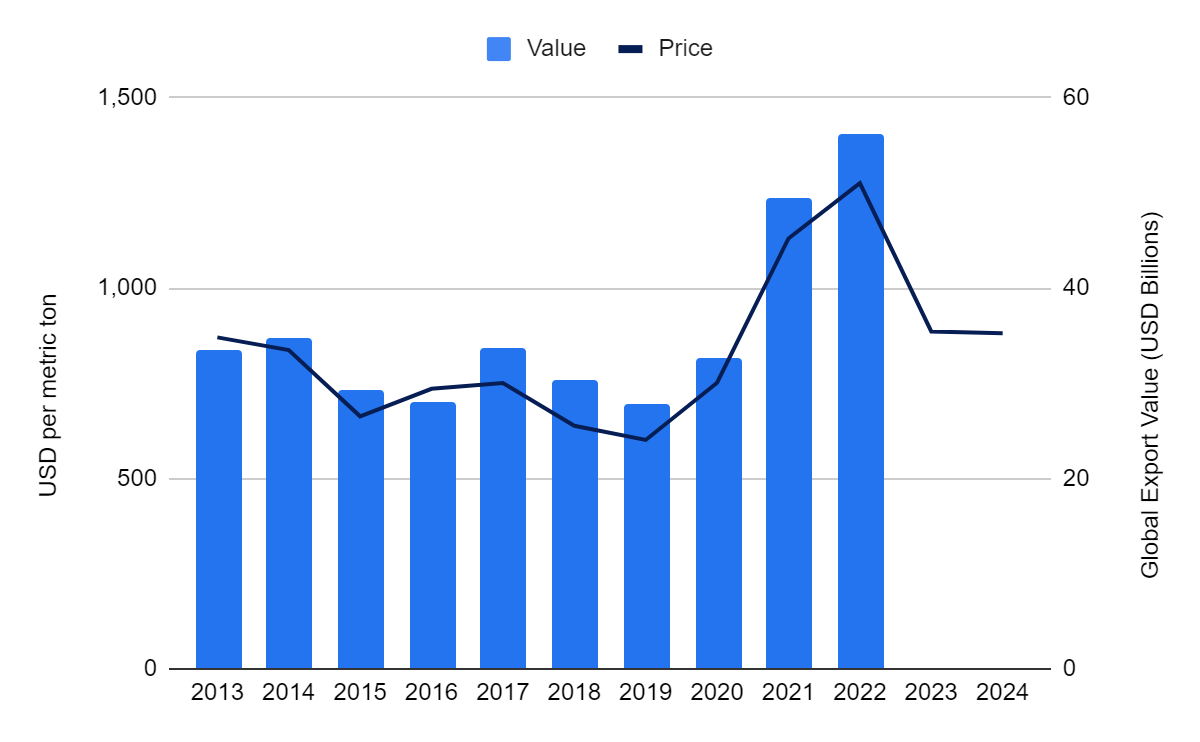

This surge in trade value was largely driven by price increases and not increases in trade volume, as illustrated in Figure 2. In 2021, palm oil prices breached the USD 1,000 per metric ton level for the first time in a decade and reached record highs on the back of Malaysia's production woes, Indonesia's high export taxes, demand recovery in India, and renewed interest in biofuels which bolstered competing soybean oil prices. However, after prices peaked in 2022, they dropped significantly in 2023 and have maintained a similar level in the Q1 2024. Resultantly, the trade value of global palm oil exports will also experience a return to lower levels in 2023 and 2024 if prices remain at current levels.

