News

Original content

Peanut production in Argentina remains one of the few sectors showing resilience amid economic challenges affecting regional agriculture. While many crops struggle with low domestic demand, high costs, and export difficulties due to an uncompetitive exchange rate, peanuts have maintained stable production levels and secured favorable market positioning. Despite broader economic challenges, the peanut sector continues to expand into niche markets and achieve relatively positive prices, distinguishing it from other struggling agricultural industries.

Drought conditions in Mexico's El Valle, Mocorito have severely impacted agricultural production, leading to a 90% reduction in irrigated crop planting for the spring-summer season. While crops like watermelon, pumpkin, and corn have been largely abandoned due to water shortages, peanut farmers are struggling with low yields and unfavorable market prices. Many are opting to sell their remaining stocks to other regions, such as Puebla, while also preserving some as seeds for future planting. The ongoing drought has left many farmers without work, relying on savings as they await the next rainy season.

Nicaragua's peanut production for the 2024/25 cycle reached 4.3 million quintals, primarily cultivated in León and Chinandega, where conditions favor strong yields. Peanuts serve as a key raw material for both domestic industries and exports. The government continues to support the sector through innovation and technology initiatives aimed at sustainable development.

Recent heavy rains in Vietnam, particularly between February 23 and 25, have caused significant flooding, impacting the 2024/25 winter-spring rice and peanut crops. Caused by cold air, the rains affected several regions, including Bình Định province, where the Côn River overflowed, severely flooding districts like Tuy Phước and Phù Cát. Around 7 hectares (ha) of peanuts in the Tây Sơn district, linked to a production-consumption project in Bình Thuận commune, have been flooded, with over 70% of the crop potentially damaged. Local authorities are working to assess and mitigate damage while monitoring ongoing flood control efforts.

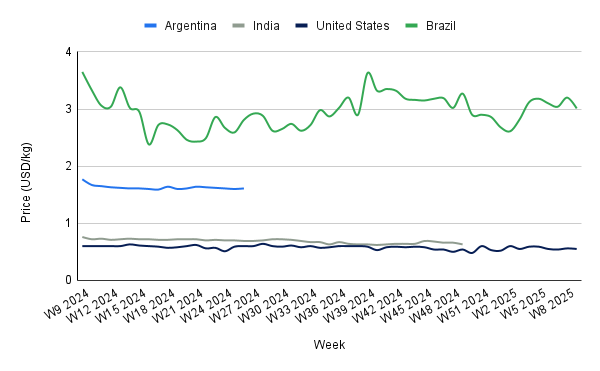

In W9, the United States (US) peanut prices fell to USD 0.55 per kilogram (kg), marking a 1.79% week-on-week (WoW) drop and an 8.33% year-on-year (YoY) decline. Farmer stock peanut prices also dropped slightly, with reduced marketings reflecting lower demand or slower movement. The estimated 2024 crop of 3.2 mmt, along with a projected carryout of 757,221 mt, indicates stable supply levels. However, increasing competition from Brazil and Argentina may restrict price recovery in export markets. Future price movements will be influenced by 2025 acreage decisions, input costs, and global trade conditions. Expanding acreage or weaker exports could pressure prices further, while reduced planting or supply disruptions may provide support.

Brazil's peanut prices declined to USD 3.01/kg in W9, reflecting a 5.94% WoW drop and a 17.53% decrease YoY. Improved weather conditions in São Paulo have supported a production rebound, while integration with sugarcane farming has bolstered supply stability. As the harvest progresses, increased output could continue to exert downward pressure on prices. However, potential weather disruptions may introduce volatility. Future price movements will largely depend on harvest conditions, policy developments, and global demand trends, shaping both domestic and export market dynamics.

Given Argentina's stable peanut production amid broader economic challenges, industry stakeholders should consider forming long-term supply contracts with Argentine producers to ensure a consistent supply of peanuts. This strategy would mitigate the risks posed by volatility in other regions like Mexico and Vietnam, where adverse weather conditions have impacted peanut crops. Additionally, exporters should explore opportunities to increase shipments to niche markets where demand is growing, further strengthening Argentina's market position.

Peanut farmers and traders in Vietnam and Brazil should closely monitor the impact of weather patterns, such as flooding in Vietnam and potential weather disruptions in Brazil, which may influence supply and prices. To mitigate risks, traders should diversify their supply chains and explore storage solutions to buffer against unexpected market fluctuations. Furthermore, fostering relationships with local authorities and agricultural experts can help predict weather-related challenges and ensure more efficient responses to crop damage.

Sources: Tridge, Nongnghiep, El 19, Debate Sinaloa, El Territorio

Read more relevant content

Recommended suppliers for you

What to read next