OPINIO

Original content

For more than a decade, many countries have been trying to combat deforestation with significant efforts such as Reducing Emissions from Deforestation and forest Degradation (REDD). In line with this, the European Union (EU) legislated the European Union Deforestation Regulation (EUDR). At the same time, several organizations like S&P Global are showing concern about the impacts of the EUDR on the related markets with various perspectives like costs or market chain.

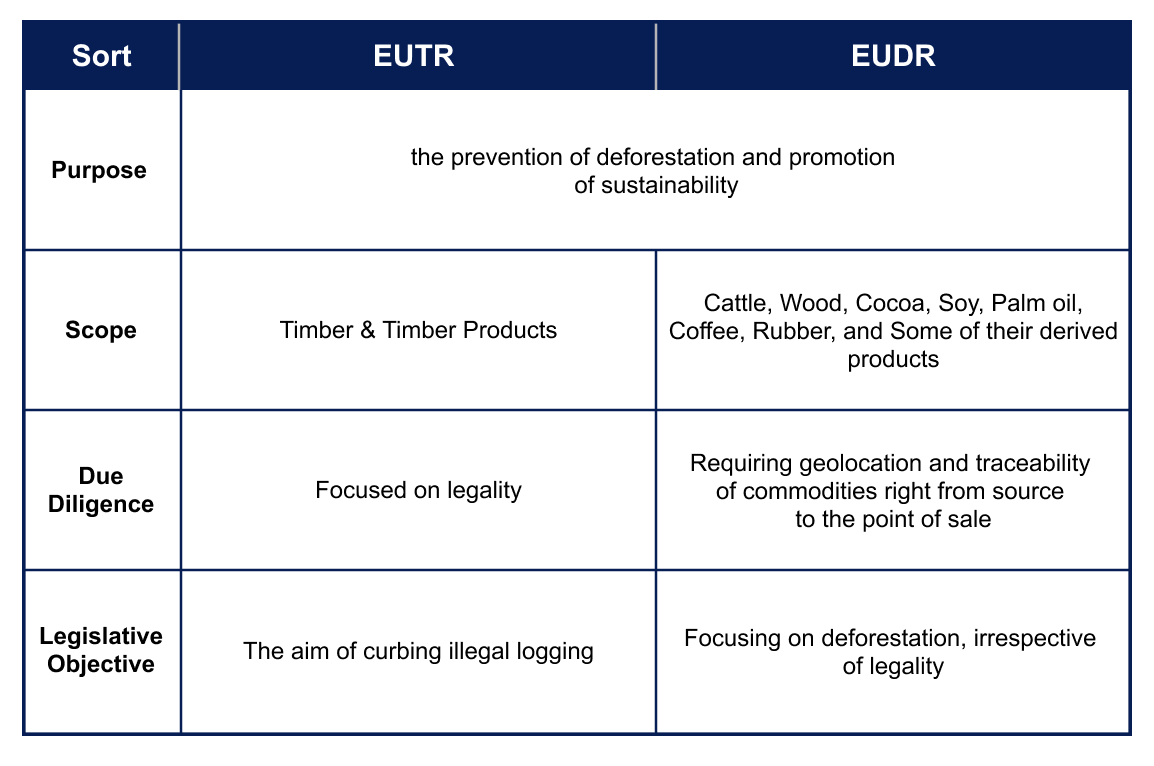

The EUDR aims to prevent deforestation and forest degradation by fostering production and consumption of deforestation-free products. The product list the regulation covers include cattle, cocoa, coffee, oil palm, soya, rubber, wood, among others. The EUDR was enforced on June 29, 2023 and the affected enterprises have almost 18 months to adhere to the regulations(Small and medium-sized enterprises have almost 24 months). The EUDR is similar to the European Union Timber Regulation (EUTR) ,which was enforced in May, 2013. The EUTR’ purpose is the same as the EUDR but with a few differences. Refer to the table below for the comparison.

Figure 1. EUDR vs EUTR

The EUDR and EUTR require the concerned suppliers to demonstrate that their products are not linked with deforestation. This will make operational costs higher than before and will influence the affected supply chains.Tridge seeks to forecast the future impact of the EUDR on the affected markets, comparing it with the market impact of the EUTR.