Figure 2. Global Palm Oil Export Value and Prices from 2013 to 2024

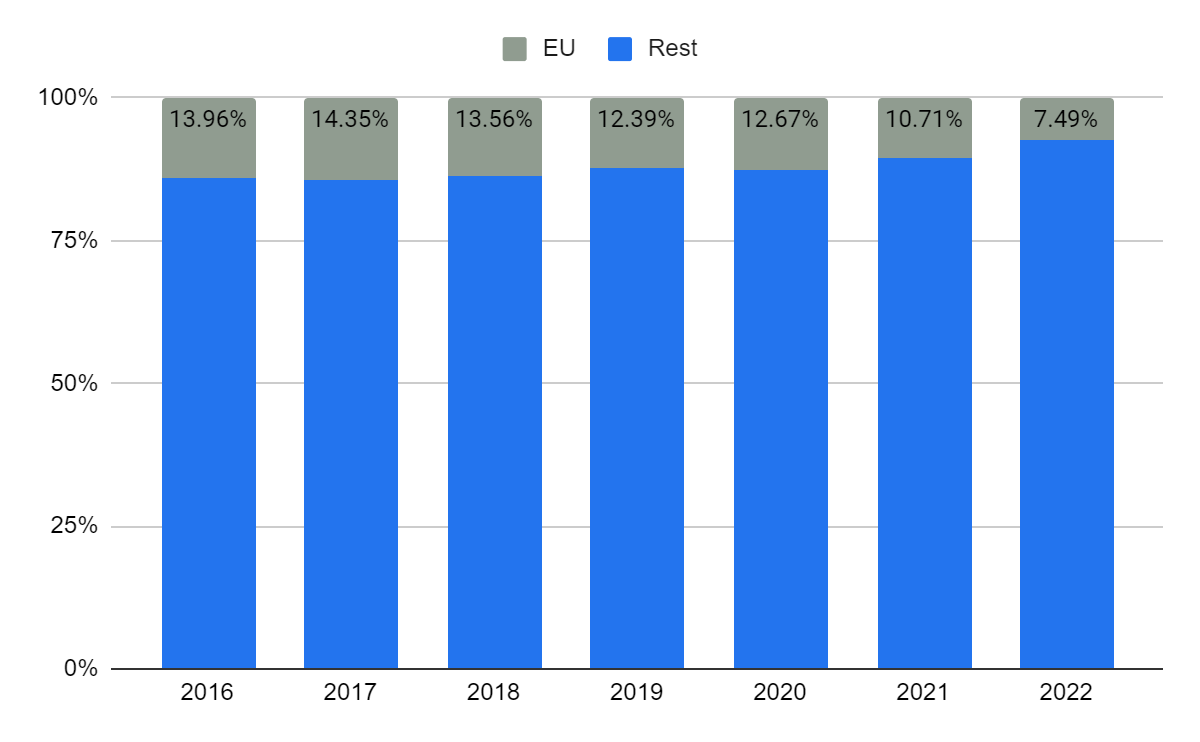

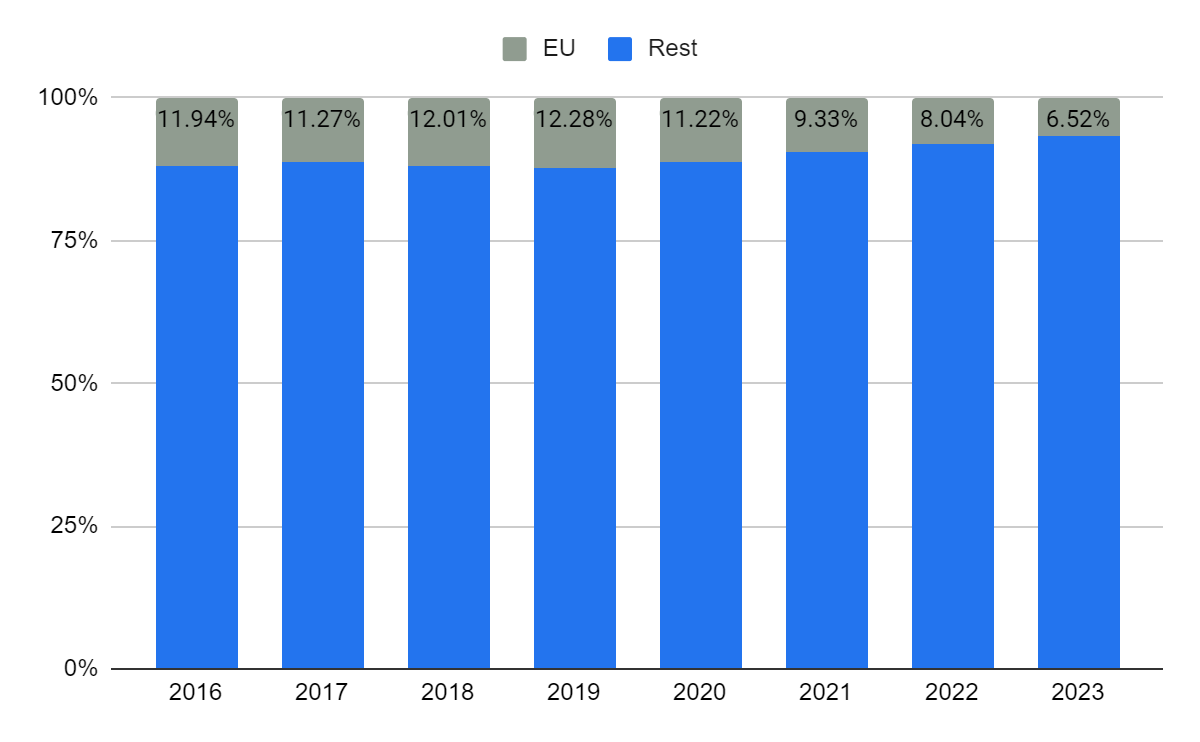

With trade values set to return to normative levels in 2024, the primary question becomes how the EUDR will affect the palm oil industries in Indonesia and Malaysia in 2025 and beyond. Since the conceptualization of the EUDR both Indonesia and Malaysia have started to reduce the percentage of exports allocated to the EU in anticipation of the inevitable introduction of the EUDR. Malaysia reduced its allocation from 11.22% in 2020 to 6.52% in 2023. Similarly, Indonesia reduced its allocation from 12.67% in 2020 to 7.49% in 2022. Although 2023 data is not available for Indonesia yet, their export allocation is likely to be in line with Malaysia at around 6.5% in 2023. These allocations are likely to decrease further in 2024 as the palm oil industries in both countries prepare to absorb the shock of the EUDR introduction.

Figure 3. Indonesia Palm Oil Exports to EU Versus Rest of the World

Thus, both Malaysia and Indonesia have started to insulate themselves against the introduction of the EUDR. Although the EU will remain an important trading part for both the Malaysian and Indonesian palm oil industries, the introduction of the EUDR is unlikely to cause major disruptions in the palm oil industry at a macro level. The most likely outcome is that the producers who can adhere to the EUDR - mostly larger scale producers - will direct their exports to the EU market while those that cannot will prioritize alternative markets. In essence, Indonesia and Malaysia have sufficiently diverse export landscapes to absorb the shock of the EUDR at the industry level.

Figure 4. Malaysia Palm Oil Exports to EU Versus Rest of the World

