News

Original content

Argentina’s beef sector is navigating a complex international landscape marked by rising global demand, stronger beef prices, which are up by between 15% to 20%, and export tax cuts from 6.75% to 5% have helped boost exports and improve market sentiment. However, United States (US)-imposed high tariffs on Brazilian beef may redirect large volumes to China, where oversupply could depress prices, impacting Argentina’s largest export destination. Domestically, despite a slight increase in beef consumption to 50.1 kilogram (kg) per capita, 5.2% higher year-on-year (YoY), structural issues persist. Cattle stocks have fallen to a 20-year low, calf weaning rates remain weak, and recovery in herd numbers is uncertain, limiting future production capacity. While recent fiscal measures support competitiveness, supply constraints and shifting trade flows present ongoing challenges for Argentina’s beef industry.

The recent US decision to impose a 50% tariff on Brazilian products, excluding beef from exemption, has placed significant pressure on Brazil’s beef industry. The Brazilian Association of Meat Exporting Industries (ABIEC) warned that the tariff, raising total duties on beef to 76.4%, could result in an estimated loss of USD 1 billion and derail plans to export 400 thousand metric tons (mt) of beef to the US in 2025. With 30 thousand mt of beef already en route to US ports, exporters rushed to clear shipments before the revised August 10 deadline to avoid added costs. While some cargo was rerouted to Mexico, industry leaders stress that no alternative market offers the same volume potential and profitability as the US, especially given America’s severe cattle shortage. The move is feared to disrupt supply chains, threaten food security, and fuel inflation in the US, where Brazilian beef is heavily used for hamburger production. Although the market reacted with a temporary rise in meatpacker stocks, industry leaders are calling for urgent diplomatic talks to protect trade and avoid long-term damage to the sector.

In the latest US–South Korea trade negotiations, South Korea reaffirmed its stance against further opening its beef and rice markets. South Korean authorities noted that 99.7% of its agricultural and livestock markets are already open to the US, with the remaining 0.3% deemed off-limits due to high sensitivity. While the US announced a reduction in its tariff on South Korean goods from 25% to 15% and stated that the market would further open to American agricultural products, South Korean authorities clarified that this would not include beef. Ongoing discussions on non-tariff barriers, such as adjustments to quarantine procedures, may facilitate customs processes but will not lead to increased import quotas or market liberalization. Agricultural stakeholders have expressed concern over potential future pressure and emphasized that food sovereignty and public health standards must remain non-negotiable.

Ahead of the summer vacation season, South Korea’s Hanwoo Self-Help Fund Management Committee and the National Hanwoo Association identified 184 economical Hanwoo stores offering premium Korean beef cuts like sirloin at prices 25% to 30% lower than average. Verified through site visits or calls by the National Hanwoo Association, these outlets were selected based on pricing thresholds for Hanwoo grades such as Grade 1++ at USD 12.94/100 grams (KRW 18,000/100g) or less. This initiative aims to support consumer access to affordable, high-quality Korean beef and strengthen transparency through a public database. Survey results show that domestic consumers are increasingly prioritizing the country of origin when buying meat, with 74% preferring Korean beef. However, during holidays like Chuseok, cheaper imported beef gains market share. In response, efforts are underway to reinforce Hanwoo’s premium image and maintain its competitiveness amid shifting consumption trends.

In its Jul-25 report, the United States Department of Agriculture (USDA) indicates that the US beef sector remains stable and influential, supported by a large inventory of 28.7 million beef cattle and 13 million animals in feedlots, enabling swift market response to demand changes. This structure reinforces the country’s role as a key global supplier, especially as international demand for beef rises. However, the industry faces mounting challenges, including weather-related risks, evolving dietary preferences, rising competition from plant-based proteins, and intensifying trade tensions. Markets such as Mexico continue to offer growth potential, driven by rising demand for high-quality meat products. However, this is tempered by growing protectionist measures, such as tariffs and import restrictions, which could disrupt established trade flows and elevate operational uncertainty. As global competition intensifies and geopolitical risks grow, the US beef sector must navigate these uncertainties to maintain its competitive edge in export markets.

