OPINIO

Original content

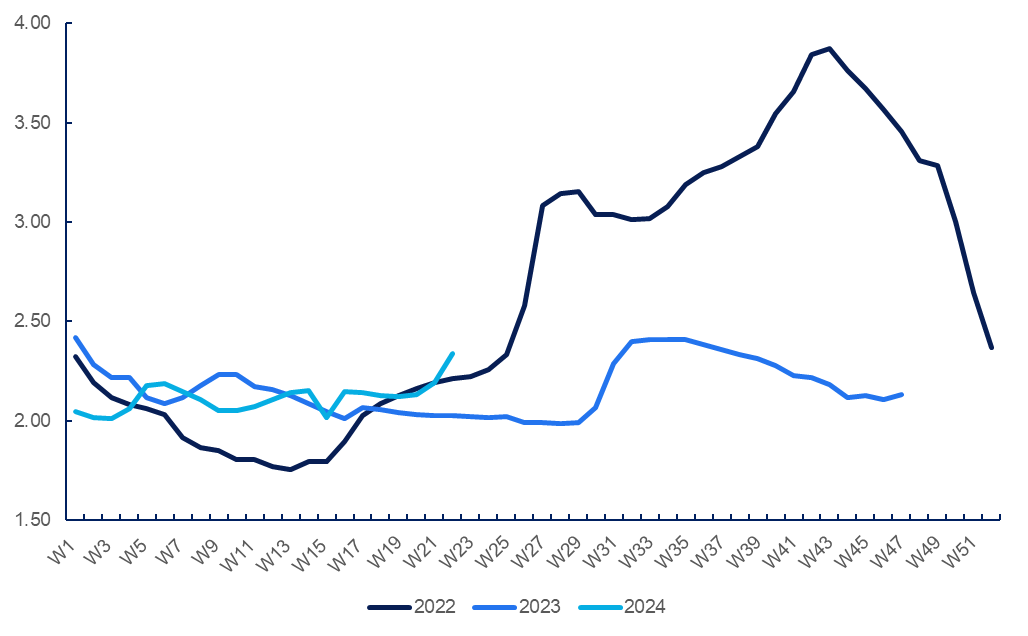

Pig prices in China started rebounding in 2024 after experiencing low prices in 2023, with an average of USD 2.16 per kilogram (kg), 18.80% below the 2022 average. According to data from Pig333, a comprehensive online resource dedicated to the global swine industry, the live pig price averaged USD 2.34/kg (CNY 16.70/kg) in W22, marking the highest value so far in 2024. This represents a 6.85% week-on-week (WoW) increase and a 15.27% year-on-year (YoY) rise. Notably, pig prices experienced a slight increase between late Jan-24 and early Feb-24, attributed to higher demand during the Chinese New Year holiday, but subsequently returned to lower levels.

Figure 1: China’s Pig Price Trend from 2022 to 2024

The recent rise in pig prices can be attributed to improvements in the supply and demand situation resulting from government intervention. In early Mar-24, the Chinese government issued new guidelines to control the pig population to avoid an oversupply.

The new regulation includes lowering the normal retention target for breeding sows from 41 million heads, as indicated in 2021, to 39 million heads, allowing for a reduction in the number of pigs. This policy also categorizes the fluctuation levels of breeding sow stocks into three ranges: green for normal levels, yellow for big fluctuations, and red for excessive fluctuations that require intervention. Notably, the African swine fever (ASF) outbreak in 2018 significantly reduced China’s pig population, leading farmers to ramp up production, resulting in the current oversupply.

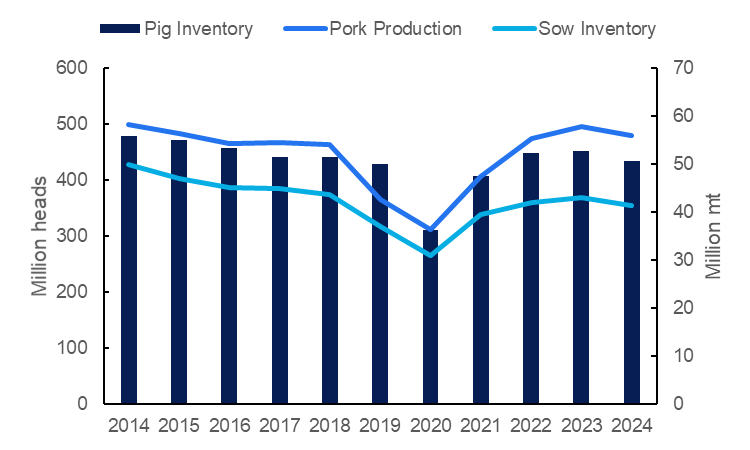

The United States Department of Agriculture (USDA) anticipated a 3.43% YoY drop in China’s pork production in 2024, expecting output to reach 55.95 million metric tons (mmt) by year-end. This outlook was attributed to an anticipated 3.67% YoY decrease in sow inventory due to herd liquidation in 2023, driven by low pork prices and high production costs that squeezed profit margins. This forecast is materializing, as China's National Bureau of Statistics reported that by the end of Mar-24, the national pig inventory stood at 408.5 million heads, a 5.9% month-on-month (MoM) drop and a 5.2% YoY decline. Additionally, the Ministry of Agriculture and Rural Affairs (MARA) reported that sow inventory totaled 39.96 million heads as of Apr-24, a 9.20% decrease compared to Dec-23 and indicating a continuous downward trend since Jun-23.

Figure 2: China’s Pig Inventor and Pork Production from 2014 to 2024

It is also worth noting that the recent increase in pig prices has brought relief to producers, increasing profitability significantly. This profitability is attributed to the general downward trend in production costs, particularly feed prices, since the beginning of the year. MARA indicates that the prices of corn and soybean meal have dropped from USD 0.38/kg (CNY 2.76/kg) and USD 0.59/kg (CNY 4.27/kg) in the first week of Jan-24 to USD 0.35/kg (CNY 2.54/kg) and USD 0.52/kg (CNY 3.75/kg) in the fourth week of May-24, respectively. As a result, the current cost of breeding is USD 2.14/kg (CNY 15.5/kg), indicating a profit of USD 0.02/kg (CNY 0.14/kg).

In conclusion, the recent rebound in pig prices in China signals a promising shift in the market after a period of decline in 2023. As a result, pig prices are anticipated to increase in the coming months due to the Chinese government's intervention in balancing supply and demand. Additionally, the expected rise in pork demand towards the Autumn holiday season will likely keep pig prices elevated. This situation will also ensure that the pig industry remains fully profitable, supported by lower production costs. Therefore, stakeholders should now monitor market dynamics closely, capitalize on favorable conditions, and adapt strategies to navigate potential fluctuations in supply and demand.

Read more relevant content

Recommended suppliers for you

What to read next