News

Original content

In 2024, Argentina’s peanut industry achieved record exports of USD 1.186 billion, driven by high global demand and increased production. The country exported 730,030 metric tons (mt), with the European Union (EU) accounting for 73% of shipments, led by the Netherlands with 36%. Córdoba remains the leading producer, contributing 72% of the planted area, as total peanut cultivation reached a historic 473,000 hectares (ha). The expansion was influenced by favorable yields, stable prices, and declining profitability in alternative crops like soybeans and corn. Argentina continues to compete with India as a top global supplier, with technology and crop rotation strategies driving further regional expansion.

A fire at the Food Corporation of India (FCI) warehouse in Thangadh’s Heater Nagar, Surendranagar, destroyed 70,000 kilograms (kg) of peanuts. Around 2,000 government-stored sacks were lost. Gujarat State Co-operative Marketing Federation’s Chairman alleged possible foul play, suggesting the fire may have been set to conceal a scam and calling for a thorough investigation into the involvement of warehouse owners and officials.

Peanut acreage in Texas increased to 236,000 acres in 2024, up 14,000 acres from the previous year. The growth was driven by higher prices for Spanish peanuts, which now account for 46% of the state's crop. Texas remains the second-largest peanut producer in the United States (US), behind Georgia. Nationally, US peanut growers planted the most acres since 2017, with projected production reaching 4.1 million metric tons (mmt), increasing ending stocks to 862,000 metric tons (mt) –up from 740,000 mt the previous year. Further acreage growth in Texas is possible if hurricane-related losses on the East Coast increase prices.

In 2024, Georgia’s peanut production rose 2% year-on-year (YoY) to 3.21 billion pounds (lbs), despite a yield decline to 3,800 lbs/acre from 4,080 lbs in 2023. Peanut acreage increased to 170,000 acres, up from 160,000 the previous year. Georgia remains the largest peanut-producing state in the US.

In Jan-25, Uzbekistan saw a notable increase in peanut exports, shipping 1,384 mt valued at USD 1.5 million. The largest importer was Pakistan, receiving 496.9 mt, followed by Kazakhstan with 343.1 mt, and Russia with 145.4 mt. Highlighting the ongoing significance of peanuts as a key revenue source for Uzbekistan’s agricultural sector.

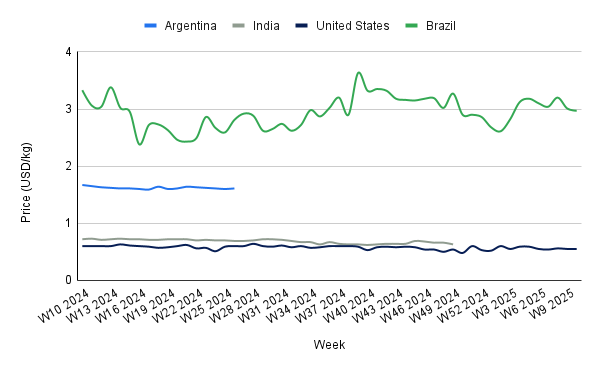

US peanut prices remained stable at USD 0.55/kg, reflecting an 8.33% YoY decrease despite increased production. Georgia’s output rose 2% YoY to 3.21 billion lbs in 2024, although yields declined. Texas’ peanut acreage expanded to 236,000 acres, driven by higher Spanish peanut prices, contributing to a national planting increase—the largest since 2017. With US production projected at 4.1 mmt and ending stocks rising to 862,000 mt, surplus supply may continue to pressure prices. However, potential hurricane-related crop losses on the East Coast could reduce supply and provide upward price support.

Brazil's peanut prices fell to USD 2.97/kg in W10, reflecting a 1.33% WoW decline and a 10.81% YoY decrease. Improved weather conditions in São Paulo have supported a production rebound, while the integration of peanut cultivation with sugarcane farming has stabilized supply. As the harvest advances, rising output may continue to pressure prices downward. However, potential weather disruptions could increase price volatility.

Further price declines are likely if favorable weather sustains high yields. Long-term price movements will depend on key factors such as global demand, trade policies, and export competition, especially from major producers like Argentina and the US. If Brazil's lower prices enhance its competitiveness in international markets, export volumes may rise, mitigating domestic oversupply and supporting future price stabilization.

Argentina and the US should explore new export markets beyond the EU and domestic consumption to reduce reliance on primary buyers and mitigate oversupply risks. Expanding trade relationships with emerging markets in Asia, the Middle East, and Africa can stabilize prices and increase market share. Governments and industry stakeholders can support this effort through targeted trade agreements and promotional campaigns.

Producers in Brazil, Argentina, and the US should closely track global price trends and adjust planting strategies accordingly. In regions where declining prices threaten profitability, integrating peanut cultivation with other crops (e.g., sugarcane in Brazil) can diversify revenue streams and maintain supply flexibility. Additionally, leveraging weather forecasting tools can help optimize planting schedules and mitigate climate-related disruptions.

Sources: Tridge, Fresh Plaza, Gujarat Samachar, Comercio y Justicia, North Texas E-News

Read more relevant content

Recommended suppliers for you

What to read next