While the US aggressively seeks to expand beef and other agricultural exports to Mexico, capitalizing on rising demand from the affluent and quality-conscious Mexican middle class, it has simultaneously tightened controls on Mexican imports, including the suspension of cattle crossings due to a screwworm outbreak. This halt in cattle exports has triggered significant financial losses for Mexican producers, estimated at USD 400 million. Meanwhile, the US beef sector sees Mexico as a key growth market, especially as Mexico has become the second-largest buyer of American agricultural products, displacing China. However, looming tariff threats, border closures, and sanitary restrictions complicate bilateral trade and expose the fragility of an otherwise deeply integrated agri-food supply chain. The situation underscores how political and sanitary decisions can reshape trade dynamics and impact beef flows between these closely linked economies.

China's decision to revoke tariff exemptions on US meat products, particularly beef and pork, is expected to strain bilateral trade and weaken the competitiveness of US meat exports in the country. The move will reinstate steep tariffs originally imposed during the 2018 trade war, with pork duties rising from 57% to 87%, significantly impacting key export categories including variety meats. While the full scope of affected beef products is still unclear, US suppliers are bracing for a loss of market share to global competitors such as Brazil, Argentina, and Australia, who benefit from more favorable trade terms with China. The decision also reflects broader diplomatic tensions and China’s strategic push to diversify food sources amid ongoing concerns about food security. With annual US meat exports to China exceeding USD 2 billion, the loss of tariff advantages could have substantial economic repercussions for the sector.

Uruguay has preserved its preferential beef export terms to the US, maintaining a 10% tariff within quota and 36.4% outside, while Brazil faces an increased 76.4% tariff. This shift stems from emergency trade measures, rather than multilateral agreements, and reflects growing US concern over Brazil’s rapid rise in market share. Although Uruguay may not significantly increase volumes to the US, it could benefit from stronger prices due to the tighter supply of lean Brazilian beef. With US access restricted, Brazil is expected to redirect beef exports to alternative destinations such as China, Southeast Asia, and the Middle East, or possibly reroute through Mexico. While Uruguay temporarily holds a tariff advantage, it still faces competitive pressure from other countries with more favorable trade terms. China remains a key and stable market, showing notable YoY volume growth in Jul-25. Uruguay’s beef export earnings have also improved, with average values up 19% compared to last year, reflecting stronger international demand and pricing.

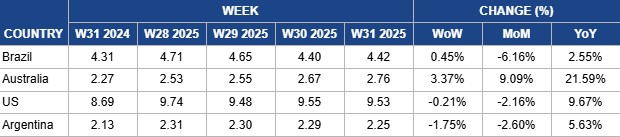

In W31, Brazil’s wholesale price for boneless rear beef rose by 0.45% week-on-week (WoW), reaching USD 4.42/kg. This figure also represented a 2.55% YoY increase, though it remained 6.16% lower month-on-month (MoM). According to Safras and Mercado, the wholesale market showed signs of an upward price trend, which is expected to persist in the short term. This outlook is supported by the injection of salaries into the economy and a projected rise in consumption linked to the upcoming Father’s Day. However, the growing competitiveness of chicken meat has tempered the positive momentum, casting a more cautious outlook on beef prices.

In the physical beef cattle market, Jul-25 saw persistent downward pressure, which Safras and Mercado attributed to the ample availability of domestic supply. Additionally, the market began to contend with uncertainty surrounding export prospects following the recent tariff hikes imposed on Brazilian beef by the US. Looking ahead into Aug-25, Safras and Mercado anticipate a moderate recovery in prices. This is expected to result from tightening slaughter scales, particularly among smaller slaughterhouses. In contrast, larger slaughterhouses are facing a different scenario, as they maintain more comfortable slaughter scales due to long-term partnership contracts and the use of in-house feedlot facilities.