However, the EUDR will change the dynamics of how the domestic palm oil industries function in Indonesia and Malaysia at a micro level. Producers who still wish to export palm oil to the EU will need to adhere to the traceability and transparency requirements which will increase the time and financial resources involved in palm oil production. Furthermore, small scale farmers will be disproportionately negatively affected as they face increased difficulty in adhering to the traceability and transparency requirements of the EUDR.

For example, In Indonesia, the world's largest palm oil producer, small scale farmers manage 6.72 million ha or 41% of the country's total palm oil area. These smaller producers who are likely to struggle to adhere to EUDR regulations will lose access to the EU market. The EUDR will also increase the cost involved in accessing the EU market for producers, making palm oil production less profitable for small scale farmers. This begs the question whether it will still be profitable and financially worth it for producers to prioritize exports to the EU and adhere to the EUDR regulations.

At a macro level, major palm oil producing countries such as Indonesia and Malaysia are well insulated against the introduction of the EUDR as they do not overly rely on the EU as a trading partner and have further reduced their reliance on exports to the EU in recent years. Thus, the introduction of the EUDR is unlikely to cause significant market shocks upon its introduction at the end of 2024. However, at the micro level, small scale producers will be disproportionately negatively affected as they will face increased difficulty to adhere to the traceability and transparency regulations of the EUDR without assistance from governments and industry organizations.

Read more relevant content

Recommended suppliers for you

What to read next