OPINIO

Original content

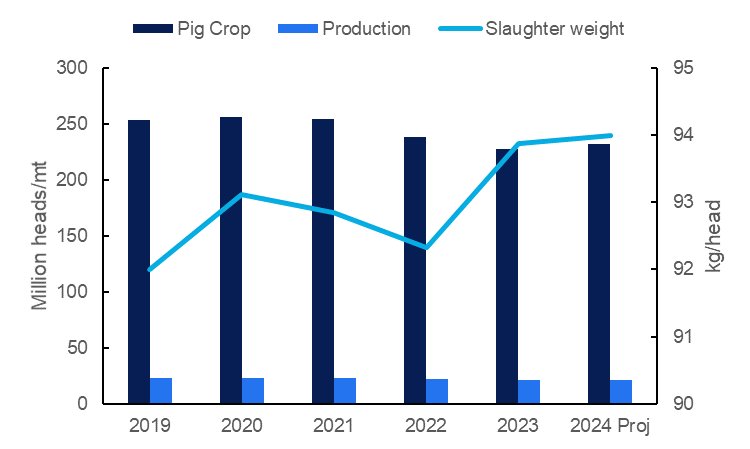

According to the United States Department of Agriculture (USDA), pork production in the European Union (EU) is expected to reach 21.15 million metric tons (mmt) in 2024. This represents an upward revision of 2.17% compared to the Jan-24 estimate of 20.7 mmt and a 1.44% increase over the 2023 volume of 20.85 mmt. Following two consecutive years of decline, this anticipated rebound is primarily attributed to the expected uptick in pig slaughter, forecasted to total 225 million heads in 2024, a 2.27% rise from the Jan-24 projection and a 1.3% increase from the 2023 level. Concurrently, the slaughter weight per pig is expected to reach approximately 94 kilograms (kg) in 2024, indicating a 1.5% increase compared to the 93.86 kg recorded in 2023. It's worth noting that farmers capitalized on lower feed prices in 2023 than those in 2022, allowing them to fatten their pigs to the highest feasible weight manageable at their farms and acceptable to slaughterers.

Figure 1: EU Pig Crop, Production, and Slaughter Weight from 2019 to 2024

The EU pig herd is projected to rise in 2024 after experiencing a slowdown in contraction witnessed since 2021, with 2023 showing nearly stagnant numbers. According to USDA data, the EU pig herd stood at 133.58 thousand heads at the beginning of 2024, a slight decrease of 0.62% compared to the 134.41 thousand heads recorded in 2023. Notably, the opening stock in 2023 was 5.13% lower than the 2022 volume of 141.68 thousand heads, which was 2.9% less than the 145.91 thousand heads reported in 2021.

The anticipated resurgence in the EU pig herd is further underpinned by the increase in the sow population during 2023, reaching approximately 10.58 thousand heads at the start of 2024, a 1.73% year-on-year (YoY) increase. Notably, record piglet and carcass prices, coupled with declining feed costs in 2023, incentivized reinvestment in the pig sector due to favorable profit margins for both fatteners and breeders. The expansion of the sow herd suggests that the EU pig crop is estimated to reach 232 thousand heads in 2024, a 4.04% increase from the Jan-24 estimate and a 1.75% YoY rise. The most significant increases in the pig crop are expected in Spain, Denmark, the Netherlands, and Poland.

The USDA forecasts EU pork exports to increase by 4.84% YoY in 2024, totaling 3.25 mmt, following a notable 25.75% YoY decline in 2023. This positive projection is attributed to the expected increase in exportable supplies and a rebound in demand from China, the primary destination, as its domestic production is forecast to decrease in 2024 due to a reduction in the pig herd. The decline in EU pork shipments in 2023 was mainly due to sluggish demand in China, where the anticipated consumption resurgence after the removal of COVID-19 restrictions did not materialize. At the same time, China witnessed increased production in 2023 due to heightened pig slaughter as several pig firms opted to sell off their pigs to bolster cash flows amid a slowing economy.

The European Commission (EC) indicates that EU exports to China amounted to 1.14 mmt in 2023, a significant 24% YoY drop, but accounted for about 37% of the total shipments. Other countries that registered decreases in pork imports from the EU in 2023 were Japan with 299.3 thousand metric tons (mt), a 22% YoY decrease, the Philippines with 222.85 thousand mt (-35.79% YoY), and South Korea with 214.47 thousand mt (-22.21% YoY). The United Kingdom registered an 8.95% YoY increase in imports from the EU, recording 367.77 thousand mt in 2023.

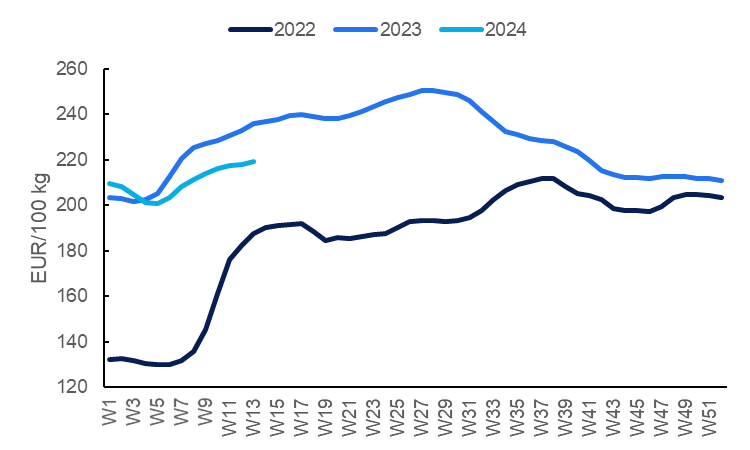

According to EC data, the average price of class E pig carcasses stood at EUR 219.47 per 100 kg in W13, a 0.61% week-on-week (WoW) increase but a 7.06% drop compared to the same period in 2023. Notably, 2024 began with declining prices in the initial five weeks, a trend that started in W49 of 2023 due to seasonal weak demand during Europe's winter season. Prices then began to ascend from W6, primarily due to tightening supplies amidst heightened demand during the Easter holidays. These prices are anticipated to continue their upward trajectory in the coming months as demand surges toward the summer season.

Figure 2: EU Pig Carcass Prices of Class E from 2022 to 2024

However, the USDA forecasts total pork consumption to reach 17.7 mmt in 2024, a 0.90% decline from 17.86 mmt in 2023, a trend observed for approximately 15 years. This consumption downturn is attributed to consumer preferences shifting towards healthier diets and more affordable alternatives amid the challenging economic landscape. Poultry meat, considered a healthier dietary option with lower prices compared to other proteins, is gaining traction among consumers. Despite this trend, the USDA anticipates that the increase in pork supply in the domestic market could support consumption recovery in Poland, Hungary, Bulgaria, and Greece in 2024.

In conclusion, the outlook for the EU pork industry in 2024 appears optimistic, with projections of growth in both production and exports. Nevertheless, EU pork exporters may encounter significant competition from countries like Brazil and the United States, primarily due to price competitiveness. Expectations indicate that pork prices will follow their typical seasonal pattern, declining in the winter months and rising during the summer. However, it is anticipated that prices in 2024 will remain below those of 2023 but above the rates observed in 2022.

Read more relevant content

Recommended suppliers for you

What to read next