OPINIO

Original content

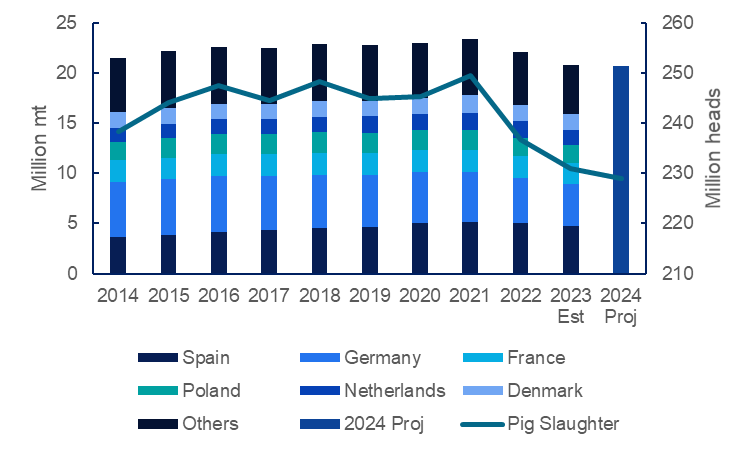

The European Union (EU) pork industry has experienced significant challenges over the past few years, including elevated pork prices and reduced exports primarily attributed to declining production. According to the European Commission (EC), pork production in the EU totaled 17.05 million metric tons (mmt) in the first 10 months of 2023, a 7.08% decrease compared to the corresponding period in 2022. Major pork-producing countries within the EU recorded year-on-year (YoY) drops during this period, with Denmark experiencing a 20.59% decline, equivalent to 276 thousand metric tons (mt), and Germany with 7.24% translating to 272 thousand mt. Projections for 2023 estimate the EU’s pork output at around 20.85 mmt, a 5.52% YoY decrease and the first instance of falling below the 21 mmt threshold since 2009. According to forecasts from the United States Department of Agriculture (USDA), a further decline is anticipated in 2024, reaching approximately 20.7 mmt, a marginal 0.72% YoY drop.

Figure 1: EU Pork Production and Pig Slaughter Trend

The substantial reduction in EU pork production is primarily attributed to a declining pig herd and a subsequent decrease in pig slaughter numbers. According to EC data, pig slaughters in the EU totaled 181.79 million heads from Jan-23 to Oct-23, a significant 7.55% decline compared to the same period in 2022. It is worth noting that EU pig slaughter has been on a steep decline since 2021 when it reached a record 249.57 million heads. Projections for 2023 estimate EU pig slaughter at 231 million heads, a 2.46% YoY drop. The USDA’s projections suggest a further decrease in pig slaughter in 2024, reaching approximately 226 million heads.

The dwindling EU pig slaughter numbers result from a contracting pig herd. Eurostat data reveals that the EU pig population stood at 134.41 million heads at the close of 2022, indicating a substantial 5.13% YoY decline. Notably, the EU pig herd has consistently diminished since 2020 when it recorded 145.91 million heads. The USDA's forecast estimates the EU pig population at 132.1 million heads at the beginning of 2024, reflecting a 1.72% decrease compared to the opening stock of 2023.

The decline in the pig herd is linked to economic challenges, including the surge in production input costs such as feed prices. Consequently, many EU producers opted to direct their pigs to slaughter to sustain their businesses in a challenging economic landscape. This decision resulted in a record pork production in 2021, followed by a decline in subsequent years. Despite prevailing feed prices being lower than the peak levels observed in mid-2022, pig farmers are reluctant to invest in their operations, driven by market uncertainties.

Additionally, the outbreak of African swine fever (ASF) in the EU has contributed to the diminishing pig herd. The German Interest Group of Pig Farmers (ISN) indicates a total of 12,121 ASF cases across the EU in 2023, nearly double the 2022 figure of 6,395, with first instances reported in Greece, Croatia, Kosovo, Bosnia-Herzegovina, and Sweden. Poland was the most affected country, with 2,654 outbreaks.

When ASF is detected, it is recommended that quarantine be carried out, including restricting pig movement and culling the affected pigs to prevent the spread of the disease. The significant expansion of ASF in the EU in 2023 underscores the urgency of robust biosecurity measures, surveillance efforts, and international cooperation to combat the spread of this devastating disease.

The EU market has witnessed a sustained surge in pork prices over recent years, primarily influenced by limited supplies in the market, resulting from diminishing production. Tridge's data reveals that the wholesale price of frozen pork ham and shoulder in Madrid, Spain, averaged USD 5.28 per kilogram (kg) in W2 of 2024, a 5.8% increase from USD 4.99/kg in the corresponding period in 2023. Notably, pork prices in 2023 displayed a bullish trend compared to the values recorded in 2021 and 2022. This trajectory is anticipated to persist in 2024, given the pessimistic forecasts for EU pork production and the pig herd. The heightened prices have impacted pork consumption negatively, prompting consumers to turn to more budget-friendly alternatives like chicken, particularly amid the high cost of living.

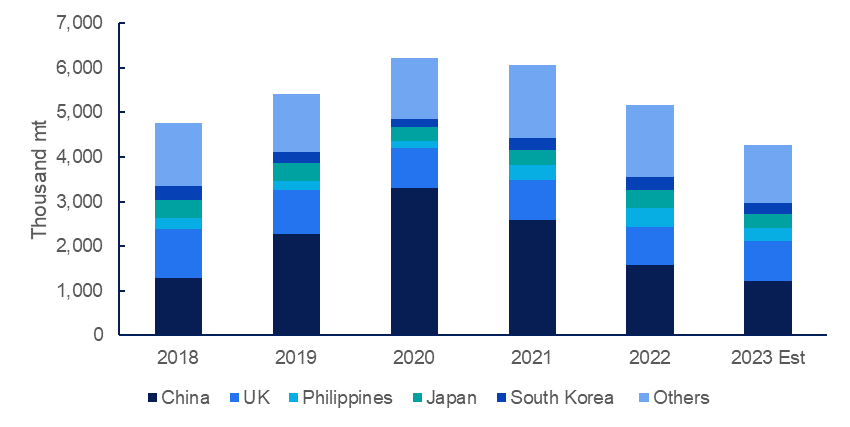

The declining pork production in the EU has significantly impacted exports. According to EC data, EU pork exports totaled 3.49 mmt in the first 10 months of 2023, a substantial 18.64% decrease compared to the corresponding period in 2022 and a notable 23.8% slump over the five-year average. Primary destinations for these shipments included China, the United Kingdom (UK), Japan, and the Philippines. Apart from the reduced availability of exportable pork, the deep drop in EU pork shipments is attributed to sluggish demand in China, where the anticipated rebound after the removal of COVID-19 restrictions did not materialize. Projections anticipate EU pork exports to reach around 4.27 mmt for 2023, a notable 17.25% YoY decline. This downward trend is expected to persist in 2024, driven by the forecasted continuous decline in production and subdued pork demand in China.

Figure 2: EU Pork Exports

Read more relevant content

Recommended suppliers for you

What to read next