News

Original content

Argentina's 2023/24 peanut season shows strong recovery, with Córdoba—responsible for 87% of national production—projected to harvest 1.2 million metric tons (mmt), a 64% increase from the drought-affected previous season. Higher yields and favorable planting conditions drove the rebound, though the total planted area remains slightly below the five-year average. International prices have also risen, reaching USD 1,272 per metric ton (mt) free-on-board (FOB) in Mar-25, up 16% month-on-month (MoM), amid limited global supply. While recent rains may affect quality, strong export demand—especially from Europe—positions peanuts as a key contributor to Argentina's agroindustrial export earnings.

Weather in Bulgaria is forecast to be highly variable in Apr-25 due to several Mediterranean cyclones, bringing precipitation above normal levels. Consistent rainfall will enhance soil moisture, particularly in Northeastern and Eastern regions, benefiting early spring crops. However, cold snaps between April 7 and April 14, and potential late frosts around April 17 and April 20 may pose risks to emerging warm-weather crops, including peanuts. Despite this, sowing conditions for peanuts are expected to become favorable by late Apr-25, as soil temperatures reach optimal levels. Producers should remain cautious of pest activity and fungal diseases due to frequent rains, and monitor forecasts closely to time sowing and plant protection measures effectively.

Despite a bumper harvest, over 20,000 peanut farmers in Kendrapara, India, are facing severe financial losses as market prices have dropped to USD 58.07 per quintal (INR 5,000/quintal)—well below the official Minimum Support Price (MSP) of USD 78.78/quintal (INR 6,783/quintal) for the 2024/25 Kharif season. The absence of government procurement mandis has led to widespread distress sales, with many farmers reconsidering peanut cultivation altogether. Rising input costs, lack of oil mills and processing facilities, and poor market linkages have further compounded the crisis. Local farmer groups are urging immediate government intervention to stabilize prices and ensure fair returns.

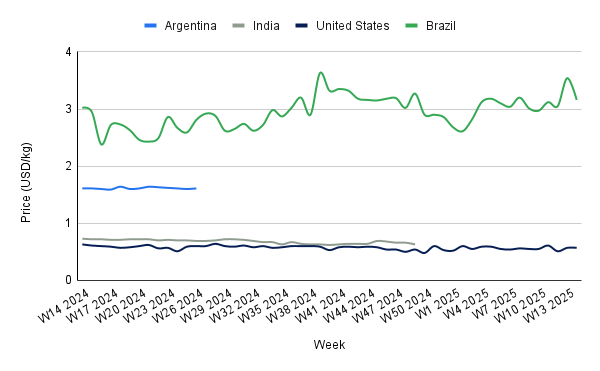

In W14, United States (US) peanut prices held steady at USD 0.57 per kilogram (kg), showing no weekly change but marking a 6.56% MoM and 9.52% year-on-year (YoY) decline. This price softening coincides with the beginning of the spring planting season, suggesting a potential easing of price pressures following years of gradual increases. The current stability may reflect a short-term balance in supply and demand. However, future prices remain sensitive to fluctuations in input costs—particularly fertilizers—as well as broader trade and demand dynamics. Continued monitoring of planting progress and global market trends will be critical in assessing future price trajectories.

Brazil’s peanut prices decreased to USD 3.16/kg in W14, registering a sharp 10.73% week-on-week (WoW) decline from USD 3.54/kg. This drop comes as the peanut harvest reaches its midpoint, with producers largely reporting favorable yields and quality. However, persistent concerns over extended rainfall remain, as delays in harvest due to wet conditions could negatively impact both yield and quality, potentially tightening supply and influencing future prices upward. Simultaneously, Brazil is intensifying efforts to expand its agricultural trade with the Philippines, positioning peanuts—alongside apples and onions—as key exports. The initiative aims to support Philippine inflation management while strengthening bilateral trade. Although current price declines reflect ample domestic availability, sustained international demand, particularly from emerging markets like the Philippines, could provide price support and shape future market dynamics.

Argentina should strengthen efforts to diversify peanut export markets beyond Europe by expanding trade relations with Asia and Africa. This would reduce overreliance on a single region and provide a buffer against fluctuations in EU demand or regulatory shifts.

To address low farmgate prices in regions like Kendrapara, India should prioritize investments in oil mills and peanut processing infrastructure. Improving local value chains would enhance price realization for farmers and reduce dependence on volatile raw peanut markets.

In Bulgaria, where variable weather poses risks to peanut cultivation, producers should implement adaptive sowing schedules and proactive pest and disease control measures. Leveraging local forecasting tools and timely interventions can help safeguard yields and crop quality.

Sources: Tridge, Sinor, Times of India, Punto a Punto, AG Info

Read more relevant content

Recommended suppliers for you

What to read next