The core idea remains consistent for both the EUTR and EUDR. Concerned enterprises must manage increased operational costs after implementation, which could impact the supply chain and market prices. Case studies from the International Tropical Timber Organization (ITTO) and the Joint Research Center (JRC) regarding the EUTR must be examined to try to forecast the impacts of the EUDR.

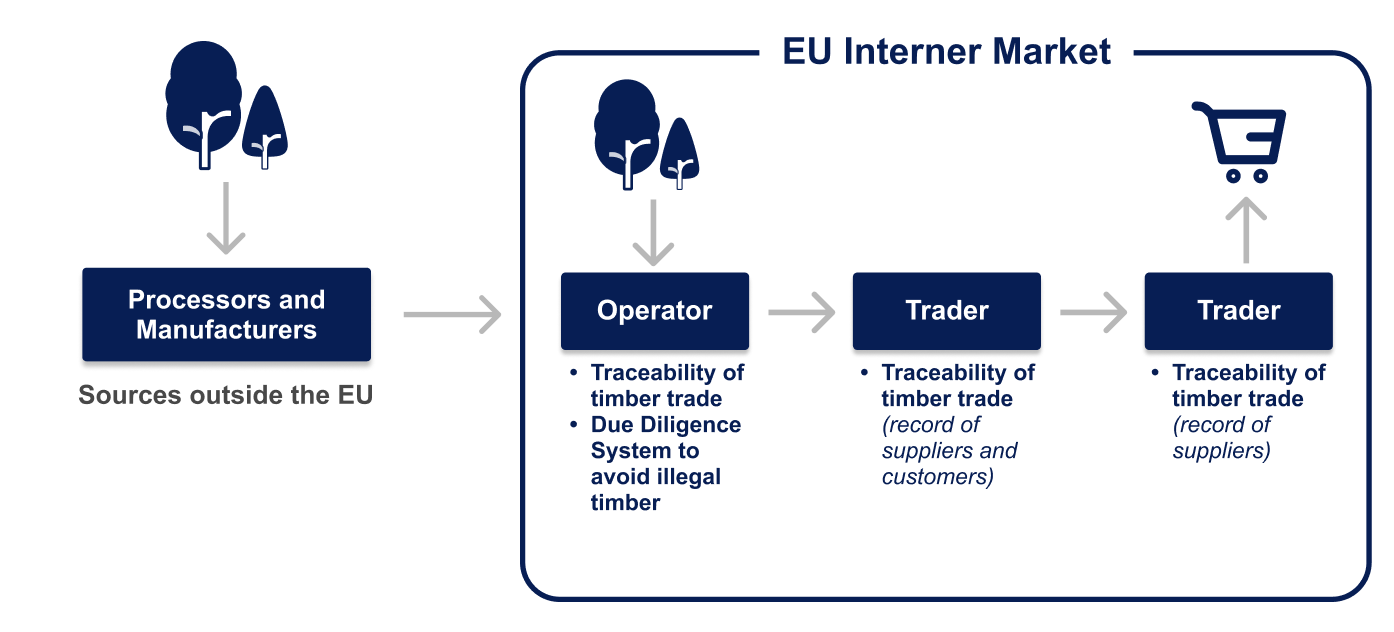

Figure 2. The Structure of EUTR

In its research, the ITTO analyzed price and import data for timber products before and after the EUTR was implemented. Contrary to concerns that the EUTR would reduce the consumption of imported products, the data analysis revealed that the regulation did not significantly impact the supply chain.

In the research conducted by the JRC, the results slightly differed. While the analysis did not provide a definitive picture of potential structural changes in the supply chain, it showed that the import prices of regulated products increased, and their import quantities decreased gradually and immensely over nearly a decade. This suggests that structural changes in the supply chain were significant but not abrupt.

The findings from the JRC research are understandable, considering that the ITTO research took place just one year after the EUTR was implemented, whereas the JRC research took place nine years after the regulation was implemented.