In W31, Australia’s National Young Cattle Indicator (NYCI) rose to USD 2.76/kg, reflecting gains of 3.37% WoW, 9.09% MoM, and 21.59% YoY. According to Meat and Livestock Australia (MLA), the cattle market remained strong, supported by a tightening supply of finished stock. Notably, all National Livestock Reporting Service (NLRS) saleyard indicators reached their highest levels since the 2022–2023 summer period. National yardings fell 17% WoW to 50.99 thousand heads, largely driven by significant declines in Queensland and New South Wales. Meanwhile, the heavy steer indicator was just 7% higher than the processor cow indicator, underscoring a narrowing price gap. Export prices for 90CL (90% lean red meat and 10% fat) beef remained firm, supported by robust processor demand for both processor and dairy cows. This strong processor activity also spilled over into the restocker market, contributing to higher heifer prices.

W31, US lean beef (92% to 94% lean) averaged USD 9.53/kg, reflecting a slight decline of 0.21% WoW and 2.16% MoM, though still 9.67% higher YoY. The YoY increase highlights historically high price levels driven by tight supplies and sustained seasonal demand during the summer. According to the USDA, the US beef cattle inventory has dropped to 28.7 million heads as of Jul-25, its lowest level in decades, mainly due to prolonged droughts that have reduced available grazing land. Despite record-high prices, consumer demand for beef has remained remarkably resilient, indicating a continued willingness among Americans to pay for their preferred source of protein. However, market analysts caution that this consumer loyalty may be tested if broader economic conditions deteriorate. Such a shift could compound the challenges faced by producers, who are already under pressure from escalating input costs and narrowing profit margins.

In W31, Argentina’s average steer beef price declined by 1.75% WoW to USD 2.25/kg, marking a 2.60% MoM drop but still reflecting a 5.63% YoY increase. The weekly decline indicates subdued demand, while the annual gain signals a gradual recovery in beef consumption following the historic lows of 2024. In Jun-25, per capita beef consumption in Argentina reached 50.1 kg per year, up 5.2% YoY. This marks a notable rebound from the 2024 average of just 47.7 kg per person, a 9% drop from 2023 and the second-lowest level in recorded history, surpassed only by 1920.

In light of the US tariff hike, Brazil should urgently intensify diplomatic efforts to negotiate partial exemptions for beef or explore phased implementations to protect at-risk volumes. Simultaneously, Brazil should rapidly scale up exports to alternative markets such as China, Mexico, Japan, and South Korea, leveraging its recent animal health upgrades. Investing in supply chain adaptability, including logistics, certification processes, and product customization, will support redirection efforts. Additionally, Brazil should enhance domestic beef consumption through promotional campaigns and bolster cold chain infrastructure to manage potential surpluses.

To balance consumer affordability with producer protection, South Korea should expand the network of certified affordable Hanwoo outlets while investing in digital traceability systems to reinforce confidence in domestic beef quality. Meanwhile, authorities should continue to engage in trade talks focused on technical and non-tariff barrier improvements rather than market liberalization. This includes mutual recognition of safety standards and harmonization of customs procedures. With increasing public interest in food sovereignty, government campaigns highlighting the health, environmental, and quality benefits of Korean beef can help mitigate the appeal of lower-priced imports during peak demand seasons like Chuseok.

Uruguay should leverage its current tariff advantage in the US by negotiating longer-term guarantees on quota allocations and exploring expanded access through bilateral dialogues. At the same time, Uruguay should build on its quality reputation to further penetrate premium segments in China and Europe, especially as lean beef demand grows. Market intelligence efforts should be enhanced to monitor shifting trade routes caused by Brazil’s redirection, allowing Uruguay to adjust its logistics and export volumes accordingly. Strengthening relationships with regional partners through Mercosur or targeted trade pacts can also secure fallback markets and reinforce Uruguay’s resilience in a highly competitive global beef landscape.

Sources: Tridge, Agromeat, UkrAgroConsult, Yna

Read more relevant content

Recommended suppliers for you

What to read next