OPINIO

Original content

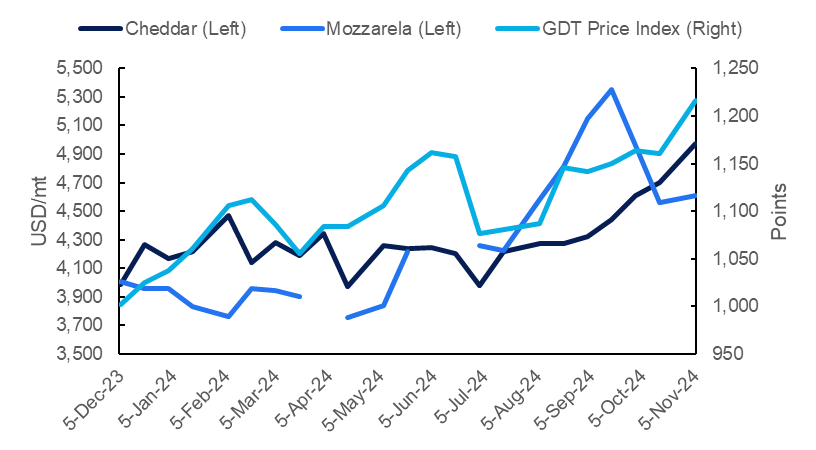

The Global Dairy Trade (GDT), the leading platform for trading primary dairy products with auctions held every two weeks, reported a price index of 1,216 points in its 367th event on November 5, 2024. This marks a 4.83% increase from the previous auction held on October 15, 2024, with the average winning price reaching USD 3,997 per metric ton (mt).

Regarding cheese dairy products, cheddar cheese was sold at an average price of USD 4,973/mt, reflecting a 5.76% rise from USD 4,702/mt in the previous auction and marking its fourth consecutive increase. Similarly, mozzarella prices rebounded after two consecutive declines, rising by 1.05% from USD 4,559/mt to USD 4,607/mt. These price increases align with the Food and Agriculture Organization's (FAO) cheese price index for Oct-24, which rose by 1.61% month-on-month (MoM) to 126 points. The FAO attributed this MoM increase to strong global import demand and limited export availability from Western Europe, where milk production has seasonally declined.

Figure 1: GDT Index and Cheese Prices Trend from 2023 to 2024

In its Oct-24 report, the United States Department of Agriculture (USDA) indicated that limited milk supplies in the European Union (EU), particularly in Western Europe, led producers to prioritize cheese production over other dairy products earlier in the year, driven by strong export growth and domestic demand. However, recent data indicates a deceleration in this shift towards cheese production. While cheese production rose by 3.8% year-over-year (YoY) in Q1-2024, growth slowed to 2.6% YoY in Q2-2024. The European Dairy Association also indicated that EU cheese stockpiles rose in Apr-24 due to increased production but decreased in Jul-24, following the typical trend of stock reductions toward year-end. Despite these fluctuations, cheese stock levels remained within the normal range.

Additionally, USDA’s Dairy Market News report indicates that milk production across Western Europe is declining, with German milk deliveries in Sep-24 down by 2.1% YoY. In the Netherlands, Sep-24 milk deliveries were 2.6% lower than in Sep-23. However, the Sep-24 decline was less steep than the 3.9% YoY drop registered in Aug-24. This reduced production is likely influenced by recent bluetongue outbreaks, which have notably impacted milk yields in Germany, the Netherlands, and Belgium, putting additional downward pressure on the region’s milk supply.

This slowdown in cheese production is expected to continue into 2025, potentially leading to higher cheese prices as processors increasingly shift back toward butter production. The USDA indicates that EU butter production, which fell by 4.3% YoY in Q1-2024, returned to 2023 levels in Q2-2024, likely driven by substantial butter price increases registered from Jan-24 to Jul-24, while cheese prices remained more stable.

In the United States (US), the USDA reported that total US cheese production, excluding cottage cheese, reached 1.16 billion pounds (lbs) in Sep-24, a 3.1% decline from Aug-24. Additionally, Italian-style cheese production totaled 487 million lbs, down 2.7% MoM, while American-style cheese output reached 456 million lbs, reflecting a 4.4% MoM decrease. Bullvine, a dairy industry news platform, noted that non-Cheddar American-style cheeses like Colby and Jack saw a 6.1% YoY drop. Cheddar and mozzarella also showed slight decreases compared to projected output. USDA data also indicated that refrigerated natural cheese stocks as of September 30, 2024, were 1% below the Aug-24 volume and 7% lower than the Sep-23 stock.

This drop in US cheese production in Sep-24 could be linked to supply chain disruptions, including high feed costs and dairy herd health issues such as highly pathogenic avian influenza (HPAI) in dairy cows, which was first confirmed in Mar-24. These factors likely impacted milk production, tightening the supply available for cheese manufacturing.

Despite a recent dip in Chicago Mercantile Exchange (CME) cheese prices, with cheese barrels averaging USD 1.8825/lb and cheese blocks at USD 1.8725/lb in the week ending November 1, 2024, reduced cheese inventories are expected to drive prices up in the near future. Processors and retailers will likely face challenges in managing stock levels and adjusting pricing strategies to accommodate shifting consumer demand, as the USDA reports a decline in food service demand for cheese while retail demand remains steady. As a result, stakeholders in the cheese industry must closely monitor these trends and proactively adapt, as continued production declines could disrupt the supply-demand balance and impact prices from farmgate to retail.

As cheese production faces challenges due to declining milk supplies and shifting priorities within the dairy sector, industry stakeholders must stay agile. By investing in supply chain diversification, flexible pricing strategies, and proactive market monitoring, industry stakeholders can mitigate the risks posed by production declines and market volatility. Long-term contracts and tailored product offerings will be key to maintaining stability while staying informed about global market trends will enable stakeholders to adapt quickly to unforeseen challenges. Strategic adaptations, informed by data-driven insights and flexible approaches, will be vital to staying competitive and meeting consumer demands in this evolving dairy market environment.

Read more relevant content

Recommended suppliers for you

What to read next