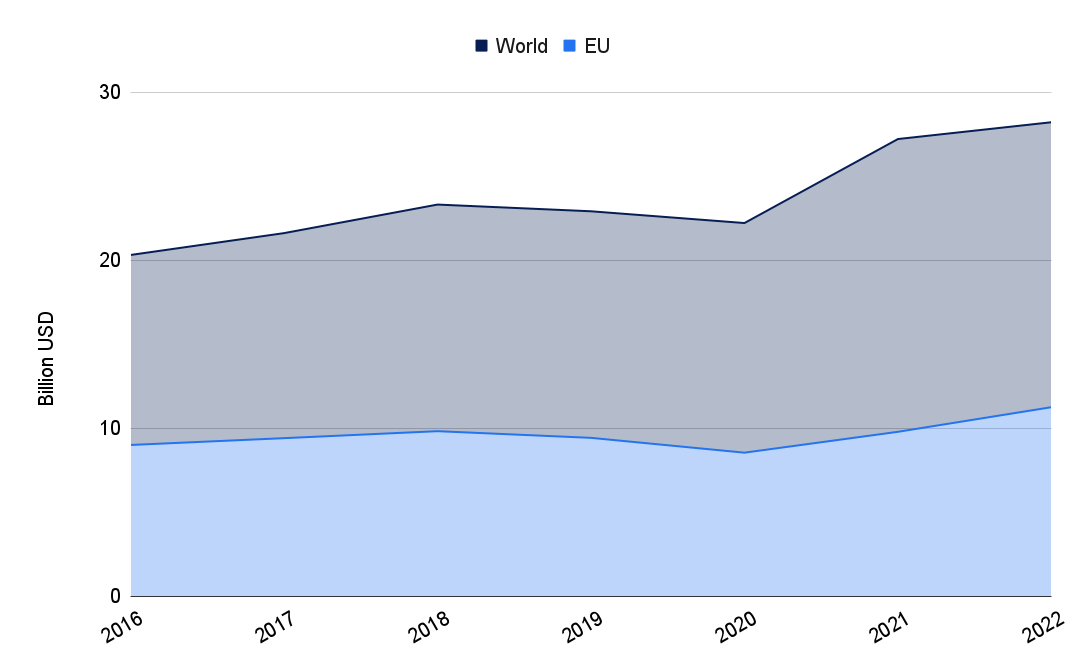

To understand the potential impact of the EUDR on market chains, Tridge analyzed the EU’s beef import (HS Code 0201). According to Tridge data, twelve of the top 30 beef-importing countries are EU countries, including Italy, Germany, and the Netherlands. In 2022, the value of beef imports to these countries reached $11 billion, accounting for 44% of the global beef imports. This significant proportion suggests the possibility that the EUDR could substantially affect the supply chains gradually. Given the fact that the two studies on the EUTR had limitations, such as narrow data coverage, the findings must be applied to the EUDR scenario with caution.

Figure 3. The value of Cattle imported into EU countries (HS Code 0201)

While the EUDR shares similarities with the EUTR in terms of addressing deforestation concerns, the market dynamics involved in each regulation differ considerably. A closer examination of import data for products affected by the EUDR, such as beef, coffee, and cocoa, reveals distinct characteristics that suggest a more significant impact on supply chains compared to the EUTR's impact on timber supply chains.

Unlike the gradual and limited impact observed with the EUTR, the EUDR is expected to have a more pronounced effect on supply chains for products covered by the regulation. For instance, the stringent requirements of the EUDR may necessitate substantial changes in sourcing practices, supply chain management, and product labeling for affected industries. This could result in disruptions and adjustments across various stages of the supply chain, potentially leading to shifts in trade patterns and market dynamics. Additionally, supply chains for products, such as cocoa and coffee include many smallholder farmers who could struggle to comply with the traceability requirements underlined in the EUDR regulations. Another important point to note is that the EUDR focuses on many food products, which have specific market dynamics that differ considerably to those of timber which is the sole focus of the EUTR.

Therefore, it is essential to recognize that the market impact of the EUTR may not accurately predict the potential impact of the EUDR on affected markets. Instead, a thorough assessment of the specific market dynamics surrounding each product covered by the EUDR is necessary to gauge its potential implications for trade and supply chains. This tailored approach will enable stakeholders to better understand the challenges and opportunities presented by the regulation and to develop effective strategies for compliance and adaptation.

Read more relevant content

Recommended suppliers for you

What to read next