News

Original content

In May-24, Spain's olive oil consumption decreased by 2 thousand metric tons (mt) month-on-month (MoM), and exports declined by 3 thousand mt. This month's total outputs (excluding exports) were estimated at 75 to 80 thousand mt. To avoid a supply shortage, the average monthly consumption over the next five months should decrease by 25% to 30% over the consumption in the first seven months of the 2023/24 season.

In Spain, Ahorramás and Carrefour lowered the price of extra virgin olive oil from USD 10.41 per liter (EUR 9.55/l) to USD 9.76/l (EUR 8.95/L) by the end of May-24. This price adjustment is based on the decrease in olive oil prices at the source in Mar-24 and Apr-24, while the other competitors remained at the previous prices.

Tunisia's olive production fell below expectations to 210 to 220 thousand mt in the 2023/24 marketing year (MY). However, due to favorable weather patterns and increased cultivation, the 2024/25 season production is expected to return to an average of 240 to 260 thousand mt. The first official production estimate for the new season will be available by the end of Jun-24. The government aims to boost domestic consumption to 50 to 70 thousand mt this season and export the surplus to the European Union (EU) and the United States (US). This strategy seeks to position Tunisia as a reliable supplier to the standardization industry, offering competitive raw materials.

The Edremit Chamber of Commerce in Türkiye organized a conference dedicated to protecting local olive species from the effects of climate change. Olive growers from Spain and Greece attended the event, which included specialized training in olive oil tasting. Participants were introduced to the unique characteristics of the region's olive varieties and production processes. They also had the opportunity to taste and learn about the distinctive features of geographically marked products.

As of April 30, 2024, Italy's olive oil inventory totaled 223.41 thousand mt, with 204.97 thousand mt in bulk and 19.44 thousand mt packed. Extra virgin olive oils comprised 73% of the stocks, amounting to 163.13 thousand mt. Of this, 111.74 thousand mt were of Italian origin, while 35.87 thousand mt were from the EU, primarily Greece. Approximately 56% of Italy's olive oil supply was stored in the southern regions, with Puglia holding the largest share of 39.7% (88.6 thousand mt), followed by Tuscany with 35.6 thousand mt, Umbria with 23.32 thousand mt, and Calabria with 22.23 thousand mt.

At the International Olive Council’s 62nd Advisory Committee for Olive Oil and Table Olives, the head of Italia Olivicola highlighted the need to improve Italian extra virgin olive oil production. He emphasized the importance of promoting Italian olive varieties and sustainable cultivation practices over super-intensive models that may introduce foreign varieties. Additionally, he addressed the challenges posed by Xylella, a plant pathogen transmitted by insects, and called for a coordinated European response to the crisis. He proposed a project to develop a unified strategy to combat the disease and ensure the future sustainability of the olive farming sector.

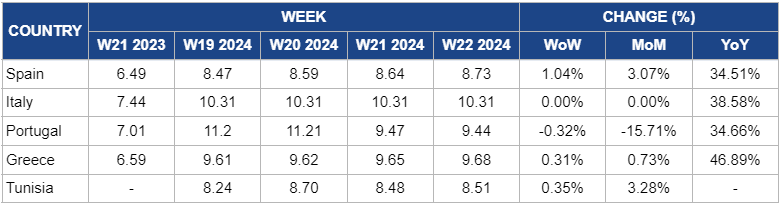

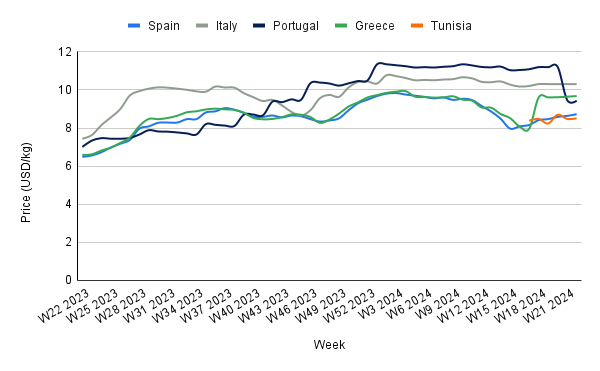

Weekly Olive Oil Pricing Important Exporters (USD/kg)

Yearly Change in Olive Oil Pricing Important Exporters (W222023 to W22 2024)

Spain's olive oil prices increased by 1.04% week-on-week (WoW) to USD 8.73 per kilogram (kg) in W22. The price increase is supported by a potential supply shortage based on the current dramatic supply and demand situation. The country must decrease consumption by 25% to 30% in the next five months to avoid a supply shortage. However, supply is expected to recover in the 2024/25 season due to optimistic production forecasts.

The olive oil prices in Italy remain unchanged at USD 10.31/kg in W22. However, based on a yearly comparison, the prices increased significantly by 38.58% year-on-year (YoY) compared to USD 7.44/kg in the same period last year. The price surge can be attributed to supply shortages due to climate change. With current stock reaching a historic low at 223.41 thousand mt, prices are anticipated to remain solid before the supply improves.

Portugal's olive oil prices slightly decreased WoW by 0.32% to USD 9.44/kg in W22. Portugal aims to increase its olive oil production to around 200 thousand m to ease demand, following Spain’s lead on the Iberian Peninsula. This target positions Portugal to potentially rival Greece in the fresh olive oil market.

Olive oil prices in Greece experienced a slight WoW increase of 0.31% to USD 9.68/kg in W22 compared to USD 9.65/kg in W21. This increase is due to currency fluctuations. The prices remained unchanged when measured in local currency. The export demand remained strong, with support from low inventories in Italy. According to the Molson-Pakion Cooperative of Laconia, olive oil export prices increased by USD 8.72/mt (EUR 8/mt) compared to the previous week.

Due to currency fluctuations, olive oil prices in Tunisia increased slightly by 0.35% WoW to USD 8.51/kg in W22. The country's first official estimate of olive production for the 2024/25 season will be available by the end of Jun-24, after the final phase of flowering settles down. Market stability is expected until then.

With an expected increase in olive production for the 2024/25 season, Tunisian stakeholders should optimize production and export strategies to capitalize on favorable market conditions. This includes investing in modern agricultural practices to maximize yield and quality and enhancing post-harvest processing and storage facilities to maintain product freshness. Furthermore, targeting key export markets such as the EU and the US with tailored marketing campaigns can help increase market penetration and drive export growth.

Given the challenges climate change and disease outbreaks pose, Italian olive oil producers should prioritize addressing supply chain challenges to ensure long-term sustainability. This could involve investing in climate-resilient olive varieties and implementing disease management strategies to mitigate the impact of Xylella and other threats. Furthermore, fostering collaboration among industry stakeholders, research institutions, and government agencies can facilitate knowledge sharing and innovation to overcome supply chain disruptions.

Source: OliMerca, Agronews, lha, Agrotypos, Agricolae

Read more relevant content

Recommended suppliers for you

What to read next