OPINIO

Original content

Over the last couple of years, Chile's oats cultivation has demonstrated fluctuating behavior. However, from 2019 to 2022 area and production showed a noticeable upward trajectory, influenced by global demand for oats for human consumption. Recognizing oats' significance for food security and as a rotational crop with wheat, the Ministry of Agriculture, led by the Office of Agrarian Studies and Policies (Odepa), aims to foster sector development by enhancing information availability and advocating for regulatory improvements to improve market transparency.

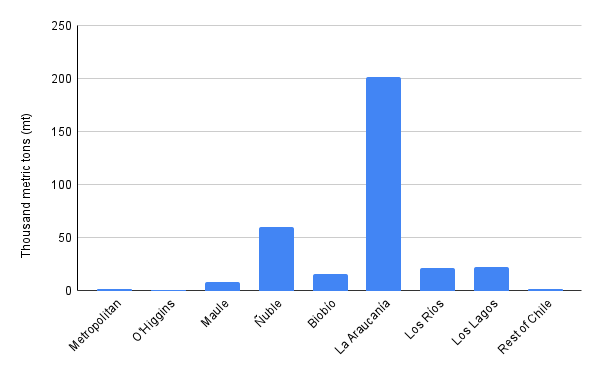

During the 2022/23 season, the National Statistics Institute (INE) reported a national oats area of 71.68 thousand hectares (ha) for Chile, marking a 41.9% decrease from the previous season. Estimated production stood at 333.07 thousand metric tons (mt), with a national average yield of 4.65 mt/ha. Regionally, Araucanía dominated, contributing 59.3% of the area and 60.6% of production, with average yields of 4.75 mt/ha. Followed by the Ñuble region, with 18.2% of the area and 18.1% of production, with yields of 4.62 mt/ha, while Biobío accounted for 7.0% and 4.7%, respectively, with yields of 3.17 mt/ha. The planted area of the crop is cyclical, reaching its historical maximum in 2017, with 136.81 thousand ha. From 2019 to 2022, it presented an upward trend from 74.61 thousand ha to 123.44 thousand ha, followed by a 42% drop in 2022.

Figure 1. Estimated oat production by region during season 2022/2023

Oats exports are classified into three categories: feed oats, raw grain oats, and processed oats. The main product exported is processed oats, accounting for 99.5% of the volume. Fodder oats represented 0.3% by volume and raw grain oats 0.15% of total oats exported. In terms of export value (Free On Board US Dollars), processed oats accounted for 99.7%, feed oats 0.21% and raw grain oats 0.1% of total exports in 2023.

Figure 2. Oats exports volume by type of product from 2019 to 2023

Over the past five years, the export of oats for fodder purposes has seen consistent growth, with exports reaching nine destinations annually on average. Colombia, Ecuador, Panama, Guatemala, and the Dominican Republic have emerged as frequent destinations, with Panama, Guatemala, and Colombia leading in export volumes. In 2023, due to the absence of Guatemala in the market, Colombia and Panama stood out as primary export destinations, comprising 47.9% and 20.7% of the total exported volume, respectively. Seventeen companies participated in the forage oats export market from 2019 to 2023, with two companies dominating the market in 2023, representing 82% of the exported volume.

Conversely, raw grain oats exports declined in 2023, with only Guatemala and the Dominican Republic receiving shipments, marking a 99.5% decrease compared to 2022 volumes. Eighteen companies participated in the raw grain oats export market from 2019 to 2023, with three companies monopolizing the market in 2023.

Processed oats exports mainly consist of flaked oats and peeled oats. Peeled oats have been consistently exported to 23 destinations, averaging 18 destinations annually. Each year, shipments are recorded to 15 countries, with Peru, Colombia, and Guatemala emerging as significant recipients, representing 29.6%, 22.7%, and 21.6% of peeled oats exported in 2023, respectively. Available data indicates a sustained upward trend in the average FOB price of peeled oats, except in 2022. Guatemala experienced a considerable increase of 40% in their export prices between 2019 and 2023, followed by Peru with 39%, reflecting a positive market trend. Furthermore, a total of 28 companies exported peeled oats. An examination of company participation reveals a significant concentration, with the leading performer consistently capturing between 37% and 46% of exports over the last five years. In 2023, the top four companies collectively accounted for 79% of the total volume exported, indicating a notable dominance in the market.

Chile's oat crop demonstrated cyclical behavior influenced by foreign trade dynamics, impacting domestic prices in response to supply and demand fluctuations. Despite a decrease in oat area in the 2022/23 season, projections suggest a 5.8% increase in the upcoming 2023/24 season, albeit insufficient to match 2022 levels. The modernization of the Chile-European Union agreement presents new export opportunities, particularly in processed oats. Notably, there's a concentration of processed oats in the Americas market. Imports, predominantly raw grain oats, exhibit stable behavior, except in 2022. The Agriculture and Livestock Service’s (SAG) efforts for the 2024 season include dissemination of regulations, training, and inspection to reinforce transactional aspects and improve producer representation and complaint channels.

Read more relevant content

Recommended suppliers for you

What to read next